Citibank 2013 Annual Report Download - page 229

Download and view the complete annual report

Please find page 229 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

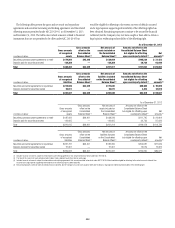

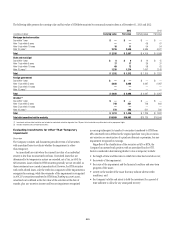

211

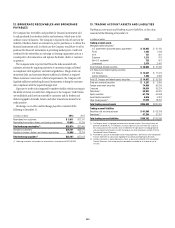

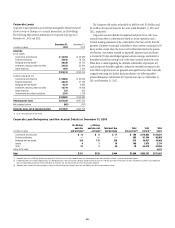

The Company’s review for impairment generally entails:

• identification and evaluation of investments that have indications of

possible impairment;

• analysis of individual investments that have fair values less than

amortized cost, including consideration of the length of time the

investment has been in an unrealized loss position and the expected

recovery period;

• discussion of evidential matter, including an evaluation of factors or

triggers that could cause individual investments to qualify as having

other-than-temporary impairment and those that would not support

other-than-temporary impairment; and

• documentation of the results of these analyses, as required under

business policies.

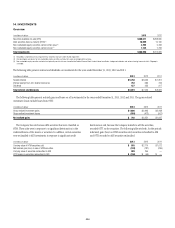

Debt

Under the guidance for debt securities, OTTI is recognized in earnings

for debt securities that the Company has an intent to sell or that the

Company believes it is more-likely-than-not that it will be required to sell

prior to recovery of the amortized cost basis. For those securities that the

Company does not intend to sell or expect to be required to sell, credit-

related impairment is recognized in earnings, with the non-credit-related

impairment recorded in AOCI.

For debt securities that are not deemed to be credit impaired,

management assesses whether it intends to sell or whether it is more-likely-

than-not that it would be required to sell the investment before the expected

recovery of the amortized cost basis. In most cases, management has asserted

that it has no intent to sell and that it believes it is not likely to be required to

sell the investment before recovery of its amortized cost basis. Where such an

assertion cannot be made, the security’s decline in fair value is deemed to be

other than temporary and is recorded in earnings.

For debt securities, a critical component of the evaluation for OTTI is

the identification of credit impaired securities, where management does

not expect to receive cash flows sufficient to recover the entire amortized

cost basis of the security. For securities purchased and classified as AFS with

the expectation of receiving full principal and interest cash flows as of the

date of purchase, this analysis considers the likelihood and the timing of

receiving all contractual principal and interest. For securities reclassified out

of the trading category in the fourth quarter of 2008, the analysis considers

the likelihood of receiving the expected principal and interest cash flows

anticipated as of the date of reclassification in the fourth quarter of 2008.

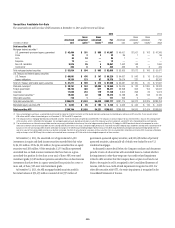

Equity

For equity securities, management considers the various factors described

above, including its intent and ability to hold the equity security for a period

of time sufficient for recovery to cost or whether it is more-likely-than-not

that the Company will be required to sell the security prior to recovery of

its cost basis. Where management lacks that intent or ability, the security’s

decline in fair value is deemed to be other-than-temporary and is recorded in

earnings. AFS equity securities deemed other-than-temporarily impaired are

written down to fair value, with the full difference between fair value and cost

recognized in earnings.

Management assesses equity method investments with fair value less

than carrying value for OTTI. Fair value is measured as price multiplied

by quantity if the investee has publicly listed securities. If the investee is

not publicly listed, other methods are used (see Note 25 to the Consolidated

Financial Statements).

For impaired equity method investments that Citi plans to sell prior to

recovery of value or would likely be required to sell, with no expectation that

the fair value will recover prior to the expected sale date, the full impairment

is recognized in earnings as OTTI regardless of severity and duration. The

measurement of the OTTI does not include partial projected recoveries

subsequent to the balance sheet date.

For impaired equity method investments that management does not plan

to sell prior to recovery of value and is not likely to be required to sell, the

evaluation of whether an impairment is other-than-temporary is based on

(i) whether and when an equity method investment will recover in value and

(ii) whether the investor has the intent and ability to hold that investment for

a period of time sufficient to recover the value. The determination of whether

the impairment is considered other-than-temporary is based on all of the

following indicators, regardless of the time and extent of impairment:

• cause of the impairment and the financial condition and near-term

prospects of the issuer, including any specific events that may influence

the operations of the issuer;

• intent and ability to hold the investment for a period of time sufficient to

allow for any anticipated recovery in market value; and

• length of time and extent to which fair value has been less than the

carrying value.

The sections below describe current circumstances related to certain of

the Company’s significant equity method investments, specific impairments

and the Company’s process for identifying credit-related impairments

in its security types with the most significant unrealized losses as of

December 31, 2013.

Akbank

In March 2012, Citi decided to reduce its ownership interest in Akbank T.A.S.,

an equity investment in Turkey (Akbank), to below 10%. As of March 31,

2012, Citi held a 20% equity interest in Akbank, which it purchased in

January 2007, accounted for as an equity method investment. As a result of

its decision to sell its share holdings in Akbank, in the first quarter of 2012

Citi recorded an impairment charge related to its total investment in Akbank

amounting to approximately $1.2 billion pretax ($763 million after-tax).

This impairment charge was primarily driven by the recognition of all

net investment foreign currency hedging and translation losses previously

reflected in AOCI, as well as a reduction in the carrying value of the

investment to reflect the market price of Akbank’s shares. The impairment

charge was recorded in OTTI losses on investments in the Consolidated

Statement of Income. During the second quarter of 2012, Citi sold a 10.1%

stake in Akbank, resulting in a loss on sale of $424 million ($274 million