Citibank 2010 Annual Report Download - page 220

Download and view the complete annual report

Please find page 220 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

218

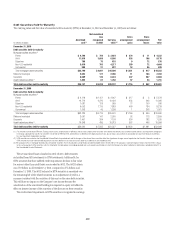

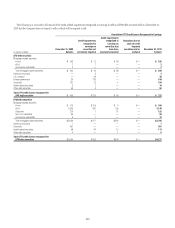

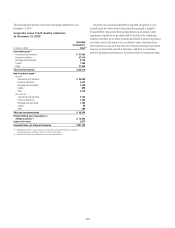

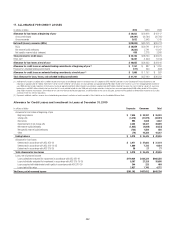

Corporate Loans

Corporate loans represent loans and leases managed by ICG or the Special

Asset Pool. The following table presents information by corporate loan type:

In millions of dollars at year end 2010 2009

Corporate

In U.S. offices

Commercial and industrial $ 14,334 $ 15,614

Loans to financial institutions (1) 29,813 6,947

Mortgage and real estate (2) 19,693 22,560

Installment, revolving credit and other (3) 12,640 17,737

Lease financing 1,413 1,297

$ 77,893 $ 64,155

In offices outside the U.S.

Commercial and industrial $ 69,718 $ 66,747

Installment, revolving credit and other (3) 11,829 9,683

Mortgage and real estate (2) 5,899 9,779

Loans to financial institutions 22,620 15,113

Lease financing 531 1,295

Governments and official institutions 3,644 2,949

$114,241 $105,566

Total Corporate loans $192,134 $169,721

Net unearned income (972) (2,274)

Corporate loans, net of unearned income $191,162 $167,447

(1) 2010 includes the impact of consolidating entities in connection with Citi’s adoption of SFAS 167.

(2) Loans secured primarily by real estate.

(3) Includes loans not otherwise separately categorized.

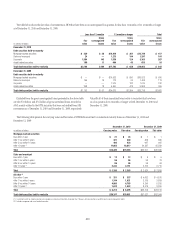

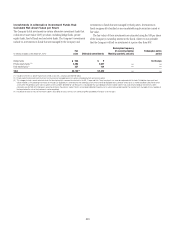

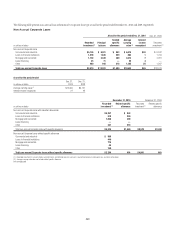

Corporate loans are identified as impaired and placed on a cash

(non-accrual) basis when it is determined, based on actual experience and

a forward-looking assessment of the collectability of the loan in full, that the

payment of interest or principal is doubtful or when interest or principal is

90 days past due, except when the loan is well collateralized and in the process

of collection. Any interest accrued on impaired corporate loans and leases

is reversed at 90 days and charged against current earnings, and interest is

thereafter included in earnings only to the extent actually received in cash.

When there is doubt regarding the ultimate collectability of principal, all

cash receipts are thereafter applied to reduce the recorded investment in the

loan. While Corporate loans are generally managed based on their internally

assigned risk rating (see further discussion below), the following table presents

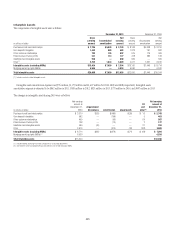

delinquency information by Corporate loan type as of December 31, 2010:

Corporate Loan Delinquency and Non-Accrual Details at December 31, 2010

In millions of dollars

30–89 days

past due

and accruing (1)

≥ 90 days

past due and

accruing (1)

Total past due

and accruing

Total

non-accrual (2)

Total

current (3)

Total

loans

Commercial and industrial $ 94 $ 39 $133 $5,125 $ 76,862 $ 82,120

Financial institutions 2 — 2 1,258 50,648 51,908

Mortgage and real estate 376 20 396 1,782 22,892 25,070

Leases 9 — 9 45 1,890 1,944

Other 100 52 152 400 26,941 27,493

Loans at fair value 2,627

Total $ 581 $111 $692 $8,610 $179,233 $191,162

(1) Corporate loans that are greater than 90 days past due are generally classified as non-accrual.

(2) Citi generally does not manage Corporate loans on a delinquency basis. Non-accrual loans generally include those loans that are ≥ 90 days past due or those loans for which Citi believes, based on actual experience

and a forward-looking assessment of the collectability of the loan in full that the payment or interest or principal is doubtful.

(3) Loans less than 30 days past due are considered current.

Citigroup has a comprehensive risk management process to monitor,

evaluate and manage the principal risks associated with its Corporate loan

portfolio. As part of its risk management process, Citi assigns risk ratings

to its Corporate loans, which are reviewed at least annually. The ratings

scale generally corresponds to the ratings as defined by S&P and Moody’s,

with investment grade facilities generally exhibiting no evident weakness

in creditworthiness and non-investment grade facilities exhibiting a range

of deterioration in the obligor’s creditworthiness or vulnerability to adverse

changes in business, financial or other economic conditions.