Citibank 2010 Annual Report Download - page 221

Download and view the complete annual report

Please find page 221 of the 2010 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

|

|

219

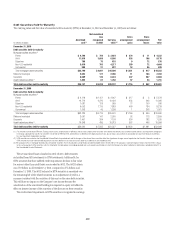

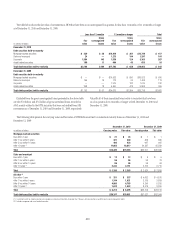

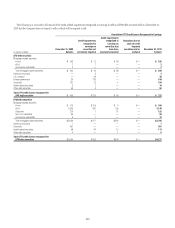

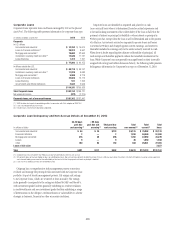

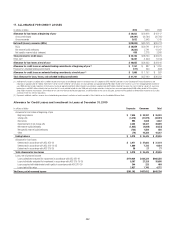

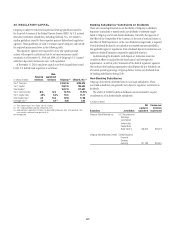

The following table presents Corporate credit quality information as of

December 31, 2010:

Corporate Loans Credit Quality Indicators

at December 31, 2010

In millions of dollars

Recorded

investment in

loans (1)

Investment grade (2)

Commercial and industrial $ 51,042

Financial institutions 47,310

Mortgage and real estate 8,119

Leases 1,204

Other 21,844

Total investment grade $129,519

Non-investment grade (2)

Accrual

Commercial and industrial $ 25,992

Financial institutions 3,412

Mortgage and real estate 3,329

Leases 695

Other 4,316

Non-accrual

Commercial and industrial 5,125

Financial institutions 1,258

Mortgage and real estate 1,782

Leases 45

Other 400

Total non-investment grade $ 46,354

Private Banking loans managed on a

delinquency basis (2) $ 12,662

Loans at fair value 2,627

Corporate loans, net of unearned income $191,162

(1) Recorded investment in a loan includes accrued interest, net of deferred loan fees and costs,

unamortized premium or discount, and less any direct write-downs.

(2) Held-for-investment loans accounted for on an amortized cost basis.

Corporate loans and leases identified as impaired and placed on non-

accrual status are written down to the extent that principal is judged to

be uncollectible. Impaired collateral-dependent loans and leases, where

repayment is expected to be provided solely by the sale of the underlying

collateral and there are no other available and reliable sources of repayment,

are written down to the lower of cost or collateral value. Cash-basis loans

are returned to an accrual status when all contractual principal and interest

amounts are reasonably assured of repayment, and there is a sustained

period of repayment performance in accordance with the contractual terms.