Citibank 2012 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

74

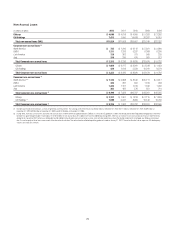

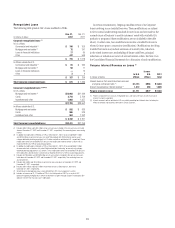

CREDIT RISK

Credit risk is the potential for financial loss resulting from the failure of a

borrower or counterparty to honor its financial or contractual obligations.

Credit risk arises in many of Citigroup’s business activities, including:

• wholesale and retail lending;

• capital markets derivative transactions;

• structured finance; and

• repurchase agreements and reverse repurchase transactions.

Credit risk also arises from settlement and clearing activities, when Citi

transfers an asset in advance of receiving its counter-value, or advances funds

to settle a transaction on behalf of a client. Concentration risk, within credit

risk, is the risk associated with having credit exposure concentrated within a

specific client, industry, region or other category.

Credit Risk Management

Credit risk is one of the most significant risks Citi faces as an institution. As

a result, Citi has a well-established framework in place for managing credit

risk across all businesses. This includes a defined risk appetite, credit limits

and credit policies, both at the business level as well as at the firm-wide

level. Citi’s credit risk management also includes processes and policies

with respect to problem recognition, including “watch lists,” portfolio

review, updated risk ratings and classification triggers. With respect to Citi’s

settlement and clearing activities, intra-day client usage of lines is closely

monitored against limits, as well as against “normal” usage patterns. To

the extent a problem develops, Citi typically moves the client to a secured

(collateralized) operating model. Generally, Citi’s intra-day settlement and

clearing lines are uncommitted and cancellable at any time.

To manage concentration of risk within credit risk, Citi has in place a

concentration management framework consisting of industry limits, obligor

limits and single-name triggers. In addition, as noted under “Management

of Global Risk—Risk Aggregation and Stress Testing” above, independent

risk management reviews concentration of risk across Citi’s regions and

businesses to assist in managing this type of risk.

Credit Risk Measurement and Stress Testing

Credit exposures are generally reported in notional terms for accrual loans,

reflecting the value at which the loans are carried on the Consolidated

Balance Sheet. Credit exposure arising from capital markets activities is

generally expressed as the current mark-to-market, net of margin, reflecting

the net value owed to Citi by a given counterparty.

The credit risk associated with these credit exposures is a function of

the creditworthiness of the obligor, as well as the terms and conditions of

the specific obligation. Citi assesses the credit risk associated with its credit

exposures on a regular basis through its loan loss reserve process (see

“Significant Accounting Policies and Significant Estimates” and Notes 1

and 17 to the Consolidated Financial Statements below), as well as through

regular stress testing at the company-, business-, geography- and product-

levels. These stress-testing processes typically estimate potential incremental

credit costs that would occur as a result of either downgrades in the credit

quality, or defaults, of the obligors or counterparties.