Citibank 2013 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

95

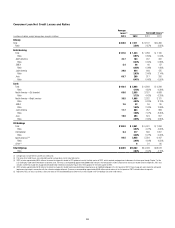

CORPORATE CREDIT DETAILS

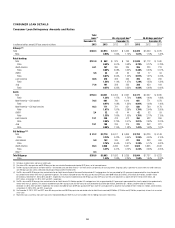

Consistent with its overall strategy, Citi’s Corporate clients are typically large,

multi-national corporations who value Citi’s global network. Citi aims to

establish relationships with these clients that encompass multiple products,

consistent with client needs, including cash management and trade services,

foreign exchange, lending, capital markets and M&A advisory.

For corporate clients and investment banking activities across Citi, the

credit process is grounded in a series of fundamental policies, in addition

to those described under “Managing Global Risk—Risk Management—

Overview” above. These include:

• joint business and independent risk management responsibility for

managing credit risks;

• a single center of control for each credit relationship, which coordinates

credit activities with each client;

• portfolio limits to ensure diversification and maintain risk/capital

alignment;

• a minimum of two authorized credit officer signatures required on most

extensions of credit, one of which must be from a credit officer in credit

risk management;

• risk rating standards, applicable to every obligor and facility; and

• consistent standards for credit origination documentation and remedial

management.

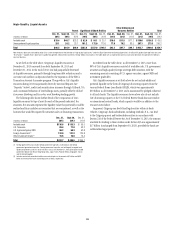

Corporate Credit Portfolio

The following table represents the Corporate credit portfolio (excluding

Private Bank in Securities and Banking), before consideration of

collateral or hedges, by remaining tenor at December 31, 2013 and 2012.

The Corporate credit portfolio includes loans and unfunded lending

commitments in Citi’s institutional client exposure in Institutional

Client Group and, to a much lesser extent, Citi Holdings, by Citi’s internal

management hierarchy and is broken out by (i) direct outstandings, which

include drawn loans, overdrafts, bankers’ acceptances and leases, and

(ii) unfunded lending commitments, which include unused commitments to

lend, letters of credit and financial guarantees.

At December 31, 2013 At December 31, 2012

In billions of dollars

Due

within

1 year

Greater

than 1 year

but within

5 years

Greater

than

5 years

Total

Exposure

Due

within

1 year

Greater

than 1 year

but within

5 years

Greater

than

5 years

Total

exposure

Direct outstandings $108 $ 80 $29 $217 $ 93 $ 76 $28 $196

Unfunded lending commitments 87 204 21 312 88 199 28 315

Total $195 $284 $50 $529 $181 $275 $56 $511

Portfolio Mix—Geography, Counterparty and Industry

Citi’s Corporate credit portfolio is diverse across geography and counterparty.

The following table shows the percentage of direct outstandings and

unfunded lending commitments by region based on Citi’s internal

management geography:

December 31,

2013

December 31,

2012

North America 51% 52%

EMEA 27 27

Asia 14 14

Latin America 87

Total 100% 100%

The maintenance of accurate and consistent risk ratings across the Corporate

credit portfolio facilitates the comparison of credit exposure across all lines

of business, geographic regions and products. Counterparty risk ratings

reflect an estimated probability of default for a counterparty and are derived

primarily through the use of validated statistical models, scorecard models

and external agency ratings (under defined circumstances), in combination

with consideration of factors specific to the obligor or market, such as

management experience, competitive position and regulatory environment.

Facility risk ratings are assigned that reflect the probability of default of

the obligor and factors that affect the loss-given-default of the facility, such

as support or collateral. Internal obligor ratings that generally correspond

to BBB and above are considered investment grade, while those below are

considered non-investment grade.

Citigroup also has incorporated climate risk assessment and reporting

criteria for certain obligors, as necessary. Factors evaluated include

consideration of climate risk to an obligor’s business and physical assets and,

when relevant, consideration of cost-effective options to reduce greenhouse

gas emissions.