Citibank 2013 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

100

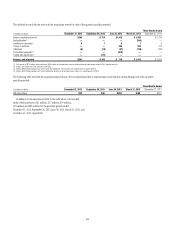

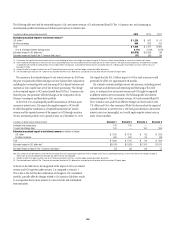

Deposits

Deposits are the primary and lowest cost funding source for Citi’s bank

subsidiaries. The table below sets forth the end of period deposits, by business

and/or segment, and the total average deposits for each of the periods

indicated.

In billions of dollars

Dec. 31,

2013

Sept. 30,

2013

Dec. 31,

2012

Global Consumer Banking

North America $170.2 $168.6 $165.2

EMEA 13.1 12.5 13.2

Latin America 47.7 47.5 48.6

Asia 101.4 101.6 110.0

Total $332.4 $330.2 $337.0

ICG

Securities and Banking $110.1 $112.6 $114.4

Transaction Services 463.7 452.8 408.7

Total $573.8 $565.4 $523.1

Corporate/Other 26.1 18.0 2.5

Total Citicorp $932.3 $913.6 $862.6

Total Citi Holdings (1) 36.0 41.8 68.0

Total Citigroup Deposits (EOP) $968.3 $955.4 $930.6

Total Citigroup Deposits (AVG) $956.4 $922.1 $928.9

(1) Included within Citi’s end-of-period deposit balance as of December 31, 2013 were approximately

$30 billion of deposits related to Morgan Stanley Smith Barney (MSSB) customers that, as previously

disclosed, will be transferred to Morgan Stanley, with remaining balances transferred in the amount of

approximately $5 billion per quarter through the end of the second quarter of 2015.

End-of-period deposits increased 4% year-over-year and 1% quarter-

over-quarter. The increase during 2013 reflected, in part, elevated levels of

market liquidity and strong corporate balance sheets, but also was driven by

underlying business growth.

Global Consumer Banking deposits decreased 1% year-over-year, as growth

in consumer checking and savings balances was offset by reductions in Citi’s

higher cost time deposits. Corporate deposits increased 10% year-over-year, as

continued strong deposit flows led to 13% growth in Transaction Services. This

deposit growth in Transaction Services was offset by a 4% decline in Securities

and Banking deposits driven by reduced deposit balances with counterparties

in Citi’s Markets businesses, while deposits increased in the Private Bank.

Corporate/Other deposits also increased year-over-year as Citi issued tenored

time deposits to further diversify its funding sources.

Average deposits increased 3% year-over-year and 4% quarter-over-quarter,

despite the transfer of approximately $26 billion of deposits relating to MSSB

to Morgan Stanley during the second half of 2013.

Operating balances represented 80% of Citicorp’s total deposit base as

of December 31, 2013, compared to 79% at September 30, 2013 and 78%

at December 31, 2012. Citi defines operating balances as checking and

savings accounts for individuals, as well as cash management accounts

for corporations; by comparison, time deposits have fixed rates for the

term of the deposit and generally lower margins. This shift to operating

balances, combined with overall market conditions and prevailing interest

rates, continued to reduce Citi’s cost of deposits during 2013. Excluding the

impact of FDIC assessments and deposit insurance, the average rate on Citi’s

total deposits was 0.50% at December 31, 2013, compared with 0.53% at

September 30, 2013, and 0.65% at December 31, 2012.

Long-Term Debt

Long-term debt (generally defined as original maturities of one year or

more) continued to represent the most significant component of Citi’s

funding for the parent entities and was a supplementary source of funding

for the bank.

Long-term debt is an important funding source for Citi’s parent

entities due in part to its multi-year maturity structure. The weighted-

average maturities of unsecured long-term debt issued by Citigroup and

its affiliates (including Citibank, N.A.) with a remaining life greater than

one year (excluding remaining trust preferred securities outstanding) was

approximately 7.0 years as of December 31, 2013, roughly unchanged from

the prior quarter and prior-year periods.

Citi’s long-term debt outstanding includes benchmark debt and what

Citi refers to as customer-related debt, consisting of structured notes, such

as equity- and credit-linked notes, as well as non-structured notes. Citi’s

issuance of customer-related debt is generally driven by customer demand

and supplements benchmark debt issuance as a source of funding for Citi’s

parent entities.