Citibank 2013 Annual Report Download - page 316

Download and view the complete annual report

Please find page 316 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

298

The derivative instruments considered to be guarantees, which are

presented in the tables above, include only those instruments that require Citi

to make payments to the counterparty based on changes in an underlying

instrument that is related to an asset, a liability, or an equity security held by

the guaranteed party. More specifically, derivative instruments considered to

be guarantees include certain over-the-counter written put options where the

counterparty is not a bank, hedge fund or broker-dealer (such counterparties

are considered to be dealers in these markets and may, therefore, not hold the

underlying instruments). Credit derivatives sold by Citi are excluded from the

tables above as they are disclosed separately in Note 23 to the Consolidated

Financial Statements. In instances where Citi’s maximum potential future

payment is unlimited, the notional amount of the contract is disclosed.

Loans sold with recourse

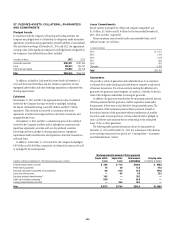

Loans sold with recourse represent Citi’s obligations to reimburse the buyers

for loan losses under certain circumstances. Recourse refers to the clause in a

sales agreement under which a lender will fully reimburse the buyer/investor

for any losses resulting from the purchased loans. This may be accomplished

by the seller taking back any loans that become delinquent.

In addition to the amounts shown in the tables above, Citi has recorded

a repurchase reserve for its potential repurchases or make-whole liability

regarding residential mortgage representation and warranty claims related

to its whole loan sales to the U.S. government-sponsored enterprises

(GSEs) and, to a lesser extent, private investors. The repurchase reserve was

approximately $341 million and $1,565 million at December 31, 2013 and

December 31, 2012, respectively, and these amounts are included in Other

liabilities on the Consolidated Balance Sheet.

Citi is also exposed to potential representation and warranty claims as

a result of mortgage loans sold through private-label securitizations in its

Consumer business in CitiMortgage as well as its legacy Securities and

Banking business. Beginning in the first quarter of 2013, Citi considers

private-label securitization representation and warranty claims as part of its

litigation accrual analysis and not as part of its repurchase reserve. See Note

28 to the Consolidated Financial Statements.

Securities lending indemnifications

Owners of securities frequently lend those securities for a fee to other parties

who may sell them short or deliver them to another party to satisfy some

other obligation. Banks may administer such securities lending programs for

their clients. Securities lending indemnifications are issued by the bank to

guarantee that a securities lending customer will be made whole in the event

that the security borrower does not return the security subject to the lending

agreement and collateral held is insufficient to cover the market value of

the security.

Credit card merchant processing

Credit card merchant processing guarantees represent the Company’s indirect

obligations in connection with: (i) providing transaction processing services

to various merchants with respect to its private-label cards; and (ii) potential

liability for bank card transaction processing services. The nature of the

liability in either case arises as a result of a billing dispute between a

merchant and a cardholder that is ultimately resolved in the cardholder’s

favor. The merchant is liable to refund the amount to the cardholder. In

general, if the credit card processing company is unable to collect this

amount from the merchant, the credit card processing company bears the

loss for the amount of the credit or refund paid to the cardholder.

With regard to (i) above, Citi has the primary contingent liability with

respect to its portfolio of private-label merchants. The risk of loss is mitigated

as the cash flows between Citi and the merchant are settled on a net basis and

Citi has the right to offset any payments with cash flows otherwise due to the

merchant. To further mitigate this risk, Citi may delay settlement, require a

merchant to make an escrow deposit, include event triggers to provide Citi

with more financial and operational control in the event of the financial

deterioration of the merchant, or require various credit enhancements

(including letters of credit and bank guarantees). In the unlikely event

that a private-label merchant is unable to deliver products, services or a

refund to its private-label cardholders, Citi is contingently liable to credit or

refund cardholders.

With regard to (ii) above, Citi has a potential liability for bank card

transactions where Citi provides the transaction processing services as well

as those where a third party provides the services and Citi acts as a secondary

guarantor, should that processor fail to perform.

Citi’s maximum potential contingent liability related to both bank card

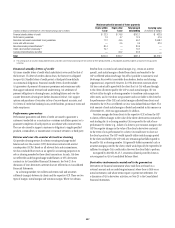

and private-label merchant processing services is estimated to be the total

volume of credit card transactions that meet the requirements to be valid

charge-back transactions at any given time. At December 31, 2013 and

December 31, 2012, this maximum potential exposure was estimated to be

$86 billion and $80 billion, respectively.

However, Citi believes that the maximum exposure is not representative

of the actual potential loss exposure based on its historical experience. This

contingent liability is unlikely to arise, as most products and services are

delivered when purchased and amounts are refunded when items are returned

to merchants. Citi assesses the probability and amount of its contingent

liability related to merchant processing based on the financial strength of the

primary guarantor, the extent and nature of unresolved charge-backs and

its historical loss experience. At December 31, 2013 and December 31, 2012,

the losses incurred and the carrying amounts of Citi’s contingent obligations

related to merchant processing activities were immaterial.