Citibank 2013 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

87

Based on the limited number of Revolving HELOCs that have begun

amortization as of December 31, 2013, approximately 6.0% of the amortizing

home equity loans were 30+ days past due compared to 2.8% of the total

outstanding home equity loan portfolio (amortizing and non-amortizing).

However, these resets have generally occurred during a period of declining

interest rates, which Citi believes has likely reduced the overall “payment

shock” to the borrower. Citi continues to monitor this reset risk closely,

particularly as it approaches 2015, and Citi will continue to consider any

potential impact in determining its allowance for loan loss reserves. In

addition, management continues to review additional actions to offset

potential reset risk, such as extending offers to non-amortizing home equity

loan borrowers to convert the non-amortizing home equity loan to a fixed-

rate amortizing loan. See also “Risk Factors—Business and Operational

Risks” above.

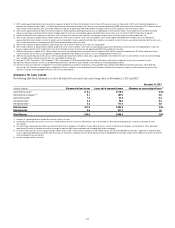

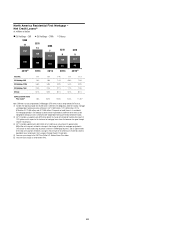

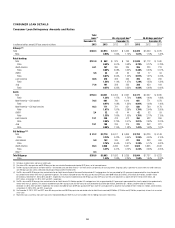

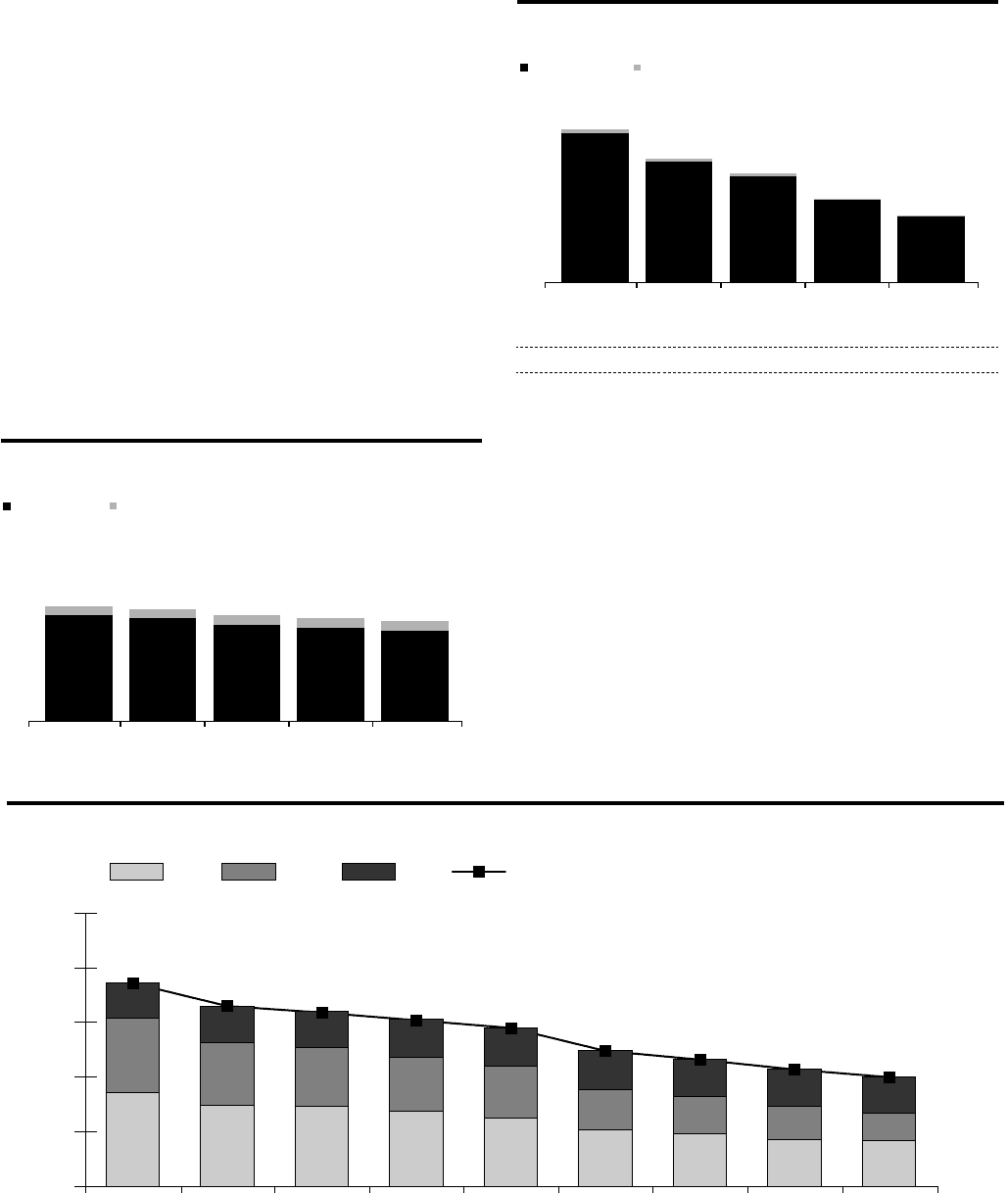

The following charts detail the quarterly trends in loan balances, net

credit losses and delinquencies for Citi’s home equity loan portfolio in

North America. The vast majority of Citi’s home equity loan exposure arises

from its portfolio in Citi Holdings.

4Q’133Q’132Q’131Q’134Q’12

34

3

33

3

31

3

30

3

29

3

North America Home Equity — EOP Loans

In billions of dollars

Citi Holdings Citicorp

$37 $36 $34 $32

$33

4Q’13(3)

3Q’132Q’131Q’134Q’12(2)

385

10

312

6

274

6

212

3

169

3

North America Home Equity — Net Credit Losses(1)

In millions of dollars

Citi Holdings Citicorp

$394

$318 $280

$173

$215

Total NCL 4.1% 3.5% 3.2% 2.5% 2.1%

Citi Holdings 4.4% 3.8% 3.4% 2.7% 2.3%

Citicorp 1.2% 0.8% 0.8% 0.4% 0.5%

(1) Includes the following amounts of charge-offs related to Citi’s fulfillment of its obligations under

the national mortgage and independent foreclosure review settlements: 4Q’12, $30 million; 1Q’13,

$51 million; 2Q’13, $12 million; 3Q’13, $14 million; and 4Q’13, $15 million. Citi expects net credit

losses in its home equity loan portfolio in Citi Holdings to continue to be impacted by its fulfillment of

the terms of the independent foreclosure review settlement. See “Independent Foreclosure Review

Settlement” below.

(2) 4Q’12 excludes an approximately $30 million benefit to charge-offs related to finalizing the impact

of the OCC guidance with respect to the treatment of mortgage loans where the borrower has gone

through Chapter 7 bankruptcy.

(3) 4Q’13 excludes approximately $100 million of net credit losses consisting of (i) approximately

$64 million for the acceleration of accounting losses associated with modified home equity loans

determined to be collateral dependent, (ii) approximately $22 million of charge-offs related to a

change in the charge-off policy for mortgages originated in CitiFinancial to more closely align to

policies used in the CitiMortgage business, and (iii) approximately $14 million of charge-offs related

to a change in the estimate of net credit losses related to collateral dependent loans to borrowers that

have gone through Chapter 7 bankruptcy.

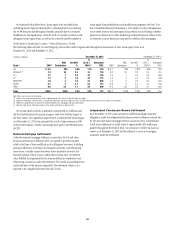

North America Home Equity Loan Delinquencies—Citi Holdings

In billions of dollars

Days Past Due:

0.0

0.5

1.0

1.5

2.0

2.5

30+ DPD

180+

90-179

30-89

4Q133Q132Q131Q134Q123Q122Q121Q124Q11

0.86 0.74 0.73 0.69 0.63 0.52 0.48 0.43 0.42

0.68 0.58 0.54 0.49 0.47 0.37 0.34 0.30 0.25

0.32

0.33 0.33 0.35 0.35

0.35 0.34 0.33

0.34

1.86

1.65 1.59 1.52 1.45

1.24 1.16 1.07 1.00

Note: Days past due excludes (i) U.S. mortgage loans that are guaranteed by U.S. government-sponsored agencies, because the potential loss predominantly resides with the U.S. agencies, and (ii) loans recorded at fair

value. Totals may not sum due to rounding.