Citibank 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

68

would include in its scope many instruments currently accounted for as

financial instruments and guarantees, including some where credit rather

than insurance risk is the primary risk factor. As a result, certain financial

contracts deemed to have significant insurance risk could no longer be

recorded at fair value, and the timing of income recognition for insurance

contracts could also be changed. For additional information on these and

other proposed changes, see Note 1 to the Consolidated Financial Statements.

Changes to financial accounting or reporting standards, whether

promulgated or required by the FASB or other regulators, could present

operational challenges and could require Citi to change certain of the

assumptions or estimates it previously used in preparing its financial

statements, which could negatively impact how it records and reports its

financial condition and results of operations generally and/or with respect

to particular businesses. In addition, the FASB continues its convergence

project with the International Accounting Standards Board (IASB) pursuant

to which U.S. GAAP and International Financial Reporting Standards (IFRS)

may be converged. Any transition to IFRS could further have a material

impact on how Citi records and reports its financial results. For additional

information on the key areas for which assumptions and estimates are used

in preparing Citi’s financial statements, see “Significant Accounting Policies

and Significant Estimates” below and Note 28 to the Consolidated Financial

Statements.

It Is Uncertain Whether Any Further Changes in the

Administration of LIBOR Could Affect the Value of LIBOR-

Linked Debt Securities and Other Financial Obligations

Held or Issued by Citi.

As a result of concerns in recent years regarding the accuracy of LIBOR,

changes have been made to the administration and process for determining

LIBOR, including increasing the number of banks surveyed to set LIBOR,

streamlining the number of LIBOR currencies and maturities and generally

strengthening the oversight of the process, including by providing for U.K.

regulatory oversight of LIBOR. In early 2014, Intercontinental Exchange

(ICE) took over the administration of LIBOR from the British Banker’s

Association (BBA).

It is uncertain whether or to what extent any further changes in the

administration or method for determining LIBOR could have on the value of

any LIBOR-linked debt securities issued by Citi, or any loans, derivatives and

other financial obligations or extensions of credit for which Citi is an obligor.

It is also not certain whether or to what extent any such changes would

have an adverse impact on the value of any LIBOR-linked securities, loans,

derivatives and other financial obligations or extensions of credit held by or

due to Citi or on Citi’s overall financial condition or results of operations.

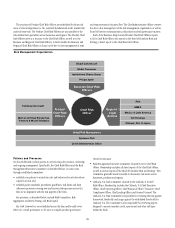

Citi May Incur Significant Losses If Its Risk Management

Processes and Strategies Are Ineffective, and Concentration

of Risk Increases the Potential for Such Losses.

Citi’s independent risk management organization is structured to facilitate

the management of the principal risks Citi assumes in conducting its

activities—credit risk, market risk and operational risk—across three

dimensions: businesses, regions and critical products. Credit risk is the

potential for financial loss resulting from the failure of a borrower or

counterparty to honor its financial or contractual obligations. Market risk

encompasses funding risk, liquidity risk and price risk. Price risk losses

arise from fluctuations in the market value of trading and non-trading

positions resulting from changes in interest rates, credit spreads, foreign

exchange rates, equity and commodity prices and in their implied volatilities.

Operational risk is the risk of loss resulting from inadequate or failed

internal processes, systems or human factors, or from external events, and

includes reputation and franchise risk associated with business practices

or market conduct in which Citi is involved. For additional information on

each of these areas of risk as well as risk management at Citi, including

management review processes and structure, see “Managing Global Risk”

below. Managing these risks is made especially challenging within a

global and complex financial institution such as Citi, particularly given

the complex and diverse financial markets and rapidly evolving market

conditions in which Citi operates.

Citi employs a broad and diversified set of risk management and

mitigation processes and strategies, including the use of various risk models,

in analyzing and monitoring these and other risk categories. However, these

models, processes and strategies are inherently limited because they involve

techniques, including the use of historical data in some circumstances, and

judgments that cannot anticipate every economic and financial outcome

in the markets in which Citi operates nor can they anticipate the specifics

and timing of such outcomes. Citi could incur significant losses if its risk

management processes, strategies or models are ineffective in properly

anticipating or managing these risks.

In addition, concentrations of risk, particularly credit and market

risk, can further increase the risk of significant losses. At December 31,

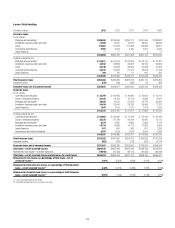

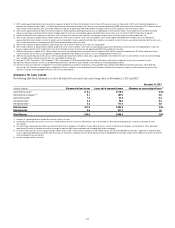

2013, Citi’s most significant concentration of credit risk was with the U.S.

government and its agencies, which primarily results from trading assets and

investments issued by the U.S. government and its agencies (for additional

information, see Note 24 to the Consolidated Financial Statements). Citi

also routinely executes a high volume of securities, trading, derivative

and foreign exchange transactions with counterparties in the financial

services sector, including banks, other financial institutions, insurance

companies, investment banks and government and central banks. To the

extent regulatory or market developments lead to an increased centralization

of trading activity through particular clearing houses, central agents or

exchanges, this could increase Citi’s concentration of risk in this sector.

Concentrations of risk can limit, and have limited, the effectiveness of Citi’s

hedging strategies and have caused Citi to incur significant losses, and they

may do so again in the future.