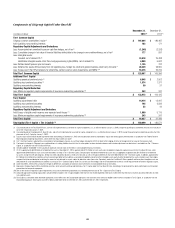

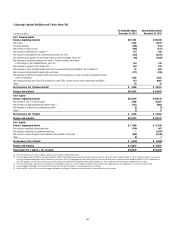

Citibank 2013 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

57

N.A., during 2013, there continues to be significant uncertainty regarding

numerous aspects of these and other regulatory capital requirements

applicable to Citi and, as a result, the ultimate impact of these requirements

on Citi.

Citi’s estimated Basel III ratios and related components are based on

its current interpretation, expectations and understanding of the final U.S.

Basel III rules and are subject to, among other things, ongoing regulatory

review, regulatory approval of Citi’s credit, market and operational Basel III

risk models (as well as its market risk models under Basel II.5), additional

refinements, modifications or enhancements (whether required or otherwise)

to Citi’s models, and further implementation guidance in the U.S. Any

modifications or requirements resulting from these ongoing reviews or the

continued implementation of Basel III in the U.S. could result in changes

in Citi’s risk-weighted assets or other elements involved in the calculation

of Citi’s Basel III ratios, which could negatively impact Citi’s capital ratios

and its ability to achieve its capital requirements as it projects or as required.

Further, because operational risk is measured based not only upon Citi’s

historical loss experience but also upon ongoing events in the banking

industry generally, Citi’s level of operational risk-weighted assets could

remain elevated for the foreseeable future, despite Citi’s continuing efforts to

reduce its risk-weighted assets and exposures.

In addition, subsequent to the issuance of the final U.S. Basel III rules,

the U.S. banking agencies proposed to amend the final U.S. Basel III rules to

require the largest U.S. bank holding companies and their insured depository

institution subsidiaries, including Citi and Citibank, N.A., to effectively

maintain minimum Supplementary Leverage ratios (SLRs) of 5% and 6%,

respectively, compared to the minimum 3% required under the final U.S.

and Basel Committee Basel III rules. If adopted as proposed, the SLR, which

was initially intended only to supplement the risk-based capital ratios, may

become the binding regulatory capital constraint facing Citi and Citibank,

N.A. In addition, when combined with the expected U.S. Tier 1 Common

Capital “global systemically important bank” (G-SIB) surcharge and other

capital requirements, Citi and Citibank, N.A. could be subject to higher

capital requirements than many of their U.S. and non-U.S. competitors,

leading to a potential competitive disadvantage and negative impact on Citi’s

businesses and results of operations.

Various proposals relating to the future liquidity standards or funding

requirements applicable to U.S. financial institutions further contribute to

the uncertainty regarding the future capital requirements applicable to Citi.

For example, the proposed U.S. Basel III Liquidity Coverage ratio (LCR) rules

would require Citi to hold additional high-quality liquid assets; however,

this requirement would also serve to increase the denominator of the SLR

and, as a result, increase the amount of Tier 1 Capital required to be held

by Citi to meet the minimum SLR requirements. The Federal Reserve Board

has also indicated it is considering proposals relating to the use of short-

term wholesale funding by U.S. financial institutions, particularly securities

financing transactions (SFTs), which could include a capital surcharge

based on the institution’s reliance on such funding, and/or increased capital

requirements applicable to SFT matched books.

As a result of these and other uncertainties arising from the ongoing

implementation of Basel III and other current or potential capital

requirements on a global basis, Citi’s capital planning and management

remains challenging. It is also not possible to determine what the overall

impact of these extensive regulatory capital changes will be on Citi’s

competitive position (among both domestic and international peers),

businesses, product offerings or results of operations.

For additional information on the Basel III Rules and other capital

and liquidity standards developments and requirements referenced above,

see “Liquidity Risks” below and “Capital Resources—Regulatory Capital

Standards Developments” above.

The Impact to Citi’s Derivatives Businesses and Results of

Operations Resulting from the Ongoing Implementation

of Derivatives Regulation in the U.S. and Globally

Remains Uncertain.

The ongoing implementation of derivatives regulations in the U.S. under

the Dodd-Frank Act as well as in non-U.S. jurisdictions has impacted, and

will continue to substantially impact, the derivatives markets by, among

other things: (i) requiring extensive regulatory and public price reporting

of derivatives transactions; (ii) requiring a wide range of over-the-counter

derivatives to be cleared through recognized clearing facilities and traded

on exchanges or exchange-like facilities; (iii) requiring the collection

and segregation of collateral for most uncleared derivatives (margin

requirements); and (iv) significantly broadening limits on the size of

positions that may be maintained in specified derivatives. These market

structure reforms have and will likely continue to make trading in many

derivatives products more costly, may significantly reduce the liquidity

of certain derivatives markets and could diminish customer demand for

covered derivatives. However, given the early stage of implementation of

these U.S. and global reforms, including the additional rulemaking that

may be or is required to occur and the ongoing significant interpretive issues

across jurisdictions, the ultimate impact to Citi’s results of operations in its

derivatives businesses remains uncertain.

For example, in October 2013, certain CFTC rules relating to trading on a

swap execution facility (SEF) became effective. As a result, certain non-U.S.

trading platforms that do not want to register with the CFTC as a SEF are

prohibiting firms with U.S. contacts, such as Citi, from trading on their

non-U.S. platforms. This has resulted in some bifurcated client activity in

the swaps marketplace, which could negatively impact Citi by reducing its

access to non-U.S. platform client activity. Also in October 2013, the CFTC’s

mandatory clearing requirements for the overseas branches of Citibank,

N.A. became effective, and certain of Citi’s non-U.S. clients have ceased to

clear their swaps with Citi given the mandatory requirement. More broadly,