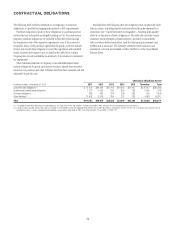

Citibank 2010 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

72

for periodic stress tests (the first round of which is in the process of being

implemented). The Federal Reserve Board may also impose other prudential

standards, including contingent capital requirements, based upon its

authority to distinguish among bank holding companies such as Citigroup

in relation to their perceived riskiness, complexity, activities, size and other

factors. The exact nature of these future requirements remains uncertain.

Further, the so-called “Collins Amendment” reflected in the Financial

Reform Act will result in new minimum capital requirements for bank

holding companies such as Citigroup, and provides for the phase-out of trust

preferred securities and other hybrid capital securities from Tier 1 Capital for

regulatory capital purposes, beginning January 1, 2013. As of December 31,

2010, Citigroup had approximately $15.4 billion in outstanding trust

preferred securities that will be subject to the provisions of the Collins

Amendment. As a result, Citigroup may need to replace certain of its existing

Tier 1 Capital with new capital.

Accordingly, Citigroup may not be able to maintain sufficient capital

in light of the changing and uncertain regulatory capital requirements

resulting from the Financial Reform Act, the Basel Committee, and U.S. or

international regulators, or Citigroup’s costs to maintain such capital levels

may increase.

Changes in regulation of derivatives under the Financial

Reform Act, including certain central clearing and

exchange trading activities, will require Citigroup to

restructure certain areas of its derivatives business which

will be disruptive and may adversely affect the results of

operations from certain of its over-the-counter and other

derivatives activities.

The Financial Reform Act and the regulations to be promulgated thereunder

will require certain over-the-counter derivatives to be standardized, subject

to requirements for transaction reporting, clearing through regulatorily

recognized clearing facilities and trading on exchanges or exchange-

like facilities. The regulations implementing this aspect of the Financial

Reform Act, including for example the definition of, and requirements

for, “swap execution facilities” through which transactions and reporting

in standardized products may be required to be carried out, and the

determination of margin requirements, are still in the process of being

formulated, and thus, the final scope of the requirements is not known. These

requirements will, however, necessitate changes to certain areas of Citi’s

derivatives business structures and practices, including without limitation

the successful and timely installation of the appropriate technological and

operational systems to report and trade the applicable derivatives accurately,

which will be disruptive, divert management attention and require additional

investment into such businesses.

The above changes could also increase Citigroup’s exposure to the

regulatorily recognized clearing facilities and exchanges, which could build

up into material concentrations of exposure. This could result in Citigroup

having a significant dependence on the continuing efficient and effective

functioning of these clearing and trading facilities, and on their continuing

financial stability.

In addition, under the so-called “push-out” provisions of the Financial

Reform Act and the regulations to be promulgated thereunder, derivatives

activities, with the exception of bona fide hedging activities and derivatives

related to traditional bank-permissible reference assets, will be curtailed

on FDIC-insured depository institutions. Citigroup, like many of its U.S.

bank competitors, conducts a substantial portion of its derivatives activities

through an insured depository institution. Moreover, to the extent that

certain of Citi’s competitors conduct such activities outside of FDIC-insured

depository institutions, Citi would be disproportionately impacted by any

restructuring of its business for push-out purposes. While the exact nature

of the changes required under the Financial Reform Act is uncertain, the

changes that are ultimately implemented will require restructuring these

activities which could negatively impact Citi’s results of operations from

these activities.

Regulatory requirements aimed at facilitating the

future orderly resolution of large financial institutions

could result in Citigroup having to change its business

structures, activities and practices in ways that negatively

impact its operations.

The Financial Reform Act requires Citi to plan for a rapid and orderly

resolution in the event of future material financial distress or failure,

and to provide its regulators information regarding the manner in which

Citibank, N.A. and its other insured depository institutions are adequately

protected from the risk of non-bank affiliates. Regulatory requirements

aimed at facilitating future resolutions in the U.S. and globally could

result in Citigroup having to restructure or reorganize businesses, legal

entities, or intercompany systems or transactions in ways that negatively

impact Citigroup’s operations. For example, Citi could be required to create

new subsidiaries instead of branches in foreign jurisdictions, or create

separate subsidiaries to house particular businesses or operations (so-called

“subsidiarization”), which would, among other things, increase Citi’s legal,

regulatory and managerial costs, negatively impact Citi’s global capital and

liquidity management and potentially impede its global strategy.

While Citigroup believes one of its competitive advantages

is its extensive global network, Citi’s extensive operations

outside of the U.S. subject it to emerging market and

sovereign volatility and numerous inconsistent or

conflicting regulations, which increase Citi’s compliance,

regulatory and other costs.

Citigroup believes its extensive global network—which includes a physical

presence in approximately 100 countries and services offered in over

160 countries and jurisdictions—provides it a competitive advantage in

servicing the broad financial services needs of large multinational clients and

its customers around the world, including in many of the world’s emerging

markets. This global footprint, however, subjects Citi to emerging market and

sovereign volatility and extensive, often inconsistent or conflicting, regulation,

all of which increase Citi’s compliance, regulatory and other costs.