Citibank 2010 Annual Report Download - page 252

Download and view the complete annual report

Please find page 252 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

250

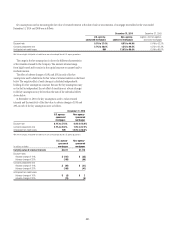

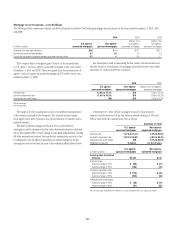

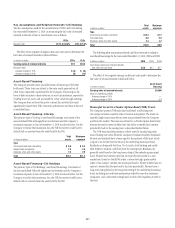

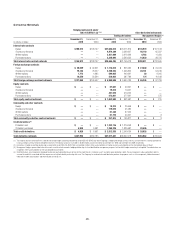

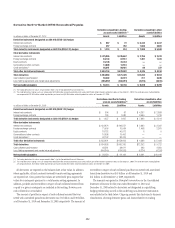

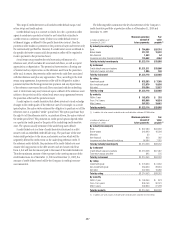

23. DERIVATIVES ACTIVITIES

In the ordinary course of business, Citigroup enters into various types of

derivative transactions. These derivative transactions include:

Futures and forward contracts,• which are commitments to buy or

sell at a future date a financial instrument, commodity or currency at a

contracted price and may be settled in cash or through delivery.

Swap contracts, • which are commitments to settle in cash at a future date

or dates that may range from a few days to a number of years, based on

differentials between specified financial indices, as applied to a notional

principal amount.

Option contracts,• which give the purchaser, for a fee, the right, but

not the obligation, to buy or sell within a specified time a financial

instrument, commodity or currency at a contracted price that may also be

settled in cash, based on differentials between specified indices or prices.

Citigroup enters into these derivative contracts relating to interest rate, foreign

currency, commodity, and other market/credit risks for the following reasons:

Trading Purposes—Customer Needs: • Citigroup offers its customers

derivatives in connection with their risk-management actions to

transfer, modify or reduce their interest rate, foreign exchange and

other market/credit risks or for their own trading purposes. As part of

this process, Citigroup considers the customers’ suitability for the risk

involved and the business purpose for the transaction. Citigroup also

manages its derivative-risk positions through offsetting trade activities,

controls focused on price verification, and daily reporting of positions to

senior managers.

Trading Purposes—Own Account: • Citigroup trades derivatives for its

own account and as an active market maker. Trading limits and price

verification controls are key aspects of this activity.

Hedging:• Citigroup uses derivatives in connection with its risk-

management activities to hedge certain risks or reposition the risk profile

of the Company. For example, Citigroup may issue fixed-rate long-term

debt and then enter into a receive-fixed, pay-variable-rate interest rate

swap with the same tenor and notional amount to convert the interest

payments to a net variable-rate basis. This strategy is the most common

form of an interest rate hedge, as it minimizes interest cost in certain yield

curve environments. Derivatives are also used to manage risks inherent

in specific groups of on-balance-sheet assets and liabilities, including

investments, loans and deposit liabilities, as well as other interest-sensitive

assets and liabilities. In addition, foreign-exchange contracts are used to

hedge non-U.S.-dollar-denominated debt, foreign-currency-denominated

available-for-sale securities, net investment exposures and foreign-

exchange transactions.

Derivatives may expose Citigroup to market, credit or liquidity risks in

excess of the amounts recorded on the Consolidated Balance Sheet. Market

risk on a derivative product is the exposure created by potential fluctuations

in interest rates, foreign-exchange rates and other factors and is a function

of the type of product, the volume of transactions, the tenor and terms of the

agreement, and the underlying volatility. Credit risk is the exposure to loss

in the event of nonperformance by the other party to the transaction where

the value of any collateral held is not adequate to cover such losses. The

recognition in earnings of unrealized gains on these transactions is subject

to management’s assessment as to collectability. Liquidity risk is the potential

exposure that arises when the size of the derivative position may not be able

to be rapidly adjusted in periods of high volatility and financial stress at a

reasonable cost.

Information pertaining to the volume of derivative activity is provided in

the tables below. The notional amounts, for both long and short derivative

positions, of Citigroup’s derivative instruments as of December 31, 2010 and

December 31, 2009 are presented in the table below.