Citibank 2013 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

42

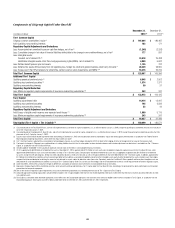

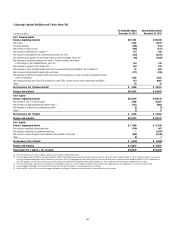

CAPITAL RESOURCES

Overview

Capital is used principally to support assets in Citi’s businesses and to

absorb credit, market and operational losses. Citi primarily generates capital

through earnings from its operating businesses. Citi may augment its capital

through issuances of common stock, perpetual preferred stock and equity

issued through awards under employee benefit plans, among other issuances.

During 2013, Citi issued approximately $4.3 billion of noncumulative

perpetual preferred stock, resulting in a total of approximately $6.7 billion

outstanding as of December 31, 2013.

Citi has also previously augmented its regulatory capital through

the issuance of trust preferred securities, although the treatment of such

instruments as regulatory capital will largely be phased out under the

final U.S. Basel III rules (Final Basel III Rules) (see “Regulatory Capital

Standards Developments” below). Accordingly, Citi has continued to redeem

certain of its trust preferred securities in contemplation of such future phase

out (see “Managing Global Risk—Market Risk—Funding and Liquidity—

Long-Term Debt” below).

Further, changes in regulatory and accounting standards as well as the

impact of future events on Citi’s business results, such as corporate and asset

dispositions, may also affect Citi’s capital levels.

Citigroup’s capital management framework is designed to ensure that

Citigroup and its principal subsidiaries maintain sufficient capital consistent

with each entity’s respective risk profile and all applicable regulatory

standards and guidelines. Citi assesses its capital adequacy against a series

of internal quantitative capital goals, designed to evaluate the Company’s

capital levels in expected and stressed economic environments. Underlying

these internal quantitative capital goals are strategic capital considerations,

centered on preserving and building financial strength. Senior management,

with oversight from the Board of Directors, is responsible for the capital

assessment and planning process, which is integrated into Citi’s capital plan,

as part of the Federal Reserve Board’s Comprehensive Capital Analysis and

Review (CCAR) process. Implementation of the capital plan is carried out

mainly through Citigroup’s Asset and Liability Committee, with oversight

from the Risk Management and Finance Committee of Citigroup’s Board of

Directors. Asset and liability committees are also established globally and for

each significant legal entity, region, country and/or major line of business.

Current Regulatory Capital Guidelines

Citigroup Capital Resources Under Current Regulatory

Guidelines

Citigroup is subject to the risk-based capital guidelines issued by the Federal

Reserve Board which currently constitute the Basel I credit risk capital

rules and also the final (revised) market risk capital rules (Basel II.5).

Commencing with 2014, Citi’s regulatory capital ratios will reflect, in part,

the implementation of certain aspects of the Final Basel III Rules, such as

those related to the transitioning toward qualifying capital components,

including the application of regulatory capital adjustments and deductions.

In addition, effective with the second quarter of 2014, Citi will begin applying

the Basel III Advanced Approaches rules. For additional information

regarding the implementation of the Final Basel III Rules, see “Regulatory

Capital Standards Developments” below.

Historically, capital adequacy has been measured, in part, based on

two risk-based capital ratios, the Tier 1 Capital and Total Capital (Tier 1

Capital + Tier 2 Capital) ratios. Tier 1 Capital consists of the sum of “core

capital elements,” such as qualifying common stockholders’ equity, as

adjusted, qualifying perpetual preferred stock, qualifying noncontrolling

interests, and qualifying trust preferred securities, principally reduced by

goodwill, other disallowed intangible assets, and disallowed deferred tax

assets. Total Capital also includes “supplementary” Tier 2 Capital elements,

such as qualifying subordinated debt and a limited portion of the allowance

for credit losses. Both measures of capital adequacy are stated as a percentage

of risk-weighted assets.

In 2009, the U.S. banking regulators developed a supervisory measure

of capital termed “Tier 1 Common,” which is defined as Tier 1 Capital less

non-common elements, including qualifying perpetual preferred stock,

qualifying noncontrolling interests, and qualifying trust preferred securities.

Until January 1, 2015, the Federal Reserve Board has retained this definition

of Tier 1 Common Capital for CCAR purposes, which differs substantially

from the more restrictive definition under the Final Basel III Rules. Moreover,

the presentation of Tier 1 Common Capital and related ratio in the tables

that follow, labeled “Current Regulatory Guidelines”, are also consistent in

derivation with this supervisory definition.