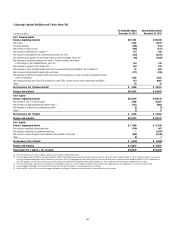

Citibank 2013 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

59

in July 2014. If Citi’s implementation of this compliance regime is not

consistent with regulatory expectations, this could further increase its

compliance risks and costs.

As in other areas of ongoing regulatory reform, alternative proposals for

the regulation of proprietary trading are developing in non-U.S. jurisdictions,

leading to overlapping or potentially conflicting regimes. For example, in

the EU, the “Liikanen Report” on bank structural reform has been reflected

in the recent European Commission proposal (the so-called “Barnier

Proposal”), which would prohibit proprietary trading by in-scope credit

institutions and banking groups, such as certain of Citi’s EU branches, and

potentially require the mandatory separation of certain trading activities into

a trading entity legally, economically and operationally separate from the

legal entity holding the banking activities of a firm.

It is likely that, given Citi’s worldwide operations, some form of these or

other proposals for the regulation of proprietary trading will eventually be

applicable to a portion of Citi’s operations. While the Volcker Rule and these

non-U.S. proposals are intended to address similar concerns— separating

the perceived risks of proprietary trading and certain other investment

banking activities in order not to affect more traditional banking and retail

activities—they would do so under different structures, which could result in

inconsistent regulatory regimes and additional compliance risks and costs for

Citi in light of its global activities.

Requirements in the U.S. and Non-U.S. Jurisdictions

to Facilitate the Future Orderly Resolution of Large

Financial Institutions Could Require Citi to Restructure

or Reorganize Its Businesses or Change Its Capital or

Funding Structure in Ways That Could Negatively Impact Its

Operations or Strategy.

Title I of the Dodd-Frank Act requires Citi to prepare and submit annually

a plan for the orderly resolution of Citigroup (the bank holding company)

and its significant legal entities under the U.S. Bankruptcy Code or other

applicable insolvency law in the event of future material financial distress or

failure. Citi is also required to prepare and submit an annual resolution plan

for its primary insured depository institution subsidiary, Citibank, N.A., and

to demonstrate how Citibank is adequately protected from the risks presented

by non-bank affiliates. These plans must include information on resolution

strategy, major counterparties and interdependencies, among other things,

and require substantial effort, time and cost across all of Citi’s businesses

and geographies. These resolution plans are subject to review by the Federal

Reserve Board and the FDIC. Citi submitted its resolution plan for 2013,

including the resolution plan for Citibank, N.A., in September 2013.

If the Federal Reserve Board and the FDIC both determine that Citi’s

resolution plan is not “credible” (which, although not defined, is generally

believed to mean the regulators do not believe the plan is feasible or

would otherwise allow the regulators to resolve Citi in a way that protects

systemically important functions without severe systemic disruption),

and Citi does not remedy the identified deficiencies in the plan within the

required time period, Citi could be required to restructure or reorganize

businesses, legal entities, operational systems and/or intracompany

transactions in ways that could negatively impact its operations and strategy,

or be subject to restrictions on growth. Citi could also eventually be subjected

to more stringent capital, leverage or liquidity requirements, or be required to

divest certain assets or operations.

In addition, other jurisdictions, such as the U.K., have requested or are

expected to request resolution plans from financial institutions, including

Citi, and the requirements and timing relating to these plans are or are

expected to be different from the U.S. requirements and from each other.

Responding to these additional requests will require additional effort, time

and cost, and regulatory review and requirements in these jurisdictions could

be in addition to, or conflict with, changes required by Citi’s regulators in

the U.S.

Title II of the Dodd-Frank Act grants the FDIC the authority, under certain

circumstances, to resolve systemically important financial institutions,

including Citi. In connection with this authority, in December 2013, the FDIC

released a notice describing its preferred single point of entry strategy for

resolving systemically important financial institutions. In furtherance of this

strategy, the Federal Reserve Board has indicated that it expects to propose

minimum levels of unsecured long-term debt required for bank holding

companies, as well as guidelines defining the terms or composition of

qualifying debt instruments, to ensure that adequate resources are available

at the holding company to resolve a systemically important financial

institution if necessary. To the extent that these future requirements differ

from Citi’s current funding profile, Citi may need to increase its aggregate

long-term debt levels and/or alter the composition and terms of its debt,

which could lead to increased costs of funds and have a negative impact

on its net interest revenue, among other potential impacts. Additionally, if

any final rules require compliance on an accelerated timeline, the resulting

increased issuance volume may further increase Citi’s cost of funds.

Furthermore, Citi could be at a competitive disadvantage versus financial

institutions that are not subject to such minimum debt requirements, such

as non-regulated financial intermediaries, smaller financial institutions and

entities in jurisdictions with less onerous or no such requirements.

Additional Regulations with Respect to Securitizations

Will Impose Additional Costs and May Prevent Citi from

Performing Certain Roles in Securitizations.

Citi plays a variety of roles in asset securitization transactions, including

acting as underwriter of asset-backed securities, depositor of the underlying

assets into securitization vehicles, trustee to securitization vehicles and

counterparty to securitization vehicles under derivative contracts. The

Dodd-Frank Act contains a number of provisions that affect securitizations.

These provisions, which in some cases will require multi-regulatory agency

implementation and will largely be applicable across asset classes, include

a prohibition on securitization participants engaging in transactions

that would involve a material conflict of interest with investors in the