Citibank 2013 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2013 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

|

|

186

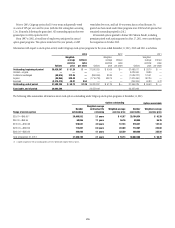

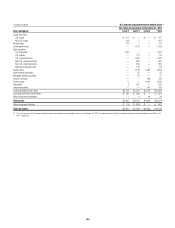

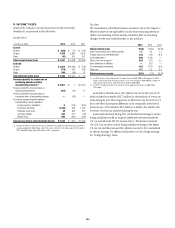

Discount Rate

The discount rates for the U.S. pension and postretirement plans were selected

by reference to a Citigroup-specific analysis using each plan’s specific

cash flows and compared with high-quality corporate bond indices for

reasonableness. Citigroup’s policy is to round to the nearest five hundredths

of a percent. The discount rates for the non-U.S. pension and postretirement

plans are selected by reference to high-quality corporate bond rates in

countries that have developed corporate bond markets. However, where

developed corporate bond markets do not exist, the discount rates are selected

by reference to local government bond rates with a premium added to reflect

the additional risk for corporate bonds in certain countries.

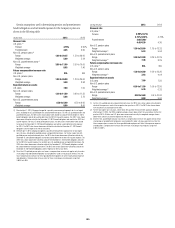

Expected Rate of Return

The Company determines its assumptions for the expected rate of return

on plan assets for its U.S. pension and postretirement plans using a

“building block” approach, which focuses on ranges of anticipated rates

of return for each asset class. A weighted average range of nominal rates

is then determined based on target allocations to each asset class. Market

performance over a number of earlier years is evaluated covering a wide

range of economic conditions to determine whether there are sound reasons

for projecting any past trends.

The Company considers the expected rate of return to be a long-term

assessment of return expectations and does not anticipate changing this

assumption unless there are significant changes in investment strategy

or economic conditions. This contrasts with the selection of the discount

rate and certain other assumptions, which are reconsidered annually in

accordance with generally accepted accounting principles.

The expected rate of return for the U.S. pension and postretirement plans

was 7.00% at December 31, 2013, 7.00% at December 31, 2012, and 7.50%

at December 31, 2011. The expected return on assets reflects the expected

annual appreciation of the plan assets and reduces the Company’s annual

pension expense. The expected return on assets is deducted from the sum

of service cost, interest cost and other components of pension expense to

arrive at the net pension (benefit) expense. Net pension (benefit) expense for

the U.S. pension plans for 2013, 2012 and 2011 reflects deductions of $863

million, $897 million and $890 million of expected returns, respectively.

The following table shows the expected rate of return used in determining the

Company’s pension expense compared to the actual rate of return on plan assets

during 2013, 2012 and 2011 for the U.S. pension and postretirement plans:

2013 2012 2011

Expected rate of return (1) 7.00% 7.50% 7.50%

Actual rate of return (2) 6.00% 11.00% 11.00%

(1) Effective December 31, 2012, the expected rate of return was changed from 7.50% to 7.00%.

(2) Actual rates of return are presented net of fees.

For the non-U.S. plans, pension expense for 2013 was reduced by the

expected return of $396 million, compared with the actual return of $(130)

million. Pension expense for 2012 and 2011 was reduced by expected returns

of $399 million and $422 million, respectively. Actual returns were lower in

2013, but higher in 2012 and 2011 than the expected returns in those years.

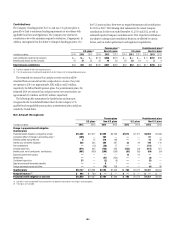

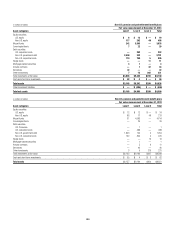

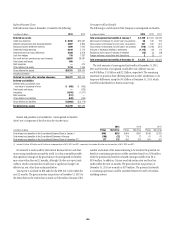

Sensitivities of Certain Key Assumptions

The following tables summarize the effect on pension expense of a one-

percentage-point change in the discount rate:

One-percentage-point increase

In millions of dollars 2013 2012 2011

U.S. plans $ 16 $ 18 $ 19

Non-U.S. plans (52) (48) (57)

One-percentage-point decrease

In millions of dollars 2013 2012 2011

U.S. plans $(57) $(36) $(34)

Non-U.S. plans 79 64 70

Since the U.S. qualified pension plan was frozen, the majority of the

prospective service cost has been eliminated and the gain/loss amortization

period was changed to the life expectancy for inactive participants. As a

result, pension expense for the U.S. qualified pension plan is driven more

by interest costs than service costs, and an increase in the discount rate

would increase pension expense, while a decrease in the discount rate would

decrease pension expense.

The following tables summarize the effect on pension expense of a one-

percentage-point change in the expected rates of return:

One-percentage-point increase

In millions of dollars 2013 2012 2011

U.S. plans $(123) $(120) $(118)

Non-U.S. plans (68) (64) (62)

One-percentage-point decrease

In millions of dollars 2013 2012 2011

U.S. plans $123 $ 120 $ 118

Non-U.S. plans 68 64 62

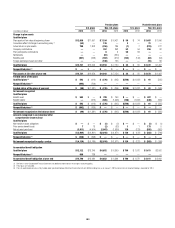

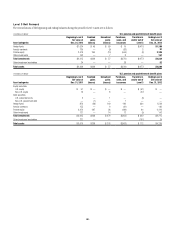

Health Care Cost-Trend Rate

Assumed health care cost-trend rates were as follows:

2013 2012

Health care cost increase rate for U.S. plans

Following year 8.00% 8.50%

Ultimate rate to which cost increase is assumed to decline 5.00 5.00

Year in which the ultimate rate is reached 2020 2020

A one-percentage-point change in assumed health care cost-trend rates

would have the following effects on postretirement expense:

One-

percentage-

point increase

One-

percentage-

point decrease

In millions of dollars 2013 2012 2013 2012

Effect on benefits earned and interest

cost for U.S. postretirement plans $ 1 $ 2 $ (1) $ (1)

Effect on accumulated postretirement benefit

obligation for U.S. postretirement plans 24 44 (19) (39)