Citibank 2010 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

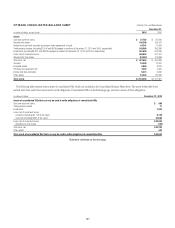

165

Consumer Mortgage Representations and Warranties

The majority of Citi’s exposure to representation and warranty claims relates

to its U.S. Consumer mortgage business.

When selling a loan, Citi (through its CitiMortgage business) makes

various representations and warranties relating to, among other things,

the following:

Citi’s ownership of the loan;•

the validity of the lien securing the loan;•

the absence of delinquent taxes or liens against the property securing •

the loan;

the effectiveness of title insurance on the property securing the loan;•

the process used in selecting the loans for inclusion in a transaction;•

the loan’s compliance with any applicable loan criteria established by the •

buyer; and

the loan’s compliance with applicable local, state and federal laws.•

The specific representations and warranties made by Citi depend

on the nature of the transaction and the requirements of the buyer.

Market conditions and credit rating agency requirements may also affect

representations and warranties and the other provisions to which Citi may

agree in loan sales.

Repurchases or “Make-Whole” Payments

In the event of a breach of these representations and warranties, Citi

may be required to either repurchase the mortgage loans (generally

at unpaid principal balance plus accrued interest) with the identified

defects or indemnify (“make-whole”) the investors for their losses. Citi’s

representations and warranties are generally not subject to stated limits in

amount or time of coverage. However, contractual liability arises only when

the representations and warranties are breached and generally only when a

loss results from the breach.

In the case of a repurchase, Citi will bear any subsequent credit loss on

the mortgage loan and the loan is typically considered a credit-impaired

loan and accounted for under SOP 03-3, “Accounting for Certain Loans and

Debt Securities Acquired in a Transfer” (now incorporated into ASC 310-30,

Receivables—Loans and Debt Securities Acquired with Deteriorated

Credit Quality) (SOP 03-3). These repurchases have not had a material

impact on Citi’s non-performing loan statistics because credit-impaired

purchased SOP 03-3 loans are not included in non-accrual loans, since they

generally continue to accrue interest until write-off.

Citi’s repurchases have primarily been from the U.S. government

sponsored entities (GSEs).

Citi has recorded a reserve for its exposure to losses from the obligation

to repurchase previously sold loans (referred to as the repurchase reserve)

that is included in Other liabilities in the Consolidated Balance Sheet. In

estimating the repurchase reserve, Citi considers reimbursements estimated

to be received from third-party correspondent lenders and indemnification

agreements relating to previous acquisitions of mortgage servicing rights. Citi

aggressively pursues collection from any correspondent lender that it believes

has the financial ability to pay. The estimated reimbursements are based on

Citi’s analysis of its most recent collection trends and the financial solvency

of the correspondents.

In the case of a repurchase of a credit-impaired SOP 03-3 loan, the

difference between the loan’s fair value and the repurchase amount is

recorded as a utilization of the repurchase reserve. Make-whole payments to

the investor are also treated as utilizations and charged directly against the

reserve. The repurchase reserve is estimated when Citi sells loans (recorded as

an adjustment to the gain on sale, which is included in Other revenue in the

Consolidated Statement of Income) and is updated quarterly. Any change in

estimate is recorded in Other revenue.

The repurchase reserve is calculated by individual sales vintage (i.e.,

the year the loans were sold) and is based on various assumptions. While

substantially all of Citi’s current loan sales are with GSEs, with which Citi

has considerable historical experience, these assumptions contain a level

of uncertainty and risk that, if different from actual results, could have a

material impact on the reserve amounts. The most significant assumptions

used to calculate the reserve levels are as follows:

Loan documentation requests;•

Repurchase claims as a percentage of loan documentation requests;•

Claims appeal success rate;•

Estimated loss given repurchase or make-whole.•

The repurchase reserve estimation process is subject to numerous

estimates and judgments. The assumptions used to calculate the repurchase

reserve contain a level of uncertainty and risk that, if different from actual

results, could have a material impact on the reserve amounts.

Securities and Banking

-Sponsored Private Label

Residential Mortgage Securitizations—Representations

and Warranties

Mortgage securitizations sponsored by Citi’s S&B business represent a much

smaller portion of Citi’s mortgage business.

The mortgages included in these securitizations were purchased from

parties outside of S&B. Representations and warranties (representations)

relating to the mortgage loans included in each trust issuing the securities

were made either by (1) Citi, or (2) in a relatively small number of cases,

third-party sellers (Selling Entities, which were also often the originators

of the loans). These representations were generally made or assigned to the

issuing trust.

The representations in these securitization transactions generally related

to, among other things, the following:

the absence of fraud on the part of the mortgage loan borrower, the seller •

or any appraiser, broker or other party involved in the origination of the

mortgage loan (which was sometimes wholly or partially limited to the

knowledge of the representation provider);

whether the mortgage property was occupied by the borrower as his or her •

principal residence;