Citibank 2010 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

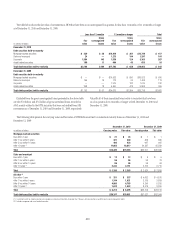

215

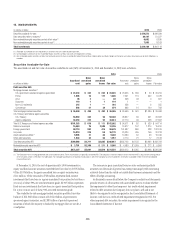

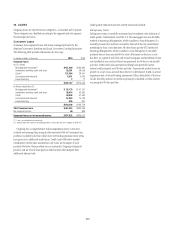

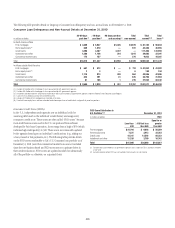

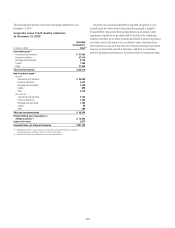

16. LOANS

Citigroup loans are reported in two categories—Consumer and Corporate.

These categories are classified according to the segment and sub-segment

that manages the loans.

Consumer Loans

Consumer loans represent loans and leases managed primarily by the

Regional Consumer Banking and Local Consumer Lending businesses.

The following table provides information by loan type:

In millions of dollars at year end 2010 2009

Consumer loans

In U.S. offices

Mortgage and real estate (1) $151,469 $183,842

Installment, revolving credit, and other 28,291 58,099

Cards (2) 122,384 28,951

Commercial and industrial 5,021 5,640

Lease financing 211

$307,167 $276,543

In offices outside the U.S.

Mortgage and real estate (1) $ 52,175 $ 47,297

Installment, revolving credit, and other 38,024 42,805

Cards 40,948 41,493

Commercial and industrial 18,584 14,780

Lease financing 665 331

$150,396 $146,706

Total Consumer loans $457,563 $423,249

Net unearned income 69 808

Consumer loans, net of unearned income $457,632 $424,057

(1) Loans secured primarily by real estate.

(2) 2010 includes the impact of consolidating entities in connection with Citi’s adoption of SFAS 167.

Citigroup has a comprehensive risk management process to monitor,

evaluate and manage the principal risks associated with its Consumer loan

portfolio. Included in the loan table above are lending products whose terms

may give rise to additional credit issues. Credit cards with below-market

introductory interest rates and interest-only loans are examples of such

products. However, these products are not material to Citigroup’s financial

position and are closely managed via credit controls that mitigate their

additional inherent risk.

Credit quality indicators that are actively monitored include:

Delinquency Status

Delinquency status is carefully monitored and considered a key indicator of

credit quality. Substantially all of the U.S. first mortgage loans use the MBA

method of reporting delinquencies, which considers a loan delinquent if a

monthly payment has not been received by the end of the day immediately

preceding the loan’s next due date. All other loans use the OTS method of

reporting delinquencies, which considers a loan delinquent if a monthly

payment has not been received by the close of business on the loan’s next

due date. As a general rule, first and second mortgages and installment loans

are classified as non-accrual when loan payments are 90 days contractually

past due. Credit cards and unsecured revolving loans generally accrue

interest until payments are 180 days past due. Commercial market loans are

placed on a cash (non-accrual) basis when it is determined, based on actual

experience and a forward-looking assessment of the collectability of the loan

in full, that the payment of interest or principal is doubtful or when interest

or principal is 90 days past due.