Citibank 2013 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

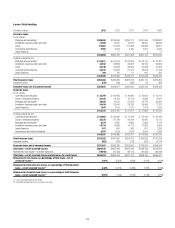

78

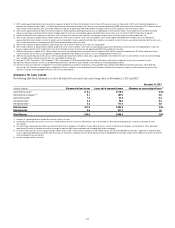

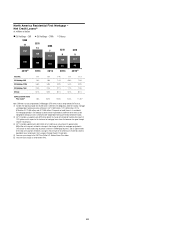

Allowance for Loan Losses

December 31, 2012

In billions of dollars Allowance for loan losses Loans, net of unearned income Allowance as a percentage of loans (1)

North America cards (2) $ 7.3 $ 112.0 6.5%

North America mortgages (3)(4) 8.6 125.4 6.9

North America other 1.5 22.1 6.8

International cards 2.9 40.7 7.0

International other (5) 2.4 108.5 2.2

Total Consumer $22.7 $ 408.7 5.6%

Total Corporate 2.8 246.8 1.1

Total Citigroup $25.5 $ 655.5 3.9%

(1) Allowance as a percentage of loans excludes loans that are carried at fair value.

(2) Includes both Citi-branded cards and Citi retail services. The $7.3 billion of loan loss reserves for North America cards as of December 31, 2012 represented approximately 18 months of coincident net credit

loss coverage.

(3) Of the $8.6 billion, approximately $8.4 billion was allocated to North America mortgages in Citi Holdings. Excluding the $40 million benefit related to finalizing the impact of the OCC guidance in the fourth quarter of

2012, the $8.6 billion of loan loss reserves for North America mortgages as of December 31, 2012 represented approximately 33 months of coincident net credit loss coverage.

(4) Of the $8.6 billion in loan loss reserves, approximately $4.5 billion and $4.1 billion is determined in accordance with ASC 450-20 and ASC 310-10-35 (troubled debt restructurings), respectively. Of the $125.4 billion

in loans, approximately $102.7 billion and $22.3 billion of the loans are evaluated in accordance with ASC 450-20 and ASC 310-10-35 (troubled debt restructurings), respectively. For additional information, see

Note 16 to the Consolidated Financial Statements.

(5) Includes mortgages and other retail loans.

Non-Accrual Loans and Assets and Renegotiated Loans

The following pages include information on Citi’s “Non-Accrual Loans

and Assets” and “Renegotiated Loans.” There is a certain amount of

overlap among these categories. The following summary provides a general

description of each category:

Non-Accrual Loans and Assets:

•Corporate and Consumer (commercial market) non-accrual status

is based on the determination that payment of interest or principal

is doubtful.

•Consumer non-accrual status is generally based on aging, i.e., the

borrower has fallen behind in payments.

•Mortgage loans discharged through Chapter 7 bankruptcy, other than

FHA-insured loans, are classified as non-accrual. In addition, home equity

loans in regulated bank entities are classified as non-accrual if the related

residential first mortgage loan is 90 days or more past due.

•North America Citi-branded cards and Citi retail services are not included

because under industry standards, credit card loans accrue interest

until such loans are charged off, which typically occurs at 180 days

contractual delinquency.

Renegotiated Loans:

•Both Corporate and Consumer loans whose terms have been modified in a

troubled debt restructuring (TDR).

•Includes both accrual and non-accrual TDRs.

Non-Accrual Loans and Assets

The table below summarizes Citigroup’s non-accrual loans as of the periods

indicated. Non-accrual loans may still be current on interest payments. In

situations where Citi reasonably expects that only a portion of the principal

owed will ultimately be collected, all payments received are reflected as a

reduction of principal and not as interest income. For all other non-accrual

loans, cash interest receipts are generally recorded as revenue.