Citibank 2010 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

63

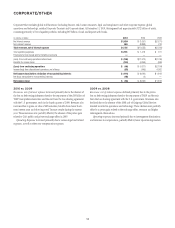

Regulatory Capital Standards Developments

The prospective regulatory capital standards for financial institutions are

currently subject to significant debate, rulemaking activity and uncertainty,

both in the U.S. and internationally. See “Risk Factors” below.

Basel II and III. In late 2005, the Basel Committee on Banking

Supervision (Basel Committee) published a new set of risk-based

capital standards (Basel II) that would permit banking organizations,

including Citigroup, to leverage internal risk models used to measure

credit, operational, and market risk exposures to drive regulatory capital

calculations. In late 2007, the U.S. banking agencies adopted these standards

for large banking organizations, including Citigroup. As adopted, the

standards require Citigroup, as a large and internationally active banking

organization, to comply with the most advanced Basel II approaches for

calculating credit and operational risk capital requirements. The U.S.

implementation timetable consists of a parallel calculation period under the

current regulatory capital regime (Basel I) and Basel II, followed by a three-

year transitional period.

Citi began parallel reporting on April 1, 2010. There will be at least four

quarters of parallel reporting before Citi enters the three-year transitional

period. The U.S. banking agencies have reserved the right to change how

Basel II is applied in the U.S. following a review at the end of the second year

of the transitional period, and to retain the existing prompt corrective action

and leverage capital requirements applicable to banking organizations in

the U.S.

Apart from the Basel II rules regarding credit and operational risks, in

June 2010, the Basel Committee agreed on certain revisions to the market risk

capital framework that would also result in additional capital requirements.

In December 2010, the U.S. banking agencies issued a proposal that would

amend their market risk capital rules to implement certain revisions

approved by the Basel Committee to the market risk capital framework.

Further, as an outgrowth of the financial crisis, in December 2010,

the Basel Committee issued final rules to strengthen existing capital

requirements (Basel III). The U.S. banking agencies will be required

to finalize, within two years, the rules to be applied by U.S. banking

organizations commencing on January 1, 2013.

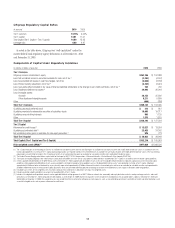

Under Basel III, when fully phased in on January 1, 2019, Citigroup would

be required to maintain risk-based capital ratios as follows:

Tier 1 Common Tier 1 Capital Total Capital

Stated minimum ratio 4.5% 6.0% 8.0%

Plus: Capital conservation

buffer requirement 2.5 2.5 2.5

Effective minimum ratio 7.0% 8.5% 10.5%

While banking organizations may draw on the 2.5% capital conservation

buffer to absorb losses during periods of financial or economic stress,

restrictions on earnings distributions (e.g., dividends, equity repurchases, and

discretionary compensation) would result, with the degree of such restrictions

greater based upon the extent to which the buffer is utilized. Moreover,

subject to national discretion by the respective bank supervisory or regulatory

authorities, a countercyclical capital buffer ranging from 0% to 2.5%,

consisting of common equity or other fully loss absorbing capital, would

also be imposed on banking organizations when it is deemed that excess

aggregate credit growth is resulting in a build-up of systemic risk in a given

country. This countercyclical capital buffer, when in effect, would serve as an

additional buffer supplementing the capital conservation buffer.

As a systemically important financial institution, Citigroup may also

be subject to additional capital requirements. The Basel Committee and

the Financial Stability Board are currently developing an integrated

approach to systemically important financial institutions that could include

combinations of capital surcharges, contingent capital and bail-in debt.

Under Basel III, Tier 1 Common capital will be required to be measured

after applying generally all regulatory adjustments (including applicable

deductions). The impact of these regulatory adjustments on Tier 1 Common

capital would be phased in incrementally at 20% annually beginning on

January 1, 2014, with full implementation by January 1, 2018. During the

transition period, the portion of the regulatory adjustments (including

applicable deductions) not applied against Tier 1 Common capital would

continue to be subject to existing national treatments.

Moreover, under Basel III certain capital instruments will no longer qualify

as non-common components of Tier 1 Capital (e.g., trust preferred securities

and cumulative perpetual preferred stock) or Tier 2 Capital. These instruments

will be subject to a 10% per-year phase-out over 10 years beginning on January

1, 2013, except for certain limited grandfathering. This phase-out period

will be substantially shorter in the U.S. as a result of the so-called “Collins

Amendment” to the Dodd-Frank Wall Street Reform and Consumer Protection

Act of 2010, which will generally require a phase out of these securities over

a three-year period also beginning on January 1, 2013. In addition, the Basel

Committee has subsequently issued supplementary minimum requirements to

those contained in Basel III, which must be met or exceeded in order to ensure

that qualifying non-common Tier 1 or Tier 2 Capital instruments fully absorb

losses at the point of a banking organization’s non-viability before taxpayers are

exposed to loss. These requirements must be reflected within the terms of the

capital instruments unless, subject to certain conditions, they are implemented

through the governing jurisdiction’s legal framework.

Although U.S. banking organizations, such as Citigroup, are currently

subject to a supplementary, non-risk-based measure of leverage for capital

adequacy purposes (see “Capital Ratios” above), Basel III establishes a more

constrained Leverage ratio requirement. Initially, during a four-year parallel

run beginning on January 1, 2013, banking organizations will be required

to maintain a minimum 3% Tier 1 Capital Leverage ratio. Disclosure of such

ratio, and its components, will start on January 1, 2015. Depending upon the

results of the parallel run test period, there could be subsequent adjustments

to the definition and calibration of the Leverage ratio, which is to be finalized

in 2017 and become a formal requirement by January 1, 2018.