Citibank 2013 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

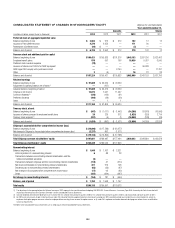

|

|

162

on Citi’s analysis of its most recent collection trends and the financial

viability of the third-party sellers (i.e., to the extent Citi made representation

and warranties on loans it purchased from third-party sellers that remain

financially viable, Citi may have the right to seek recovery from the third

party based on representations and warranties made by the third party to Citi

(a “back-to-back” claim)).

In the case of a repurchase, Citi will bear any subsequent credit loss on

the mortgage loan and the loan is typically considered a credit-impaired

loan and accounted for under AICPA Statement of Position (SOP) 03-3,

“Accounting for Certain Loans and Debt Securities Acquired in a Transfer”

(now incorporated into ASC 310-30, Receivables—Loans and Debt

Securities Acquired with Deteriorated Credit Quality) (SOP 03-3).

In the case of a repurchase of a credit-impaired SOP 03-3 loan, the

difference between the loan’s fair value and unpaid principal balance at the

time of the repurchase is recorded as a utilization of the repurchase reserve.

Make-whole payments to the investor are also treated as utilizations and

charged directly against the reserve. The repurchase reserve is estimated

when Citi sells loans (recorded as an adjustment to the gain on sale, which is

included in Other revenue in the Consolidated Statement of Income) and is

updated quarterly. Any change in estimate is recorded in Other revenue.

Goodwill

Goodwill represents the excess of acquisition cost over the fair value

of net tangible and intangible assets acquired. Goodwill is subject to

annual impairment testing and between annual tests if an event occurs

or circumstances change that would more likely than not reduce the fair

value of a reporting unit below its carrying amount. The Company has an

option to assess qualitative factors to determine if it is necessary to perform

the goodwill impairment test. If, after assessing the totality of events or

circumstances, the Company determines that it is not more likely than not

that the fair value of a reporting unit is less than its carrying amount, no

further testing is necessary. If, however, the Company determines that it

is more likely than not that the fair value of a reporting unit is less than

its carrying amount, the Company is required to perform the first step

of the two-step goodwill impairment test. Furthermore, on any business

dispositions, goodwill is allocated to the business disposed of based on the

ratio of the fair value of the business disposed of to the fair value of the

reporting unit.

Additional information on Citi’s goodwill impairment testing can be

found in Note 17 to the Consolidated Financial Statements.

Intangible Assets

Intangible assets—including core deposit intangibles, present value

of future profits, purchased credit card relationships, other customer

relationships, and other intangible assets, but excluding MSRs—are

amortized over their estimated useful lives. Intangible assets deemed to

have indefinite useful lives, primarily certain asset management contracts

and trade names, are not amortized and are subject to annual impairment

tests. An impairment exists if the carrying value of the indefinite-lived

intangible asset exceeds its fair value. For other intangible assets subject to

amortization, an impairment is recognized if the carrying amount is not

recoverable and exceeds the fair value of the intangible asset.

Other Assets and Other Liabilities

Other assets include, among other items, loans held-for-sale, deferred tax

assets, equity method investments, interest and fees receivable, premises

and equipment, repossessed assets, and other receivables. Other liabilities

include, among other items, accrued expenses and other payables, deferred

tax liabilities, and reserves for legal claims, taxes, unfunded lending

commitments, repositioning reserves, and other matters.

Other Real Estate Owned and Repossessed Assets

Real estate or other assets received through foreclosure or repossession are

generally reported in Other assets, net of a valuation allowance for selling

costs and subsequent declines in fair value.

Securitizations

The Company primarily securitizes credit card receivables and mortgages.

Other types of securitized assets include corporate debt instruments (in cash

and synthetic form) and student loans.

There are two key accounting determinations that must be made

relating to securitizations. Citi first makes a determination as to whether the

securitization entity would be consolidated. Second, it determines whether

the transfer of financial assets to the entity is considered a sale under GAAP. If

the securitization entity is a VIE, the Company consolidates the VIE if it is the

primary beneficiary (as discussed in “Variable Interest Entities” above). For

all other securitization entities determined not to be VIEs in which Citigroup

participates, a consolidation decision is based on which party has voting

control of the entity, giving consideration to removal and liquidation rights

in certain partnership structures. Only securitization entities controlled by

Citigroup are consolidated.

Interests in the securitized and sold assets may be retained in the form

of subordinated or senior interest-only strips, subordinated tranches, spread

accounts and servicing rights. In credit card securitizations, the Company

retains a seller’s interest in the credit card receivables transferred to the trusts,

which is not in securitized form. In the case of consolidated securitization

entities, including the credit card trusts, these retained interests are not

reported on Citi’s Consolidated Balance Sheet. The securitized loans remain