Citibank 2010 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

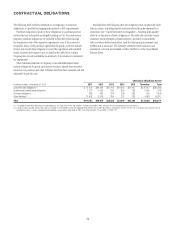

71

RISK FACTORS

The ongoing implementation of the Dodd-Frank Wall Street

Reform and Consumer Protection Act of 2010 will require

Citigroup to restructure or change certain of its business

practices and potentially reduce revenues or otherwise

limit its profitability, including by imposing additional

costs on Citigroup, some of which may be significant.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010

(Financial Reform Act), signed into law on July 21, 2010, calls for significant

structural reforms and new substantive regulation across the financial

industry. Because most of the provisions of the Financial Reform Act that

could particularly impact Citi are currently or will be subject to extensive

rulemaking and interpretation, a significant amount of uncertainty remains

as to the ultimate impact of the Financial Reform Act on Citigroup, especially

when combined with other ongoing U.S. and global regulatory developments.

This uncertainty impedes future planning with respect to certain of Citi’s

businesses and, combined with the extensive and comprehensive regulatory

requirements adopted and implemented in compressed time frames,

presents operational and compliance costs and risks. What is certain is that

the Financial Reform Act will require Citigroup to restructure, transform

or change certain of its business activities and practices, potentially limit

or eliminate Citi’s ability to pursue business opportunities, and impose

additional costs, some significant, on Citigroup, each of which could

negatively impact, possibly significantly, Citigroup’s earnings.

Increases in FDIC insurance premiums will significantly

increase Citi’s required premiums, which will negatively

impact Citigroup’s earnings.

The FDIC maintains a fund out of which it covers losses on insured deposits.

The fund is composed of assessments on financial institutions that hold

FDIC-insured deposits, including Citibank, N.A. and Citigroup’s other

FDIC-insured depository institutions. As a result of the recent financial

crisis, the Financial Reform Act seeks to put the FDIC fund on a sounder

financial footing by requiring that the fund have assets equal to at least

1.35% of insurable deposits. The FDIC has adopted a higher target of 2.0% of

insurable deposits.

The cost of FDIC assessments to FDIC-insured depository institutions,

including Citibank, N.A. and Citigroup’s other FDIC-insured depository

institutions, depends on the assessment rate and the assessment base of each

institution. The Financial Reform Act changed the assessment base from

the amount of U.S. domestic deposits to the amount of worldwide average

consolidated total assets less average tangible equity. The FDIC has adopted

a complex set of calculation rules for its assessment rate, to be effective

in the second quarter of 2011. As a result of these changes, Citigroup’s

FDIC assessments could increase significantly (prior to any potential

mitigating actions), which will negatively impact its earnings. Given

Citi’s substantial global footprint, the change from an assessment based

on Citigroup’s relatively smaller U.S. deposit base, as compared to its U.S.

competitors, to one related to global assets (including Citigroup’s relatively

larger global deposit base as compared to its U.S. competitors) will cause a

disproportionate increase in Citigroup’s assessment base relative to many of

its U.S. competitors that are subject to the FDIC assessment. The assessment

could also disadvantage Citi’s competitive position in relation to foreign local

banks which are not subject to the assessment.

Although Citigroup currently believes it is “well

capitalized,” prospective regulatory capital requirements

for financial institutions are uncertain and Citi’s

capitalization may not prove to be sufficient relative to

future requirements.

The prospective regulatory capital standards for financial institutions are

currently subject to significant debate and rulemaking activity, both in the

U.S. and internationally, resulting in a degree of uncertainty as to their

ultimate scope and effect.

As an outgrowth of the financial crisis, the Basel Committee on Banking

Supervision (Basel Committee) has established global financial reforms

designed, in part, to strengthen existing capital requirements (Basel III).

Under Basel III, when fully phased in, Citigroup would be subject to stated

minimum capital ratio requirements for Tier 1 Common of 4.5%, for Tier 1

Capital of 6.0%, and for Total Capital of 8.0%. Further, the new standards

also require a capital conservation buffer of 2.5%, and potentially also a

countercyclical capital buffer, above these stated minimum requirements

for each of these three capital tiers. Apart from risk-based capital, Basel III

also introduced a more constrained Leverage ratio requirement than that

currently imposed on U.S. banking organizations. For more information on

Basel III and other requirements and proposals relating to capital adequacy,

see “Capital Resources—Regulatory Capital Standards Developments” above.

Even though Citigroup continues to be “well capitalized” in accordance

with current federal bank regulatory agency definitions, with a Tier 1 Capital

ratio of 12.9%, a Total Capital ratio of 16.6%, and a Leverage ratio of 6.6%,

as well as a Tier 1 Common ratio of 10.8%, each as of December 31, 2010,

Citigroup may not be able to maintain sufficient capital consistent with

Basel III and other future regulatory capital requirements. Because the rules

relating to the U.S. implementation of Basel III and other future regulatory

capital requirements are not entirely certain, Citigroup’s ability to comply

with these requirements on a timely basis depends upon certain assumptions,

including, for instance, those with respect to Citigroup’s significant

investments in unconsolidated financial entities (such as the Morgan Stanley

Smith Barney joint venture), the size of Citigroup’s deferred tax assets and

MSRs, and its internal risk calibration models. If any of these assumptions

proves to be incorrect, it could negatively affect Citigroup’s ability to comply

in a timely manner with these future regulatory capital requirements.

In addition, the Financial Reform Act grants new regulatory authority to

various U.S. federal regulators, including the Federal Reserve Board and a

newly created Financial Stability Oversight Council, to impose heightened

prudential standards on financial institutions that pose a systemic risk

to market-wide financial stability (Citigroup will be defined as such an

institution under the Financial Reform Act). These standards include

heightened capital, leverage and liquidity standards, as well as requirements