Citibank 2013 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

198

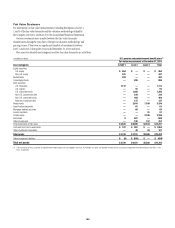

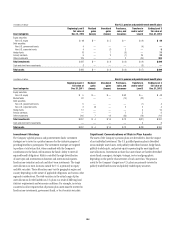

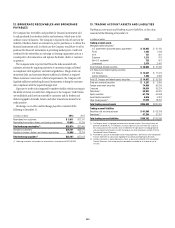

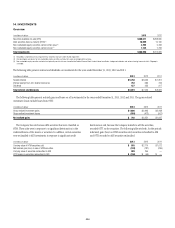

The following table summarizes the amounts of tax carry-forwards and

their expiration dates as of December 31, 2013:

In billions of dollars Amount

Year of expiration

December 31,

2013

December 31,

2012

U.S. tax return foreign tax credit

carry-forwards

2016 $ — $ 0.4

2017 4.7 6.6

2018 5.2 5.3

2019 1.2 1.3

2020 3.1 2.3

2021 1.4 1.9

2022 3.3 4.2

2023 (1) 0.7 —

Total U.S. tax return foreign tax credit

carry-forwards $19.6 $22.0

U.S. tax return general business credit

carry-forwards

2027 $ — $ 0.3

2028 0.4 0.4

2029 0.4 0.4

2030 0.4 0.5

2031 0.4 0.5

2032 0.5 0.5

2033 0.4 —

Total U.S. tax return general business credit

carry-forwards $ 2.5 $ 2.6

U.S. subsidiary separate federal NOL carry-forwards

2027 $ 0.2 $ 0.2

2028 0.1 0.1

2030 0.3 0.3

2031 1.7 1.8

2033 1.7 —

Total U.S. subsidiary separate federal NOL

carry-forwards (2) $ 4.0 $ 2.4

New York State NOL carry-forwards

2027 $ 0.1 $ 0.1

2028 6.5 7.2

2029 2.0 1.9

2030 0.1 0.4

2032 0.9 —

Total New York State NOL carry-forwards (2) $ 9.6 $ 9.6

New York City NOL carry-forwards

2027 $ 0.1 $ 0.1

2028 3.9 3.7

2029 1.5 1.6

2032 0.6 0.2

Total New York City NOL carry-forwards (2) $ 6.1 $ 5.6

APB 23 subsidiary NOL carry-forwards

Various $ 0.2 $ 0.2

Total APB 23 subsidiary NOL carry-forwards $ 0.2 $ 0.2

(1) The $0.7 billion in FTC carry-forwards that expires in 2023 is in a non-consolidated tax return entity

but is eventually expected to be utilized in Citigroup’s consolidated tax return.

(2) Pretax.

While Citi’s net total DTAs decreased year-over-year, the time remaining

for utilization has shortened, given the passage of time, particularly with

respect to the FTC component of the DTAs. Realization of the DTAs will

continue to be driven by Citi’s ability to generate U.S. taxable earnings in the

carry-forward periods, including through actions that optimize Citi’s U.S.

taxable earnings.

Although realization is not assured, Citi believes that the realization

of the recognized net DTAs of $52.8 billion at December 31, 2013 is more

likely than not based upon expectations as to future taxable income in the

jurisdictions in which the DTAs arise and available tax planning strategies

(as defined in ASC 740, Income Taxes) that would be implemented, if

necessary, to prevent a carry-forward from expiring. In general, Citi would

need to generate approximately $98 billion of U.S. taxable income during the

FTC carry-forward periods to prevent this most time sensitive component of

Citi’s DTAs from expiring. Citi’s net DTAs will decline primarily as additional

domestic GAAP taxable income is generated.

Citi has concluded that two components of positive evidence support the

full realization of its DTAs. First, Citi forecasts sufficient U.S. taxable income

in the carryforward periods, exclusive of ASC 740 tax planning strategies.

Citi’s forecasted taxable income, which will continue to be subject to overall

market and global economic conditions, incorporates geographic business

forecasts and taxable income adjustments to those forecasts (e.g., U.S.

tax exempt income, loan loss reserves deductible for U.S. tax reporting in

subsequent years), and actions intended to optimize its U.S. taxable earnings.

Second, Citi has sufficient tax planning strategies available to it under

ASC 740 that would be implemented to prevent a carry-forward from

expiring. These strategies include: repatriating low taxed foreign source

earnings for which an assertion that the earnings have been indefinitely

reinvested has not been made; accelerating U.S. taxable income into, or

deferring U.S. tax deductions out of, the latter years of the carry-forward

period (e.g., selling appreciated intangible assets, electing straight-line

depreciation); accelerating deductible temporary differences outside the

U.S.; and selling certain assets that produce tax-exempt income, while

purchasing assets that produce fully taxable income. In addition, the sale

or restructuring of certain businesses can produce significant U.S. taxable

income within the relevant carry-forward periods.