Citibank 2010 Annual Report Download - page 249

Download and view the complete annual report

Please find page 249 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

247

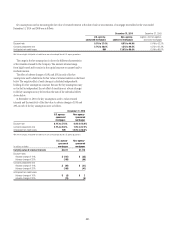

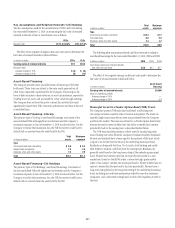

Key Assumptions and Retained Interests—Citi Holdings

The key assumptions, used for the securitization of CDOs and CLOs during

the year ended December 31, 2010, in measuring the fair value of retained

interests at the date of sale or securitization are as follows:

CDOs CLOs

Discount rate 14.7% to 40.6% 3.6% to 5.4%

The effect of two negative changes in discount rates used to determine the

fair value of retained interests is disclosed below.

In millions of dollars CDOs CLOs

Carrying value of retained interests $51 $618

Discount rates

Adverse change of 10% $ (3) $ (6)

Adverse change of 20% (6) (13)

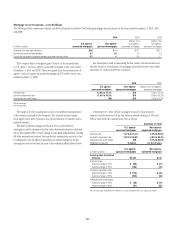

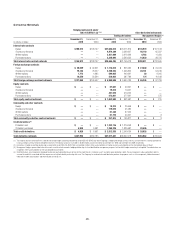

Asset-Based Financing

The Company provides loans and other forms of financing to VIEs that

hold assets. Those loans are subject to the same credit approvals as all

other loans originated or purchased by the Company. Financings in the

form of debt securities or derivatives are, in most circumstances, reported in

Trading account assets and accounted for at fair value through earnings.

The Company does not have the power to direct the activities that most

significantly impact these VIEs’ economic performance and thus it does not

consolidate them.

Asset-Based Financing—Citicorp

The primary types of Citicorp’s asset-based financings, total assets of the

unconsolidated VIEs with significant involvement and the Company’s

maximum exposure to loss at December 31, 2010 are shown below. For the

Company to realize that maximum loss, the VIE (borrower) would have to

default with no recovery from the assets held by the VIE.

In billions of dollars

Total

assets

Maximum

exposure

Type

Commercial and other real estate $ 0.9 $ 0.3

Hedge funds and equities 7.6 3.0

Airplanes, ships and other assets 7.6 7.9

Total $16.1 $11.2

Asset-Based Financing—Citi Holdings

The primary types of Citi Holdings’ asset-based financings, total assets of

the unconsolidated VIEs with significant involvement and the Company’s

maximum exposure to loss at December 31, 2010 are shown below. For the

Company to realize that maximum loss, the VIE (borrower) would have to

default with no recovery from the assets held by the VIE.

In billions of dollars

Total

assets

Maximum

exposure

Type

Commercial and other real estate $12.2 $1.7

Corporate loans 6.0 5.0

Airplanes, ships and other assets 4.4 2.2

Total $22.6 $8.9

The following table summarizes selected cash flow information related to

asset-based financings for the years ended December 31, 2010, 2009 and 2008:

In billions of dollars 2010 2009 2008

Cash flows received on retained interests

and other net cash flows $2.8 $2.7 $1.7

The effect of two negative changes in discount rates used to determine the

fair value of retained interests is disclosed below.

In millions of dollars

Asset-based

financing

Carrying value of retained interests $5,006

Value of underlying portfolio

Adverse change of 10% —

Adverse change of 20% (57)

Municipal Securities Tender Option Bond (TOB) Trusts

The Company sponsors TOB trusts that hold fixed- and floating-rate,

tax-exempt securities issued by state or local municipalities. The trusts are

typically single-issuer trusts whose assets are purchased from the Company

and from the market. The trusts are referred to as Tender Option Bond trusts

because the senior interest holders have the ability to tender their interests

periodically back to the issuing trust, as described further below.

The TOB trusts fund the purchase of their assets by issuing long-term

senior floating rate notes (floaters) and junior residual securities (residuals).

Floaters and residuals have a tenor equal to the maturity of the trust, which

is equal to or shorter than the tenor of the underlying municipal bond.

Residuals are frequently less than 1% of a trust’s total funding and entitle

their holder to residual cash flows from the issuing trust. Residuals are

generally rated based on the long-term rating of the underlying municipal

bond. Floaters bear interest rates that are typically reset weekly to a new

market rate (based on the SIFMA index: a seven-day high-grade market

index of tax-exempt, variable-rate municipal bonds). Floater holders have an

option to tender their floaters back to the trust periodically. Floaters have a

long-term rating based on the long-term rating of the underlying municipal

bond, including any credit enhancement provided by monoline insurance

companies, and a short-term rating based on that of the liquidity provider to

the trust.