Citibank 2010 Annual Report Download - page 250

Download and view the complete annual report

Please find page 250 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

248

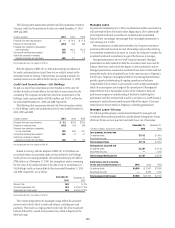

The Company sponsors two kinds of TOB trusts: customer TOB trusts

and proprietary TOB trusts. Customer TOB trusts are trusts through which

customers finance investments in municipal securities. Residuals are held

by customers, and floaters by third-party investors. Proprietary TOB trusts

are trusts through which the Company finances its own investments in

municipal securities. The Company holds residuals in proprietary TOB trusts.

The Company serves as remarketing agent to the trusts, facilitating

the sale of floaters to third parties at inception and facilitating the reset of

the floater coupon and tenders of floaters. If floaters are tendered and the

Company (in its role as remarketing agent) is unable to find a new investor

within a specified period of time, it can declare a failed remarketing (in

which case the trust is unwound) or it may choose to buy floaters into its own

inventory and may continue to try to sell them to a third-party investor. While

the level of the Company’s inventory of floaters fluctuates, the Company

held none of the floater inventory related to the customer or proprietary TOB

programs as of December 31, 2010.

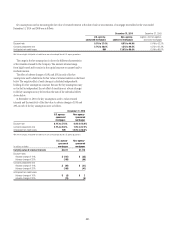

Approximately $0.6 billion of the municipal bonds owned by TOB trusts

have a credit guarantee provided by the Company. In all other cases, the

assets are either unenhanced or are insured with a monoline insurance

company. While the trusts have not encountered any adverse credit events

as defined in the underlying trust agreements, certain monoline insurance

companies have experienced downgrades. In these cases, the Company has

proactively managed the TOB programs by applying additional insurance on

the assets or proceeding with orderly unwinds of the trusts.

If a trust is unwound early due to an event other than a credit event on

the underlying municipal bond, the underlying municipal bond is sold

in the market. If there is an accompanying shortfall in the trust’s cash

flows to fund the redemption of floaters after the sale of the underlying

municipal bond, the trust draws on a liquidity agreement in an amount

equal to the shortfall. Liquidity agreements are generally provided to

the trust directly by the Company. For customer TOBs where the residual

is less than 25% of the trust’s capital structure, the Company has a

reimbursement agreement with the residual holder under which the residual

holder reimburses the Company for any payment made under the liquidity

arrangement. Through this reimbursement agreement, the residual holder

remains economically exposed to fluctuations in the value of the municipal

bond. These reimbursement agreements are actively margined based on

changes in the value of the underlying municipal bond to mitigate the

Company’s counterparty credit risk. In cases where a third party provides

liquidity to a proprietary TOB trust, a similar reimbursement arrangement is

made whereby the Company (or a consolidated subsidiary of the Company)

as residual holder absorbs any losses incurred by the liquidity provider. As of

December 31, 2010, liquidity agreements provided with respect to customer

TOB trusts, and other non-consolidated, customer-sponsored municipal

investment funds, totaled $10.1 billion, offset by reimbursement agreements

in place with a notional amount of $8.6 billion. The remaining exposure

relates to TOB transactions where the residual owned by the customer is

at least 25% of the bond value at the inception of the transaction and no

reimbursement agreement is executed. In addition, the Company has

provided liquidity arrangements with a notional amount of $0.1 billion for

other unconsolidated proprietary TOB trusts described below.

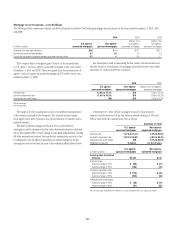

The Company considers the customer and proprietary TOB trusts to be

VIEs. Customer TOB trusts were not consolidated by the Company in prior

periods and remain unconsolidated upon the Company’s adoption of SFAS

167. Because third-party investors hold residual and floater interests in the

customer TOB trusts, the Company’s involvement includes only its role as

remarketing agent and liquidity provider. The Company has concluded

that the power over customer TOB trusts is primarily held by the customer

residual holder, who may unilaterally cause the sale of the trust’s bonds.

Because the Company does not hold the residual interest and thus does not

have the power to direct the activities that most significantly impact the

trust’s economic performance, it does not consolidate the customer TOB

trusts under SFAS 167.

Proprietary TOB trusts generally were consolidated in prior periods.

They remain consolidated upon the Company’s adoption of SFAS 167. The

Company’s involvement with the Proprietary TOB trusts includes holding the

residual interests as well as the remarketing and liquidity agreements with

the trusts. Similar to customer TOB trusts, the Company has concluded that

the power over the proprietary TOB trusts is primarily held by the residual

holder, who may unilaterally cause the sale of the trust’s bonds. Because

the Company holds residual interest and thus has the power to direct the

activities that most significantly impact the trust’s economic performance, it

continues to consolidate the proprietary TOB trusts under SFAS 167.

Prior to 2010, certain TOB trusts met the definition of a QSPE and were

not consolidated in prior periods. Upon the Company’s adoption of SFAS

167, former QSPE trusts have been consolidated by the Company as residual

interest holders and are presented as proprietary TOB trusts.

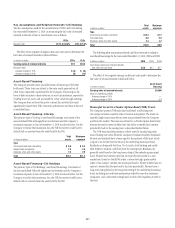

Total assets in proprietary TOB trusts also include $0.5 billion of

assets where residuals are held by hedge funds that are consolidated and

managed by the Company. The assets and the associated liabilities of these

TOB trusts are not consolidated by the hedge funds (and, thus, are not

consolidated by the Company) under the application of ASC 946, Financial

Services—Investment Companies, which precludes consolidation of

owned investments. The Company consolidates the hedge funds, because

the Company holds controlling financial interests in the hedge funds.

Certain of the Company’s equity investments in the hedge funds are hedged

with derivatives transactions executed by the Company with third parties

referencing the returns of the hedge fund. The Company’s accounting for

these hedge funds and their interests in the TOB trusts is unchanged by the

Company’s adoption of SFAS 167.