Citibank 2013 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

88

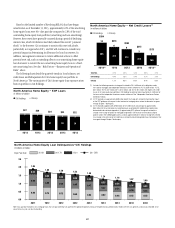

As evidenced by the tables above, home equity loan net credit losses

and delinquencies improved during 2013, including fewer loans entering

the 30-89 days past due delinquency bucket, primarily due to continued

modifications and liquidations. Given the lack of a market in which to sell

delinquent home equity loans, as well as the relatively smaller number of

home equity loan modifications and modification programs (see Note 15 to

the Consolidated Financial Statements), Citi’s ability to reduce delinquencies

or net credit losses in its home equity loan portfolio in Citi Holdings, whether

pursuant to deterioration of the underlying credit performance of these loans

or otherwise, is more limited as compared to residential first mortgages.

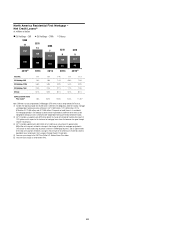

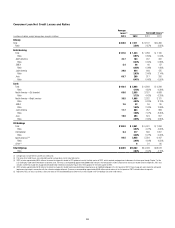

North America Home Equity Loans—State Delinquency Trends

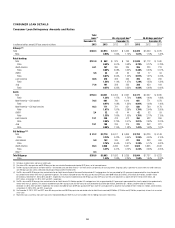

The following tables set forth, for total Citigroup, the six states and/or regions with the highest concentration of Citi’s home equity loans as of

December 31, 2013 and December 31, 2012.

In billions of dollars December 31, 2013 December 31, 20112

State (1) ENR (2)

ENR

Distribution

90+DPD

%

%

CLTV >

100% (3)

Refreshed

FICO ENR (2)

ENR

Distribution

90+DPD

%

%

CLTV >

100% (3)

Refreshed

FICO

CA $ 8.2 28% 1.6% 17% 726 $ 9.7 28% 2.0% 40% 723

NY/NJ/CT (4) 7.2 24 2.3 12 718 8.2 23 2.3 20 715

FL (4) 2.1 7 2.9 44 704 2.4 7 3.4 58 698

IL (4) 1.2 4 1.6 42 713 1.4 4 2.1 55 708

IN/OH/MI (4) 1.0 3 1.6 47 686 1.2 3 2.2 55 679

AZ/NV 0.7 2 2.1 53 713 0.8 2 3.1 70 709

Other 9.5 32 1.7 26 699 11.5 33 2.2 37 695

Total $29.9 100% 1.9% 23% 712 $35.2 100% 2.3% 37% 704

Note: Totals may not sum due to rounding.

(1) Certain of the states are included as part of a region based on Citi’s view of similar HPI within the region.

(2) Ending net receivables. Excludes loans in Canada and Puerto Rico and loans subject to LTSCs. Excludes balances for which FICO or LTV data are unavailable.

(3) Represents combined loan-to-value (CLTV) for both residential first mortgages and home equity loans.

(4) New York, New Jersey, Connecticut, Indiana, Ohio, Florida and Illinois are judicial states.

Citi’s home equity portfolio is primarily concentrated in California and

the New York/New Jersey/Connecticut region (with New York the largest of

the three states). The significant improvement in refreshed CLTV percentages

as of December 31, 2013 were primarily the result of improvements in HPI

in these states/regions, thereby increasing values used in the determination

of CLTV.

National Mortgage Settlement

Under the national mortgage settlement, entered into by Citi and other

financial institutions in February 2012, Citi agreed to provide customer

relief in the form of loan modifications for delinquent borrowers, including

principal reductions, and other loss mitigation activities, and refinancing

concessions to enable current borrowers whose properties are worth less

than the balance of their loans to reduce their interest rates. Citi believes

it has fulfilled its requirement for the loan modification remediation and

refinancing concessions under the settlement. The results are pending review

and certification of the monitor required by the settlement, which is not

expected to be completed until the first half of 2014.

Independent Foreclosure Review Settlement

As of December 31, 2013, Citi continues to fulfill its mortgage assistance

obligations under the independent foreclosure review settlement, entered into

by Citi and other major mortgage servicers in January 2013, and estimates

it will incur additional net credit losses of approximately $25 million per

quarter through the first half of 2014. Citi continues to believe its loan loss

reserve as of December 31, 2013 will be sufficient to cover any mortgage

assistance under the settlement.