Citibank 2010 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

118

Mitigation and Hedging of Risk

Financial institutions’ financial performance is subject to some degree of risk due

to changes in interest rates. In order to manage these risks effectively, Citigroup

may modify pricing on new customer loans and deposits, enter into transactions

with other institutions or enter into off-balance-sheet derivative transactions that

have the opposite risk exposures. Thus, Citigroup regularly assesses the viability of

strategies to reduce unacceptable risks to earnings and implements such strategies

when it believes those actions are prudent. As information becomes available,

Citigroup formulates strategies aimed at protecting earnings from the potential

negative effects of changes in interest rates.

Citigroup employs additional measurements, including stress testing the

impact of non-linear interest rate movements on the value of the balance

sheet; the analysis of portfolio duration and volatility, particularly as they

relate to mortgage loans and mortgage-backed securities; and the potential

impact of the change in the spread between different market indices.

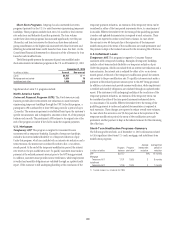

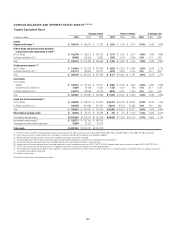

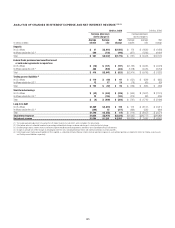

Non-Trading Portfolios

The exposures in the following table represent the approximate annualized

risk to NIR assuming an unanticipated parallel instantaneous 100 bps

change, as well as a more gradual 100 bps (25 bps per quarter) parallel

change in rates compared with the market forward interest rates in selected

currencies.

December 31, 2010 December 31, 2009

In millions of dollars Increase Decrease Increase Decrease

U.S. dollar

Instantaneous change $(105) NM $ (859) NM

Gradual change 25 NM (460) NM

Mexican peso

Instantaneous change $ 181 $(181) $ 50 $ (50)

Gradual change 107 (107) 26 (26)

Euro

Instantaneous change $ (10) $ (38) $ 85 NM

Gradual change (8) 8 47 NM

Japanese yen

Instantaneous change $ 93 NM $ 200 NM

Gradual change 52 NM 116 NM

Pound sterling

Instantaneous change $ 33 $ (20) $ (11) NM

Gradual change 21 (21) (6) NM

NM Not meaningful

A 100 bps decrease in interest rates would imply negative rates for the yield curve.

The changes in the U.S. dollar IRE from the prior year reflect revised

modeling of mortgages and deposits based on lower rates, pricing changes

due to the CARD Act, asset sales, debt issuance and swapping activities, as well

as repositioning of the liquidity portfolio.

Certain trading-oriented businesses within Citi have accrual-accounted

positions that are excluded from the table above. The U.S. dollar IRE

associated with these businesses is $(79) million for a 100 basis point

instantaneous increase in interest rates.

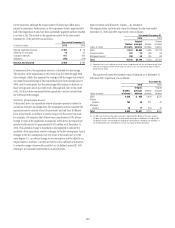

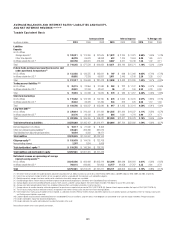

The following table shows the risk to NIR from six different changes in the implied-forward rates. Each scenario assumes that the rate change will occur on a

gradual basis every three months over the course of one year.

Scenario 1 Scenario 2 Scenario 3 Scenario 4 Scenario 5 Scenario 6

Overnight rate change (bps) — 100 200 (200) (100) —

10-year rate change (bps) (100) — 100 (100) — 100

Impact to net interest revenue (in millions of dollars) $(135) $ 61 $ (39) NM NM $ (21)