Citibank 2010 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

93

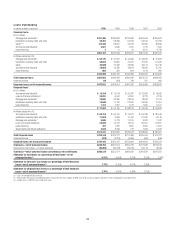

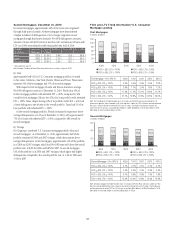

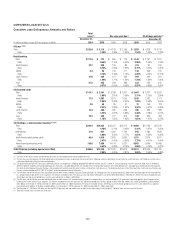

Citi’s first mortgage portfolio includes $9.3 billion of loans with FHA or VA

guarantees. These portfolios consist of loans originated to low-to-moderate-

income borrowers with lower FICO (Fair Isaac Corporation) scores and

generally have higher loan-to-value ratios (LTVs). Losses on FHA loans are

borne by the sponsoring agency, provided that the insurance has not been

breached as a result of an origination defect. The VA establishes a loan-level

loss cap, beyond which Citi is liable for loss. FHA and VA loans have high

delinquency rates but, given the guarantees, Citi has experienced negligible

credit losses on these loans. The first mortgage portfolio also includes

$1.8 billion of loans with LTVs above 80%, which have insurance through

private mortgage insurance (PMI) companies, and $1.7 billion of loans

subject to long-term standby commitments (LTSC), with U.S. government

sponsored entities (GSEs), for which Citi has limited exposure to credit losses.

Citi’s second mortgage portfolio also includes $0.6 billion of loans subject to

LTSCs with GSEs, for which Citi has limited exposure to credit losses. Citi’s

allowance for loan loss calculations take into consideration the impact of

these guarantees.

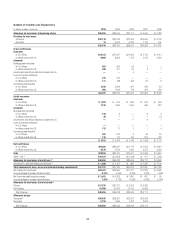

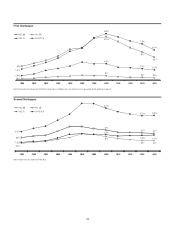

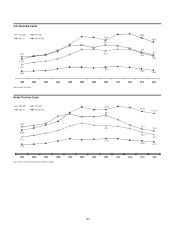

Consumer Mortgage Quarterly Trends—Delinquencies and

Net Credit Losses

The following charts detail the quarterly trends in delinquencies and

net credit losses for Citi’s first and second Consumer mortgage portfolios

in North America. As set forth in the charts below, net credit losses and

delinquencies of 90 days or more in both first and second mortgages

continued to improve during the fourth quarter of 2010. Citi continued to

manage down its first and second mortgage portfolios in Citi Holdings during

2010. The first mortgage portfolio in Citi Holdings was reduced by almost

20% to $80 billion, and the second mortgage portfolio by 14% to $44 billion,

each as of December 31, 2010. These reductions were achieved through a

combination of sales (first mortgages only), run-off and net credit losses.

For first mortgages, delinquencies of 90 days or more were down for the

fourth consecutive quarter. The sequential decline in delinquencies was due

entirely to asset sales and trial modifications converting into permanent

modifications, without which the delinquencies in first mortgages would

have been up slightly. During the full year 2010, Citi sold $4.8 billion in

delinquent mortgages. In addition, as of December 31, 2010, Citi had

converted a total of approximately $4.8 billion of trial modifications under

Citi’s loan modification programs to permanent modifications, more than

three-quarters of which were pursuant to the U.S. Treasury’s Home Affordable

Modification Program (HAMP).

For second mortgages, the net credit loss and delinquencies of 90 days or

more were relatively stable compared to the third quarter of 2010.

For information on Citi’s loan modification programs regarding

mortgages, see “Consumer Loan Modification Programs” below.