Citibank 2010 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

99

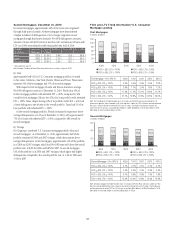

Interest Rate Risk Associated with Consumer Mortgage

Lending Activity

Citigroup originates and funds mortgage loans. As with all other lending

activity, this exposes Citigroup to several risks, including credit, liquidity and

interest rate risks. To minimize credit and liquidity risk, Citigroup sells most

of the mortgage loans it originates, but retains the servicing rights. These

sale transactions create an intangible asset referred to as MSRs, which expose

Citi to interest rate risk. For example, the fair value of MSRs declines with

increased prepayments, and lower interest rates are generally one factor that

tends to lead to increased prepayments.

In managing this risk, Citigroup hedges a significant portion of the value

of its MSRs. However, since the change in the value of these hedges does

not perfectly match the change in the value of the MSRs, Citigroup is still

exposed to what is commonly referred to as “basis risk.” Citigroup manages

this risk by reviewing the mix of the various hedges on a daily basis.

Citigroup’s MSRs totaled $4.554 billion and $6.530 billion at

December 31, 2010 and December 31, 2009, respectively. For additional

information on Citi’s MSRs, see Notes 18 and 22 to the Consolidated

Financial Statements.

As part of its mortgage lending activity, Citigroup commonly enters into

purchase commitments to fund residential mortgage loans at specific interest

rates within a given period of time, generally up to 60 days after the rate

has been set. If the resulting loans will be classified as loans held-for-sale,

Citigroup accounts for the commitments as derivatives. Accordingly, changes

in the fair value of these commitments, which are driven by changes in

mortgage interest rates, are recognized in current earnings after taking into

consideration the likelihood that the commitment will be funded.

Citigroup hedges its exposure to the change in the value of these commitments.

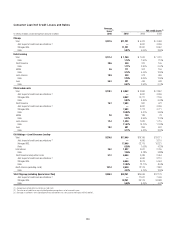

North America Cards

Overview

Citi’s North America cards portfolio consists of its Citi-branded and retail

partner cards portfolios reported in Citicorp—Regional Consumer

Banking and Citi Holdings—Local Consumer Lending, respectively. As of

December 31, 2010, the Citi-branded portfolio totaled $78 billion, while the

retail partner cards portfolio was $46 billion.

Beginning as early as 2008, Citi actively pursued loss mitigation

measures, such as stricter underwriting standards for new accounts and

closing high-risk accounts, in each of its Citi-branded and retail partner

cards portfolios. As a result of these efforts, higher risk customers have either

had their available lines of credit reduced or their accounts closed. On a net

basis, end-of-period open accounts are down 8% in Citi-branded cards and

11% in retail partner cards, each versus prior-year levels.

See “Consumer Loan Modification Programs” below for a discussion of

Citi’s modification programs for card loans.

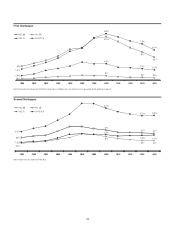

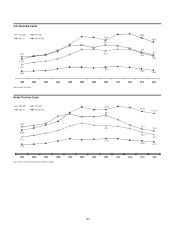

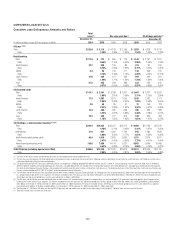

Cards Quarterly Trends—Delinquencies and Net Credit Losses

The following charts detail the quarterly trends in delinquencies and net

credit losses for Citigroup’s North America Citi-branded and retail partner

cards portfolios. Trends for both Citi-branded and retail partner cards

continued to reflect the improving credit quality of these portfolios. In Citi-

branded cards, delinquencies declined for the fourth consecutive quarter to

$1.6 billion, an improvement of 12% from the prior quarter. Net credit losses

declined for the third consecutive quarter to $1.7 billion, 11% lower than the

prior quarter. In retail partner cards, delinquencies declined for the fourth

consecutive quarter while net credit losses declined for the sixth consecutive

quarter. For both portfolios, early-stage delinquencies also continued to

show improvement.