Citibank 2010 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

83

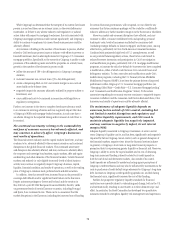

CREDIT RISK

Credit risk is the potential for financial loss resulting from the failure of a

borrower or counterparty to honor its financial or contractual obligations.

Credit risk arises in many of Citigroup’s business activities, including:

lending; •

sales and trading; •

derivatives; •

securities transactions; •

settlement; and •

when Citigroup acts as an intermediary.•

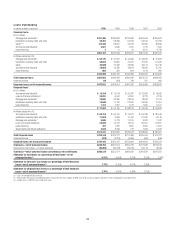

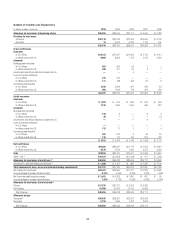

Loan and Credit Overview

During 2010, Citigroup’s aggregate loan portfolio increased by $57.3 billion

to $648.8 billion primarily due to the adoption of SFAS 166/167 on

January 1, 2010. Excluding the impact of SFAS 166/167, the aggregate loan

portfolio decreased by $102.1 billon. Citi’s total allowance for loan losses

totaled $40.7 billion at December 31, 2010, a coverage ratio of 6.31% of total

loans, up from 6.09% at December 31, 2009.

During 2010, Citi had a net release of $5.8 billion from its credit reserves

and allowance for unfunded lending commitments, compared to a net build

of $8.3 billion in 2009. The release consisted of a net release of $2.5 billion

for Corporate loans (primarily in SAP) and a net release of $3.3 billion for

Consumer loans (mainly a $1.5 billion release in RCB and a $1.8 billion

release in LCL). Despite the reserve release for Consumer loans, the

coincident months of net credit loss coverage for the Consumer portfolio

increased from 13.7 months in 2009 to 15.0 months in 2010.

Net credit losses of $30.9 billion during 2010 decreased $11.4 billion

from year-ago levels (on a managed basis). The decrease consisted of a net

decrease of $7.9 billion for Consumer loans (mainly a $1.1 billion decrease

in RCB and a $6.7 billion decrease in LCL) and a decrease of $3.5 billion for

corporate loans (almost all of which is related to SAP).

Consumer non-accrual loans (which generally exclude credit cards with

the exception of certain international portfolios) totaled $10.8 billion at

December 31, 2010, compared to $18.3 billion at December 31, 2009. For

total Consumer loans, the 90 days or more past due delinquency rate was

2.99% at December 31, 2010, compared to 4.29% at December 31, 2009 (on a

managed basis). The 30 to 89 days past due Consumer loan delinquency rate

was 2.92% at December 31, 2010, compared to 3.50% at December 31, 2009

(on a managed basis). During 2010, early- and later-stage delinquencies

improved on a dollar basis across most of the Consumer loan portfolios,

driven by improvement in North America mortgages, both in first and

second mortgages, Citi-branded cards in Citicorp and retail partner cards in

Citi Holdings. The improvement in first mortgages was driven by asset sales

and loans moving to permanent modifications.

Corporate non-accrual loans were $8.6 billion at December 31, 2010,

compared to $13.5 billion at December 31, 2009. The decrease in non-

accrual loans from the prior year was mainly due to loan sales, write-offs and

paydowns, which were partially offset by increases due to the weakening of

certain borrowers.

For Citi’s loan accounting policies, see Note 1 to the Consolidated

Financial Statements. See Notes 16 and 17 for additional information on

Citigroup’s Consumer and Corporate loan, credit and allowance data.