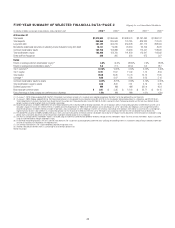

Citibank 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

35

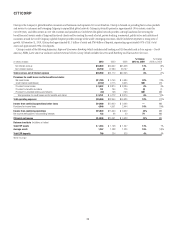

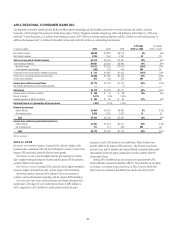

2009 vs. 2008

Revenues, net of interest expense were fairly flat as higher credit losses

in the securitization trusts were offset by higher net interest margin in

cards, higher volumes in retail banking, and higher gains from loan sales

in mortgages.

Net interest revenue was up 20% driven by the impact of pricing actions

relating to the CARD Act and lower funding costs in Citi-branded cards, and

by higher deposit and loan volumes in retail banking, with average deposits

up 12% and average loans up 11%.

Non-interest revenue declined 21%, driven by higher credit losses

flowing through the securitization trusts and by the absence of a

$349 million gain on the sale of Visa shares and a $170 million gain from

a cards portfolio sale in 2008. This decline was partially offset by higher

gains from loan sales in mortgages.

Operating expenses declined 34%. Excluding a 2008 goodwill

impairment charge of $2.3 billion, expenses were down 12% reflecting the

benefits from re-engineering efforts, lower marketing costs, and the absence

of $217 million of repositioning charges in 2008 offset by the absence of a

$159 million Visa litigation reserve release in 2008.

Provisions for credit losses and for benefits and claims increased

$642 million, or 59%, primarily due to rising net credit losses in both cards

and retail banking. The continued weakening of leading credit indicators and

trends in the macroeconomic environment during the period, including rising

unemployment and higher bankruptcy filings, drove higher credit costs. The

cards managed net credit loss ratio increased 376 basis points to 9.41%, while

the retail banking net credit loss ratio increased 44 basis points to 0.90%.