Citibank 2013 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

82

North America Consumer Mortgage Lending

Overview

Citi’s North America Consumer mortgage portfolio consists of both

residential first mortgages and home equity loans. At December 31, 2013,

Citi’s North America Consumer residential first mortgage portfolio was

$75.9 billion (compared to $88.2 billion at December 31, 2012), while the

home equity loan portfolio was $31.6 billion (compared to $37.2 billion at

December 31, 2012). At December 31, 2013, $44.6 billion of first mortgages

was recorded in Citi Holdings, with the remaining $31.3 billion recorded

in Citicorp. At December 31, 2013, $28.7 billion of home equity loans

was recorded in Citi Holdings, with the remaining $2.9 billion recorded

in Citicorp.

Citi’s residential first mortgage portfolio included $7.7 billion of loans

with FHA insurance or VA guarantees at December 31, 2013, compared to

$8.5 billion at December 31, 2012. This portfolio consists of loans to low-to-

moderate-income borrowers with lower FICO (Fair Isaac Corporation) scores

and generally has higher loan-to-value ratios (LTVs). Credit losses on FHA

loans are borne by the sponsoring governmental agency, provided that the

insurance terms have not been rescinded as a result of an origination defect.

With respect to VA loans, the VA establishes a loan-level loss cap, beyond

which Citi is liable for loss. While FHA and VA loans have high delinquency

rates, given the insurance and guarantees, respectively, Citi has experienced

negligible credit losses on these loans.

In addition, Citi’s residential first mortgage portfolio included $1.1 billion

of loans with origination LTVs above 80% that have insurance through

mortgage insurance companies at December 31, 2013, compared to

$1.5 billion at December 31, 2012. At December 31, 2013, the residential

first mortgage portfolio also had $0.8 billion of loans subject to long-term

standby commitments (LTSCs) with U.S. government-sponsored entities

(GSEs) for which Citi has limited exposure to credit losses, compared to

$1.0 billion at December 31, 2012. Citi’s home equity loan portfolio also

included $0.3 billion of loans subject to LTSCs with GSEs (compared to

$0.4 billion at December 31, 2012) for which Citi also has limited exposure

to credit losses. These guarantees and commitments may be rescinded in the

event of loan origination defects. Citi’s allowance for loan loss calculations

takes into consideration the impact of the guarantees and commitments

described above.

Citi does not offer option-adjustable rate mortgages/negative-amortizing

mortgage products to its customers. As a result, option-adjustable rate

mortgages/negative-amortizing mortgages represent an insignificant portion

of total balances, since they were acquired only incidentally as part of prior

portfolio and business purchases.

As of December 31, 2013, Citi’s North America residential first mortgage

portfolio contained approximately $5.0 billion of adjustable rate mortgages

that are currently required to make a payment only of accrued interest for

the payment period, or an interest-only payment, compared to $7.7 billion

at December 31, 2012. This decline resulted primarily from repayments of

$1.2 billion, conversions to amortizing loans of $1.0 billion and asset sales of

$0.4 billion. Borrowers who are currently required to make an interest-only

payment cannot select a lower payment that would negatively amortize the

loan. Residential first mortgages with this payment feature are primarily

to high-credit-quality borrowers who have on average significantly higher

origination and refreshed FICO scores than other loans in the residential first

mortgage portfolio, and have exhibited significantly lower 30+ delinquency

rates as compared with residential first mortgages without this payment

feature. As such, Citi does not believe the residential mortgage loans with this

payment feature represent substantially higher risk in the portfolio.

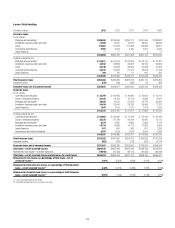

North America Consumer Mortgage Quarterly Credit Trends—Net Credit

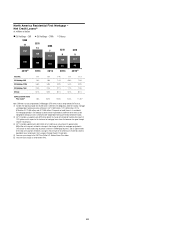

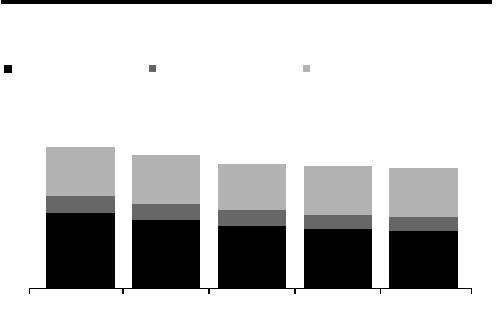

Losses and Delinquencies—Residential First Mortgages

The following charts detail the quarterly trends in loan balances, net credit

losses and delinquencies for Citigroup’s residential first mortgage portfolio in

North America. As set forth in the tables below, approximately 59% of Citi’s

residential first mortgage exposure arises from its portfolio in Citi Holdings,

which includes residential first mortgages originated by both CitiMortgage as

well as Citi’s legacy CitiFinancial North America business.

4Q’133Q’132Q’131Q’134Q’12

47

11

31

43

10

31

39

10

29

37

9

31

36

9

31

North America Residential First Mortgage — EOP Loans

In billions of dollars

Citi Holdings - CMI Citi Holdings - CFNA Citicorp

$88 $84 $78 $76

$77