Citibank 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

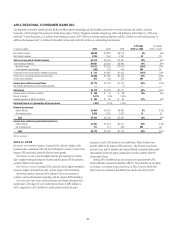

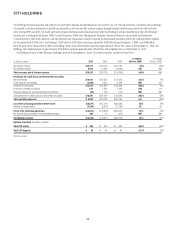

48

LOCAL CONSUMER LENDING

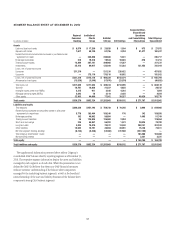

Local Consumer Lending (LCL), which constituted approximately 70% of Citi Holdings by assets as of December 31, 2010, includes a portion of Citigroup’s

North American mortgage business, retail partner cards, Western European cards and retail banking, CitiFinancial North America and other local Consumer

finance businesses globally. The Student Loan Corporation is reported as discontinued operations within the Corporate/Other segment for the second half

of 2010 only. At December 31, 2010, LCL had $252 billion of assets ($226 billion in North America). Approximately $129 billion of assets in LCL as of

December 31, 2010 consisted of U.S. mortgages in the Company’s CitiMortgage and CitiFinancial operations. The North American assets consist of residential

mortgage loans (first and second mortgages), retail partner card loans, personal loans, commercial real estate (CRE), and other consumer loans and assets.

In millions of dollars 2010 2009 2008

% Change

2010 vs. 2009

% Change

2009 vs. 2008

Net interest revenue $13,831 $ 12,995 $ 17,136 6% (24)%

Non-interest revenue 1,995 4,770 6,362 (58) (25)

Total revenues, net of interest expense $15,826 $ 17,765 $ 23,498 (11)% (24)%

Total operating expenses $ 8,064 $ 9,799 $ 14,238 (18)% (31)%

Net credit losses $17,040 $ 19,185 $ 13,111 (11)% 46%

Credit reserve build (release) (1,771) 5,799 8,573 NM (32)

Provision for benefits and claims 775 1,054 1,192 (26) (12)

Provision for unfunded lending commitments —— — ——

Provisions for credit losses and for benefits and claims $16,044 $ 26,038 $ 22,876 (38)% 14%

(Loss) from continuing operations before taxes $ (8,282) $(18,072) $(13,616) 54% (33)%

Benefits for income taxes (3,289) (7,656) (5,259) 57 (46)

(Loss) from continuing operations $ (4,993) $(10,416) $ (8,357) 52% (25)%

Net income attributable to noncontrolling interests 833 12 (76) NM

Net (loss) $ (5,001) $(10,449) $ (8,369) 52% (25)%

Average assets (in billions of dollars) $ 324 $ 351 $ 420 (8)% (16)

Net credit losses as a percentage of average loans 6.20% 6.38% 3.80%

NM Not meaningful

2010 vs. 2009

Revenues, net of interest expense decreased 11% from the prior year. Net

interest revenue increased 6% due to the adoption of SFAS 166/167, partially

offset by the impact of lower balances due to portfolio run-off and asset sales.

Non-interest revenue declined 58%, primarily due to the absence of the

$1.1 billion gain on the sale of Redecard in the first quarter of 2009 and a

higher mortgage repurchase reserve charge.

Operating expenses decreased 18%, primarily due to the impact of

divestitures, lower volumes, re-engineering actions and the absence of costs

associated with the U.S. government loss-sharing agreement, which was

exited in the fourth quarter of 2009.

Provisions for credit losses and for benefits and claims decreased

38%, reflecting a net $1.8 billion credit reserve release in 2010 compared to

a $5.8 billion build in 2009. Lower net credit losses across most businesses

were partially offset by the impact of the adoption of SFAS 166/167. On

a comparable basis, net credit losses were lower year-over-year, driven

by improvement in U.S. mortgages, international portfolios and retail

partner cards.

Assets declined 21% from the prior year, primarily driven by portfolio

run-off, higher loan loss reserve balances, and the impact of asset sales and

divestitures, partially offset by an increase of $41 billion resulting from the

adoption of SFAS 166/167. Key divestitures in 2010 included The Student

Loan Corporation, Primerica, auto loans, the Canadian Mastercard business

and U.S. retail sales finance portfolios.

2009 vs. 2008

Revenues, net of interest expense decreased 24% from the prior year. Net

interest revenue was 24% lower than the prior year, primarily due to lower

balances, de-risking of the portfolio, and spread compression. Non-interest

revenue decreased $1.6 billion, mostly driven by the impact of higher

credit losses flowing through the securitization trusts, partially offset by the

$1.1 billion gain on the sale of Redecard in the first quarter of 2009.

Operating expenses declined 31% from the prior year, due to lower

volumes and reductions from expense re-engineering actions, and the impact

of goodwill write-offs of $3.0 billion in the fourth quarter of 2008, partially

offset by higher costs associated with delinquent loans.

Provisions for credit losses and for benefits and claims increased 14%

from the prior year, reflecting an increase in net credit losses of $6.1 billion,

partially offset by lower reserve builds of $2.8 billion. Higher net credit losses

were primarily driven by higher losses of $3.6 billion in residential real estate

lending, $1.0 billion in retail partner cards, and $0.7 billion in international.

Assets decreased $57 billion from the prior year, primarily driven by lower

originations, wind-down of specific businesses, asset sales, divestitures, write-

offs and higher loan loss reserve balances. Key divestitures in 2009 included

the FI credit card business, Italy Consumer finance, Diners Europe, Portugal

cards, Norway Consumer and Diners Club North America.