Citibank 2013 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

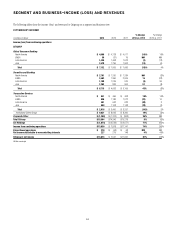

19

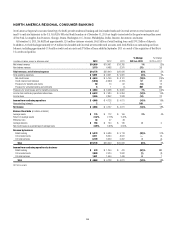

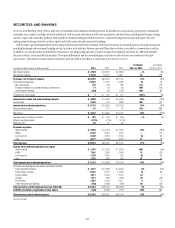

2013 vs. 2012

Net income decreased 14%, mainly driven by lower revenues and lower loan

loss reserve releases, partially offset by lower net credit losses and expenses.

Revenues decreased 6% primarily due to lower retail banking revenues.

Retail banking revenues of $5.4 billion declined 20% due to lower mortgage

origination revenues driven by the significantly lower U.S. mortgage

refinancing activity, particularly during the second half of 2013 due to higher

interest rates. In addition, retail banking continued to experience ongoing

spread compression in the deposit portfolios within the consumer and

commercial banking businesses. Partially offsetting the spread compression

was growth in average deposits (8%), average commercial loans (15%)

and average retail loans (3%). While Citi believes mortgage revenues may

have broadly stabilized as of year-end 2013, retail banking revenues will

likely continue to be negatively impacted in 2014 by the lower mortgage

origination revenues and spread compression in the deposit portfolios.

Cards revenues increased 1%. In Citi-branded cards, revenues were

unchanged at $8.2 billion as continued improvement in net interest spreads,

reflecting higher yields as promotional balances represented a smaller

percentage of the portfolio total as well as lower funding costs, were offset

by a 5% decline in average loans. Citi-branded cards net interest revenue

increased 1%, reflecting the higher yields and lower cost of funds, partially

offset by the decline in average loans and a continued increased payment

rate from consumer deleveraging. Citi-branded cards non-interest revenue

declined 5% due to higher affinity rebates.

Citi retail services revenues increased 3% primarily due to the acquisition

of the Best Buy portfolio, partially offset by declining non-interest revenues,

driven by improving credit and the resulting impact on contractual partner

payments. Citi retail services net interest revenues increased 6% driven by a

4% increase in average loans, primarily due to the Best Buy U.S. portfolio

acquisition, although net interest spreads declined as the percentage of

promotional balances within the portfolio increased and could continue to

increase into 2014. Total card purchase sales of $240 billion increased 3%

from the prior year, with 3% growth in Citi-branded cards and 5% growth in

retail services. Citi expects cards revenues could continue to be negatively

impacted by higher payment rates for consumers, reflecting the relatively

slow economic recovery and deleveraging as well as Citi’s shift to higher

credit quality borrowers.

Expenses decreased 3%, primarily due to lower legal and related costs

and repositioning savings, partially offset by higher-mortgage origination

costs in the first half of 2013 and expenses in cards as a result of the Best Buy

portfolio acquisition during the second half of the year.

Provisions increased 7%, as lower net credit losses in the Citi-branded

cards and Citi retail services portfolios were offset by continued lower loan

loss reserve releases ($1.0 billion in 2013 compared to $2.4 billion in 2012),

primarily related to cards, as well as reserve builds for new loans originated

in the Best Buy portfolio during the latter part of 2013, which are expected to

continue into 2014.

2012 vs. 2011

Net income increased 18%, mainly driven by higher mortgage revenues in

retail banking and a decline in net credit losses, partially offset by a reduction

in loan loss reserve releases.

Revenues increased 5%, driven by a 38% increase in retail banking

mortgage revenues resulting from the high level of U.S. refinancing activity

as well as higher margins resulting from the shift to retail as compared to

third-party origination channels. Excluding mortgages, revenue from the

retail banking business was essentially unchanged, as volume growth and

improved mix in the deposit and lending portfolios within the consumer and

commercial portfolios were offset by significant spread compression.

Cards revenues declined 4%. In Citi-branded cards, both average loans

and net interest revenue declined year-over-year, reflecting continued

increased payment rates resulting from consumer deleveraging and the

impact of the look-back provisions of The Credit Card Accountability

Responsibility and Disclosure Act (CARD Act). In Citi retail services, net

interest revenues improved slightly but were offset by declining non-interest

revenues, driven by improving credit and the resulting impact on contractual

partner payments.

Expenses increased 2%, primarily due to increased mortgage origination

costs resulting from the higher retail channel mortgage volumes and $100

million of repositioning charges in the fourth quarter of 2012 as well as

higher legal and related costs, partially offset by lower expenses in cards.

Provisions decreased 14%, due to a 29% decline in net credit losses,

primarily in the cards portfolios, partly offset by lower loan loss reserve

releases ($2.4 billion in 2012 compared to $4.2 billion in 2011).