Citibank 2012 Annual Report Download - page 275

Download and view the complete annual report

Please find page 275 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

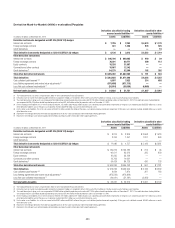

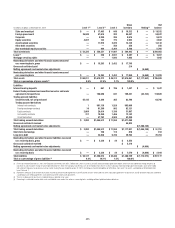

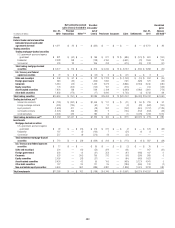

253

Subprime-related direct exposures in CDOs

The valuation of high-grade and mezzanine asset-backed security (ABS)

CDO positions utilizes prices based on the underlying assets of each high-

grade and mezzanine ABS CDO. The high-grade and mezzanine positions

are largely hedged through the ABX and bond short positions. This results in

closer symmetry in the way these long and short positions are valued by the

Company. Citigroup uses trader marks to value this portion of the portfolio

and will do so as long as it remains largely hedged.

For most of the lending and structuring direct subprime exposures,

fair value is determined utilizing observable transactions where available,

other market data for similar assets in markets that are not active and other

internal valuation techniques.

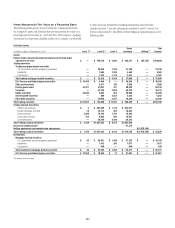

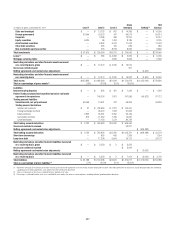

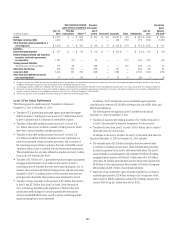

Investments

The investments category includes available-for-sale debt and marketable

equity securities, whose fair value is generally determined by utilizing similar

procedures described for trading securities above or, in some cases, using

consensus pricing as the primary source.

Also included in investments are nonpublic investments in private equity

and real estate entities held by the S&B business. Determining the fair

value of nonpublic securities involves a significant degree of management

resources and judgment, as no quoted prices exist and such securities are

generally very thinly traded. In addition, there may be transfer restrictions

on private equity securities. The Company uses an established process for

determining the fair value of such securities, utilizing commonly accepted

valuation techniques, including comparables analysis. In determining the

fair value of nonpublic securities, the Company also considers events such

as a proposed sale of the investee company, initial public offerings, equity

issuances or other observable transactions. As discussed in Note 15 to the

ConsolidatedFinancialStatements,theCompanyusesnetassetvalue(NAV)

to value certain of these investments.

PrivateequitysecuritiesaregenerallyclassifiedasLevel3ofthefair

value hierarchy.

Short-term borrowings and long-term debt

Where fair value accounting has been elected, the fair value of non-

structured liabilities is determined by utilizing internal models using the

appropriate discount rate for the applicable maturity. Such instruments are

generallyclassifiedasLevel2ofthefairvaluehierarchy,asallinputsare

readily observable.

The Company determines the fair value of structured liabilities (where

performance is linked to structured interest rates, inflation or currency risks)

and hybrid financial instruments (where performance is linked to risks

other than interest rates, inflation or currency risks) using the appropriate

derivative valuation methodology (described above) given the nature of the

embeddedriskprofile.SuchinstrumentsareclassifiedasLevel2orLevel3

depending on the observability of significant inputs to the model.

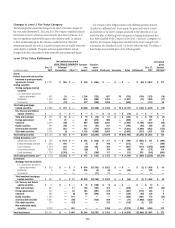

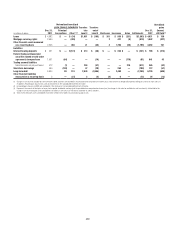

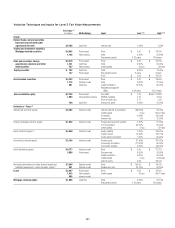

Alt-A mortgage securities

The Company classifies its Alt-A mortgage securities as held-to-maturity,

available-for-sale and trading investments. The securities classified as trading

and available-for-sale are recorded at fair value with changes in fair value

reported in current earnings and AOCI, respectively. For these purposes, Citi

defines Alt-A mortgage securities as non-agency residential mortgage-backed

securities (RMBS) where (i) the underlying collateral has weighted average

FICO scores between 680 and 720 or (ii) for instances where FICO scores

are greater than 720, RMBS have 30% or less of the underlying collateral

composed of full documentation loans.

Similar to the valuation methodologies used for other trading securities

and trading loans, the Company generally determines the fair values of

Alt-A mortgage securities utilizing internal valuation techniques. Fair value

estimates from internal valuation techniques are verified, where possible, to

prices obtained from independent vendors. Consensus data providers compile

prices from various sources. Where available, the Company may also make

use of quoted prices for recent trading activity in securities with the same or

similar characteristics to the security being valued.

The valuation techniques used for Alt-A mortgage securities, as with other

mortgage exposures, are price-based and discounted cash flows. The primary

market-derived input is yield. Cash flows are based on current collateral

performance with prepayment rates and loss projections reflective of current

economic conditions of housing price change, unemployment rates, interest

rates, borrower attributes and other market indicators.

Alt-A mortgage securities that are valued using these methods are

generallyclassifiedasLevel2.However,Alt-Amortgagesecuritiesbacked

by Alt-A mortgages of lower quality or subordinated tranches in the capital

structurearemostlyclassifiedasLevel3duetothereducedliquiditythat

exists for such positions, which reduces the reliability of prices available from

independent sources.