Citibank 2013 Annual Report Download - page 264

Download and view the complete annual report

Please find page 264 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

246

Managed Loans

After securitization of credit card receivables, the Company continues to

maintain credit card customer account relationships and provides servicing

for receivables transferred to the trusts. As a result, the Company considers

the securitized credit card receivables to be part of the business it manages.

As Citigroup consolidates the credit card trusts, all managed securitized card

receivables are on-balance sheet.

Funding, Liquidity Facilities and Subordinated Interests

As noted above, Citigroup securitizes credit card receivables through two

securitization trusts—Master Trust, which is part of Citicorp, and Omni

Trust, which is also substantially part of Citicorp. The liabilities of the trusts

are included in the Consolidated Balance Sheet, excluding those retained

by Citigroup.

Master Trust issues fixed- and floating-rate term notes. Some of the term

notes are issued to multi-seller commercial paper conduits. The weighted

average maturity of the term notes issued by the Master Trust was 3.1 years as

of December 31, 2013 and 3.8 years as of December 31, 2012.

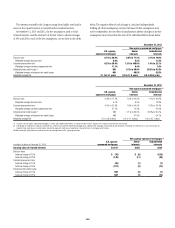

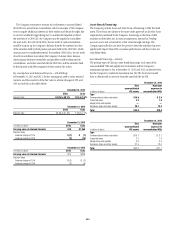

Master Trust Liabilities (at par value)

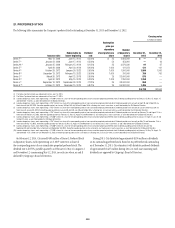

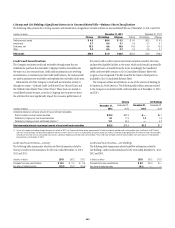

In billions of dollars

Dec. 31,

2013

Dec. 31,

2012

Term notes issued to third parties $27.9 $18.6

Term notes retained by Citigroup affiliates 6.2 4.8

Total Master Trust liabilities $34.1 $23.4

The Omni Trust issues fixed- and floating-rate term notes, some of which

are purchased by multi-seller commercial paper conduits. The weighted

average maturity of the third-party term notes issued by the Omni Trust was

0.7 years as of December 31, 2013 and 1.7 years as of December 31, 2012.

Omni Trust Liabilities (at par value)

In billions of dollars

Dec. 31,

2013

Dec. 31,

2012

Term notes issued to third parties $ 4.4 $ 4.4

Term notes retained by Citigroup affiliates 1.9 7.1

Total Omni Trust liabilities $ 6.3 $11.5

Mortgage Securitizations

The Company provides a wide range of mortgage loan products to a diverse

customer base. Once originated, the Company often securitizes these loans

through the use of SPEs. These SPEs are funded through the issuance of trust

certificates backed solely by the transferred assets. These certificates have

the same life as the transferred assets. In addition to providing a source of

liquidity and less expensive funding, securitizing these assets also reduces

the Company’s credit exposure to the borrowers. These mortgage loan

securitizations are primarily non-recourse, thereby effectively transferring

the risk of future credit losses to the purchasers of the securities issued by

the trust. However, the Company’s Consumer business generally retains

the servicing rights and in certain instances retains investment securities,

interest-only strips and residual interests in future cash flows from the trusts

and also provides servicing for a limited number of Securities and Banking

securitizations. Securities and Banking and Citi Holdings do not retain

servicing for their mortgage securitizations.

The Company securitizes mortgage loans generally through either a

government-sponsored agency, such as Ginnie Mae, Fannie Mae or Freddie

Mac (U.S. agency-sponsored mortgages), or private-label (non-agency-

sponsored mortgages) securitization. The Company is not the primary

beneficiary of its U.S. agency-sponsored mortgage securitizations because

Citigroup does not have the power to direct the activities of the SPE that most

significantly impact the entity’s economic performance. Therefore, Citi does

not consolidate these U.S. agency-sponsored mortgage securitizations.

The Company does not consolidate certain non-agency-sponsored

mortgage securitizations, because Citi is either not the servicer with the power

to direct the significant activities of the entity or Citi is the servicer but the

servicing relationship is deemed to be a fiduciary relationship and, therefore,

Citi is not deemed to be the primary beneficiary of the entity.

In certain instances, the Company has (i) the power to direct the

activities and (ii) the obligation to either absorb losses or the right to receive

benefits that could be potentially significant to its non-agency-sponsored

mortgage securitizations and, therefore, is the primary beneficiary and thus

consolidates the SPE.