Citibank 2010 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

137

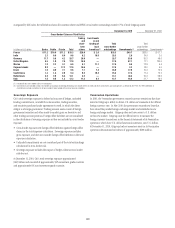

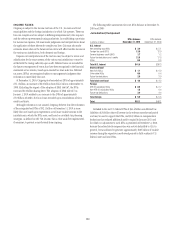

The following table reflects the incremental impact of adopting SFAS

166/167 on Citigroup’s GAAP assets, liabilities, and stockholders’ equity.

In billions of dollars January 1, 2010

Assets

Trading account assets $ (9.9)

Investments (0.6)

Loans 159.4

Allowance for loan losses (13.4)

Other assets 1.8

Total assets $137.3

Liabilities

Short-term borrowings $ 58.3

Long-term debt 86.1

Other liabilities 1.3

Total liabilities $145.7

Stockholders’ equity

Retained earnings $ (8.4)

Total stockholders’ equity (8.4)

Total liabilities and stockholders’ equity $137.3

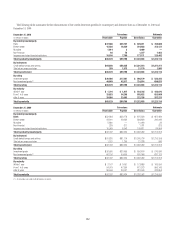

The preceding tables reflect: (i) the portion of the assets of former

QSPEs to which Citigroup, acting as principal, had transferred assets and

received sales treatment prior to January 1, 2010 (totaling approximately

$712.0 billion), and (ii) the assets of significant VIEs as of January 1, 2010

with which Citigroup is involved (totaling approximately $219.2 billion) that

were previously unconsolidated and are required to be consolidated under

the new accounting standards. Due to the variety of transaction structures

and the level of Citigroup involvement in individual former QSPEs and VIEs,

only a portion of the former QSPEs and VIEs with which Citi is involved were

required to be consolidated.

In addition, the cumulative effect of adopting these new accounting

standards as of January 1, 2010 resulted in an aggregate after-tax charge

to Retained earnings of $8.4 billion, reflecting the net effect of an

overall pretax charge to Retained earnings (primarily relating to the

establishment of loan loss reserves and the reversal of residual interests held)

of $13.4 billion and the recognition of related deferred tax assets amounting

to $5.0 billion.

The impact on certain of Citigroup’s regulatory capital ratios of adopting

these new accounting standards, reflecting immediate implementation of

the recently issued final risk-based capital rules regarding SFAS 166/167, was

as follows:

As of January 1, 2010

Impact

Tier 1 Capital (141) bps

Total Capital (142) bps

Non-Consolidation of Certain Investment Funds

The FASB issued Accounting Standards Update No. 2010-10, Consolidation

(Topic 810), Amendments for Certain Investment Funds (ASU 2010-10)

in the first quarter of 2010. ASU 2010-10 provides a deferral to the

requirements of SFAS 167 where the following criteria are met:

the entity being evaluated for consolidation is an investment company, as •

defined, or an entity for which it is acceptable based on industry practice

to apply measurement principles that are consistent with an investment

company;

the reporting enterprise does not have an explicit or implicit obligation •

to fund losses of the entity that could potentially be significant to the

entity; and

the entity being evaluated for consolidation is not:•

– a securitization entity;

– an asset-backed financing entity; or

– an entity that was formerly considered a qualifying special-purpose entity.

Citigroup has determined that a majority of the investment vehicles managed

by it are provided a deferral from the requirements of SFAS 167 as they meet

these criteria. These vehicles continue to be evaluated under the requirements

of FIN 46(R) (ASC 810-10), prior to the implementation of SFAS 167.

Where Citi has determined that certain investment vehicles are subject to

the consolidation requirements of SFAS 167, the consolidation conclusions

reached upon initial application of SFAS 167 are consistent with the

consolidation conclusions reached under the requirements of ASC 810-10,

prior to the implementation of SFAS 167.