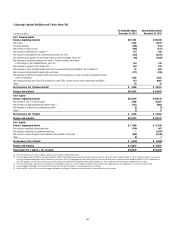

Citibank 2013 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

60

securitization and, in certain transactions, a retention requirement by

securitizers of an unhedged exposure to at least 5% of the economic risk

of the securitized assets. Regulations implementing these provisions have

been proposed but in many cases have not yet been adopted. The SEC also

has proposed additional extensive regulation of both publicly and privately

offered securitization transactions through revisions to the registration,

disclosure and reporting requirements for asset-backed securities and other

structured finance products. Moreover, the final U.S. Basel III capital rules

will increase the capital required to be held by Citi against various exposures

to securitizations.

The cumulative effect of these extensive regulatory changes, as well as

other potential future regulatory changes, cannot currently be assessed.

It is likely, however, that these various measures will increase the costs or

decrease the attractiveness of executing certain securitization transactions,

and could effectively limit Citi’s overall volume of, and the role Citi may play

in, securitizations and make it impractical for Citi to execute certain types

of securitization transactions it previously executed. As a result, these effects

could impair Citi’s ability to continue to earn income from these transactions

or could hinder Citi’s ability to use such transactions to hedge risks, reduce

exposures or reduce assets with adverse risk-weighting in its businesses,

and those consequences could affect the conduct of these businesses. In

addition, certain sectors of the securitization markets, particularly residential

mortgage-backed securitizations, have been inactive or experienced

dramatically diminished transaction volumes since the financial crisis.

The impact of various regulatory reform measures could adversely impact

any future recovery of these sectors of the securitization markets and, thus,

the opportunities for Citi to participate in securitization transactions in

such sectors.

MARKET AND ECONOMIC RISKS

The Continued Uncertainty Relating to the Sustainability

and Pace of Economic Recovery in the U.S. and Globally,

Including in the Emerging Markets, Could Have a Negative

Impact on Citi’s Businesses and Results of Operations.

Moreover, Any Significant Global Economic Downturn or

Disruption, Including a Significant Decline in Global Trade

Volumes, Could Materially and Adversely Impact Citi’s

Businesses, Results of Operations and Financial Condition.

Citi’s businesses have been, and could continue to be, negatively impacted by

the uncertainty surrounding the sustainability and pace of economic recovery

in the U.S., as well as globally. Fiscal and monetary actions taken by U.S. and

non-U.S. government and regulatory authorities to spur economic growth

or otherwise, including by maintaining or increasing interest rates, can also

impact Citi’s businesses and results of operations. For example, changing

expectations regarding the Federal Reserve Board’s tapering of quantitative

easing has impacted market and customer activity as well as trading volumes

which has negatively impacted the results of operations for Securities and

Banking, and could continue to do so in the future.

Additionally, given its global focus, Citi could be disproportionately

impacted as compared to its competitors by any impact of government or

regulatory policies or economic conditions in the international and/or

emerging markets (which Citi generally defines as the markets in Asia

(other than Japan, Australia and New Zealand), the Middle East, Africa and

central and eastern European countries in EMEA and the markets in Latin

America). Countries such as India, Singapore, Hong Kong, Brazil and China,

each of which are part of Citi’s emerging markets strategy, have recently

experienced uncertainty over the potential impact of further tapering by the

Federal Reserve Board and/or the extent of future economic growth. Actual

or perceived impacts or a slowdown in growth in these and other emerging

markets could negatively impact Citi’s businesses and results of operations.

Further, if a particular country’s economic situation were to deteriorate below

a certain level, U.S. regulators could impose mandatory loan loss and other

reserve requirements on Citi, which could negatively impact its earnings,

perhaps significantly.

Moreover, if a severe global economic downturn or other major economic

disruption were to occur, including a significant decline in global trade

volumes, Citi would likely experience substantial loan and other losses and

be required to significantly increase its loan loss reserves, among other

impacts. A global trade disruption that results in a permanently reduced

level of trade volumes and increased costs of global trade, whether as a

result of a prolonged “trade war” or some other reason, could significantly

impact trade financing activities, certain trade dependent economies (such

as the emerging markets in Asia), and certain industries heavily dependent

on trade, among other things. Given Citi’s global strategy and focus on the

emerging markets, such a downturn and decrease in global trade volumes

could materially and adversely impact Citi’s businesses, results of operation

and financial condition, particularly as compared to its competitors. This

could include, among other things, the potential that a portion of any such

losses would not be tax benefitted, given the current environment.

Concerns About the Level of U.S. Government Debt and

a Downgrade (or a Further Downgrade) of the U.S.

Government Credit Rating Could Negatively Impact Citi’s

Businesses, Results of Operations, Capital, Funding

and Liquidity.

Concerns about the overall level of U.S. government debt and/or a U.S.

government default, as well as uncertainty relating to actions that may or

may not be taken to address these and related issues, have adversely affected,

and could continue to adversely affect, U.S. and global financial markets,

economic conditions and Citi’s businesses and results of operations.

The credit rating agencies have also expressed concerns about these issues

and have taken actions to downgrade and/or place the long-term sovereign

credit rating of the U.S. government on negative outlook. A future downgrade