Citibank 2010 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

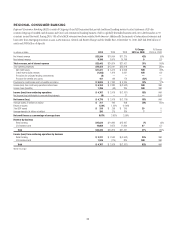

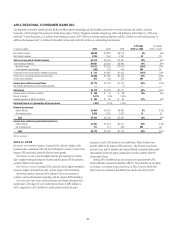

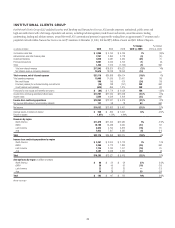

36

EMEA REGIONAL CONSUMER BANKING

EMEA Regional Consumer Banking (EMEA RCB) provides traditional banking and Citi-branded card services to retail customers and small to mid-size

businesses, primarily in Central and Eastern Europe, the Middle East and Africa. Remaining activities in respect of Western Europe retail banking are included

in Citi Holdings. EMEA RCB has generally repositioned its business, shifting from a strategy of widespread distribution to a focused strategy concentrating on

larger urban markets within the region. An exception is Bank Handlowy, which has a mass market presence in Poland. The countries in which EMEA RCB has

the largest presence are Poland, Turkey, Russia and the United Arab Emirates. At December 31, 2010, EMEA RCB had 298 retail bank branches with 3.7 million

customer accounts, $4.4 billion in retail banking loans and $9.2 billion in average deposits. In addition, the business had 2.5 million Citi-branded card

accounts with $2.8 billion in outstanding card loan balances.

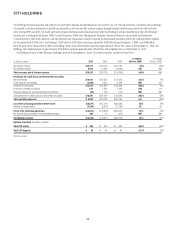

In millions of dollars 2010 2009 2008

% Change

2010 vs. 2009

% Change

2009 vs. 2008

Net interest revenue $ 931 $ 979 $1,269 (5)% (23)%

Non-interest revenue 580 576 596 1(3)

Total revenues, net of interest expense $1,511 $1,555 $1,865 (3)% (17)%

Total operating expenses $1,169 $1,094 $1,500 7% (27)%

Net credit losses $ 320 $ 487 $ 237 (34)% NM

Provision for unfunded lending commitments (4) — — —NM

Credit reserve build (release) (119) 307 75 NM NM

Provisions for loan losses $ 197 $ 794 $ 312 (75)% NM

Income (loss) from continuing operations before taxes $ 145 $ (333) $ 53 NM NM

Income taxes (benefits) 42 (124) 3 NM NM

Income (loss) from continuing operations $ 103 $ (209) $ 50 NM NM

Net income (loss) attributable to noncontrolling interests (1) — 12 —(100)%

Net income (loss) $ 104 $ (209) $ 38 NM NM

Average assets (in billions of dollars) $ 10 $ 11 $ 13 (9)% (15)%

Return on assets 1.04% (1.90)% 0.29%

Average deposits (in billions of dollars) $ 9 $ 9 $ 11 — (18)

Net credit losses as a percentage of average loans 4.34% 5.81% 2.48%

Revenue by business

Retail banking $ 830 $ 889 $1,160 (7)% (23)%

Citi-branded cards 681 666 705 2(6)

Total $1,511 $1,555 $1,865 (3)% (17)%

Income (loss) from continuing operations by business

Retail banking $ (40) $ (179) $ (57) 78% NM

Citi-branded cards 143 (30) 107 NM NM

Total $ 103 $ (209) $ 50 NM NM

NM Not meaningful

2010 vs. 2009

Revenues, net of interest expense declined 3% from the prior-year period.

The decrease was due to lower lending revenues, driven by the repositioning

of the lending strategy toward better profile customer segments for new

acquisitions and liquidation of the existing non-strategic customer portfolios,

across EMEA RCB markets. The lower lending revenues were partially

offset by a 45% growth in investment sales with assets under management

increasing by 14%.

Net interest revenue was 5% lower than the prior year due to lower retail

volumes, with average loans for retail banking down 17%.

Non-interest revenue was higher by 1%, reflecting a marginal increase

in the contribution from an equity investment in Turkey.

Operating expenses increased by 7%, reflecting targeted investment

spending, expansion of the sales force and regulatory and legal expenses.

Provisions for loan losses decreased by $597 million to $197 million. Net

credit losses decreased from $487 million to $320 million, while the loan

loss reserve had a release of $119 million in 2010 compared to a build of

$307 million in 2009. These numbers reflected the ongoing improvement in

credit quality during the period.