Citibank 2013 Annual Report Download - page 286

Download and view the complete annual report

Please find page 286 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

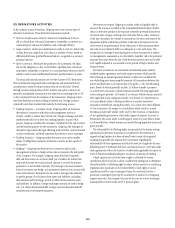

268

payments to the buyer upon the occurrence of predefined credit events

(commonly referred to as “settlement triggers”). These settlement triggers

are defined by the form of the derivative and the reference credit and are

generally limited to the market standard of failure to pay on indebtedness

and bankruptcy of the reference credit and, in a more limited range of

transactions, debt restructuring. Credit derivative transactions referring to

emerging market reference credits will also typically include additional

settlement triggers to cover the acceleration of indebtedness and the risk of

repudiation or a payment moratorium. In certain transactions, protection

may be provided on a portfolio of reference credits or asset-backed securities.

The seller of such protection may not be required to make payment until a

specified amount of losses has occurred with respect to the portfolio and/or

may only be required to pay for losses up to a specified amount.

The Company is a market maker and trades a range of credit derivatives.

Through these contracts, the Company either purchases or writes protection

on either a single name or a portfolio of reference credits. The Company

also uses credit derivatives to help mitigate credit risk in its Corporate and

Consumer loan portfolios and other cash positions, and to facilitate client

transactions.

The range of credit derivatives sold includes credit default swaps, total

return swaps, credit options and credit-linked notes.

A credit default swap is a contract in which, for a fee, a protection seller

agrees to reimburse a protection buyer for any losses that occur due to

a credit event on a reference entity. If there is no credit default event or

settlement trigger, as defined by the specific derivative contract, then the

protection seller makes no payments to the protection buyer and receives only

the contractually specified fee. However, if a credit event occurs as defined in

the specific derivative contract sold, the protection seller will be required to

make a payment to the protection buyer.

A total return swap transfers the total economic performance of a

reference asset, which includes all associated cash flows, as well as capital

appreciation or depreciation. The protection buyer receives a floating rate of

interest and any depreciation on the reference asset from the protection seller

and, in return, the protection seller receives the cash flows associated with

the reference asset plus any appreciation. Thus, according to the total return

swap agreement, the protection seller will be obligated to make a payment

any time the floating interest rate payment and any depreciation of the

reference asset exceed the cash flows associated with the underlying asset. A

total return swap may terminate upon a default of the reference asset subject

to the provisions of the related total return swap agreement between the

protection seller and the protection buyer.

A credit option is a credit derivative that allows investors to trade or hedge

changes in the credit quality of the reference asset. For example, in a credit

spread option, the option writer assumes the obligation to purchase or sell the

reference asset at a specified “strike” spread level. The option purchaser buys

the right to sell the reference asset to, or purchase it from, the option writer at

the strike spread level. The payments on credit spread options depend either

on a particular credit spread or the price of the underlying credit-sensitive

asset. The options usually terminate if the underlying assets default.

A credit-linked note is a form of credit derivative structured as a debt

security with an embedded credit default swap. The purchaser of the note

writes credit protection to the issuer and receives a return that could be

negatively affected by credit events on the underlying reference credit. If

the reference entity defaults, the purchaser of the credit-linked note may

assume the long position in the debt security and any future cash flows

from it but will lose the amount paid to the issuer of the credit-linked note.

Thus, the maximum amount of the exposure is the carrying amount of the

credit-linked note. As of December 31, 2013 and December 31, 2012, the

amount of credit-linked notes held by the Company in trading inventory was

immaterial.

The following tables summarize the key characteristics of the Company’s

credit derivative portfolio as protection seller as of December 31, 2013 and

December 31, 2012:

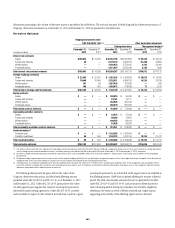

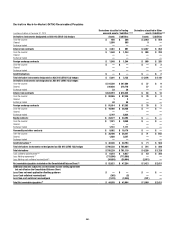

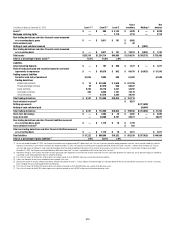

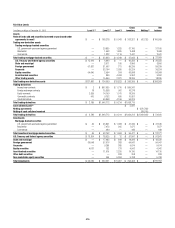

In millions of dollars at

December 31, 2013

Maximum potential

amount of

future payments

Fair

value

payable (1)(2)

By industry/counterparty

Bank $ 727,748 $ 6,520

Broker-dealer 224,073 4,001

Non-financial 2,820 56

Insurance and other financial institutions 188,722 2,059

Total by industry/counterparty $1,143,363 $12,636

By instrument

Credit default swaps and options $1,141,864 $12,607

Total return swaps and other 1,499 29

Total by instrument $1,143,363 $12,636

By rating

Investment grade $ 546,011 $ 2,385

Non-investment grade 170,789 7,408

Not rated 426,563 2,843

Total by rating $1,143,363 $12,636

By maturity

Within 1 year $ 221,562 $ 858

From 1 to 5 years 853,391 7,492

After 5 years 68,410 4,286

Total by maturity $1,143,363 $12,636

(1) In addition, fair value amounts payable under credit derivatives purchased were $28,723 million.

(2) In addition, fair value amounts receivable under credit derivatives sold were $26,673 million.