Citibank 2010 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

202

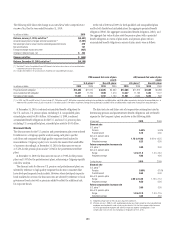

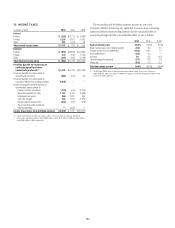

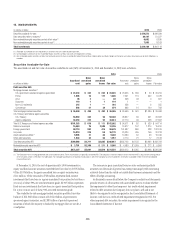

With respect to the New York NOLs, the Company has recorded a net

deferred tax asset of $1.1 billion, along with less significant net operating

losses in various other states for which the Company has recorded a net

deferred tax asset of $0.6 billion and which expire between 2012 and

2031. In addition, the Company has recorded deferred tax assets in foreign

subsidiaries, for which an assertion has been made that the earnings

are indefinitely reinvested, for foreign net operating loss carryforwards

of $487 million (which expire in 2012–2019) and $60 million (with no

expiration), respectively.

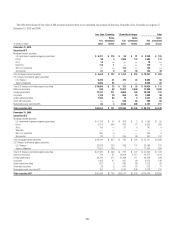

Although realization is not assured, the Company believes that the

realization of the recognized net deferred tax asset of $52.1 billion is more

likely than not based upon expectations as to future taxable income in the

jurisdictions in which the DTAs arise and available tax planning strategies,

as defined in ASC 740, Income Taxes, (formerly SFAS 109) that would be

implemented, if necessary, to prevent a carryforward from expiring. Included

in the net U.S. federal DTA of $41.6 billion are $4 billion in DTLs that will

reverse in the relevant carryforward period and may be used to support the

DTA, and $0.3 billion in compensation deductions that reduced additional

paid-in capital in January 2011 and for which no adjustment was permitted

to such DTA at December 31, 2010 because the related stock compensation

was not yet deductible to Citi. In general, the Company would need to

generate approximately $105 billion of taxable income during the respective

carryforward periods to fully realize its U.S. federal, state and local DTAs.

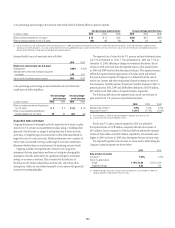

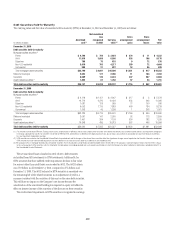

As a result of the losses incurred in 2008 and 2009, the Company is

in a three-year cumulative pretax loss position at December 31, 2010. A

cumulative loss position is considered significant negative evidence in

assessing the realizability of a DTA. The Company has concluded that

there is sufficient positive evidence to overcome this negative evidence. The

positive evidence includes two means by which the Company is able to fully

realize its DTA. First, the Company forecasts sufficient taxable income in the

carryforward period, exclusive of tax planning strategies, even under stressed

scenarios. Secondly, the Company has sufficient tax planning strategies,

including potential sales of businesses and assets, in which it could realize

the excess of appreciated value over the tax basis of its assets. The amount

of the DTA considered realizable, however, is necessarily subject to the

Company’s estimates of future taxable income in the jurisdictions in which it

operates during the respective carryforward periods, which is in turn subject

to overall market and global economic conditions.

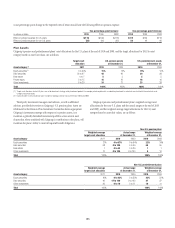

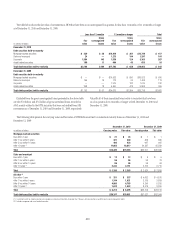

Based upon the foregoing discussion, as well as tax planning

opportunities and other factors discussed below, the U.S. federal and New

York State and City net operating loss carryforward period of 20 years provides

enough time to utilize the DTAs pertaining to the existing net operating loss

carryforwards and any NOL that would be created by the reversal of the future

net deductions that have not yet been taken on a tax return.

The U.S. foreign tax credit carryforward period is 10 years. In addition,

utilization of foreign tax credits in any year is restricted to 35% of foreign

source taxable income in that year. Further, overall domestic losses that

the Company has incurred of approximately $47 billion are allowed to be

reclassified as foreign source income to the extent of 50% of domestic source

income produced in subsequent years and such resulting foreign source

income is in fact sufficient to cover the foreign tax credits being carried

forward. As such, the foreign source taxable income limitation will not be

an impediment to the foreign tax credit carryforward usage as long as the

Company can generate sufficient domestic taxable income within the 10-year

carryforward period. Under U.S. tax law, NOL carry-forwards must generally

be used against taxable income before foreign tax credits (FTCs) or general

business credits (GBCs) can be utilized.

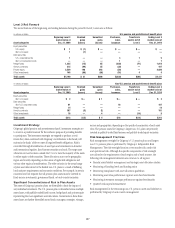

Regarding the estimate of future taxable income, the Company has

projected its pretax earnings predominantly based upon the “core”

businesses in Citicorp that the Company intends to conduct going forward.

These “core” businesses have produced steady and strong earnings in the

past. In 2010, operating trends were positive and credit costs improved. The

Company has already taken steps to reduce its cost structure. Taking these

items into account, the Company is projecting that it will generate sufficient

pretax earnings within the 10-year carryforward period alluded to above

to be able to fully utilize the foreign tax credit carryforward, in addition to

any foreign tax credits produced in such period. Until the U.S. federal NOL

carryforward is fully utilized, the FTCs and GBCs will likely continue to

increase. The Company’s net DTA will decline as additional domestic GAAP

taxable income is generated.

The Company has also examined tax planning strategies available to

it in accordance with ASC 740 that would be employed, if necessary, to

prevent a carryforward from expiring. These strategies include repatriating

low-taxed foreign source earnings for which an assertion that the earnings

are indefinitely reinvested has not been made, accelerating U.S. taxable

income into or deferring U.S. tax deductions out of the latter years of the

carryforward period (e.g., selling appreciated intangible assets and electing

straight-line depreciation), accelerating deductible temporary differences

outside the U.S., holding onto available-for-sale debt securities with losses

until they mature and selling certain assets that produce tax exempt income,

while purchasing assets that produce fully taxable income. In addition,

the sale or restructuring of certain businesses can produce significant U.S.

taxable income within the relevant carryforward periods.

The Company’s ability to utilize its DTAs to offset future taxable income

may be significantly limited if the Company experiences an “ownership

change,” as defined in Section 382 of the Internal Revenue Code of 1986, as

amended (the “Code”). In general, an ownership change will occur if there

is a cumulative change in the Company’s ownership by “5% shareholders”

(as defined in the Code) that exceeds 50 percentage points over a rolling

three-year period. A corporation that experiences an ownership change will

generally be subject to an annual limitation on its pre-ownership change

DTAs equal to the value of the corporation immediately before the ownership

change, multiplied by the long-term tax-exempt rate (subject to certain

adjustments), provided that the annual limitation would be increased

each year to the extent that there is an unused limitation in a prior year.

The limitation arising from an ownership change under Section 382 on

Citigroup’s ability to utilize its DTAs will depend on the value of Citigroup’s

stock at the time of the ownership change. Under IRS Notice 2010-2,

Citigroup did not experience an ownership change within the meaning

of Section 382 as a result of the sales of its common stock held by the

U.S. Treasury.