Citibank 2012 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

121

Differences Between Country Risk and Cross-Border Risk

As described in more detail in the sections above, there are significant

differences between the reporting of country risk and cross-border risk. A

general summary of the more significant differences is as follows:

• Country risk is the risk that an event within a country will impair the

value of Citi’s franchise or adversely affect the ability of obligors within

the country to honor their obligations to Citi. Country risk reporting in

Citi’s internal risk management systems is based on the identification

of the country where the client relationship, taken as a whole, is most

directly exposed to the economic, financial, sociopolitical or legal risks.

Generally, country risk includes the benefit of margin received as well as

offsetting exposures and hedge positions. As such, country risk generally

measures net exposure to a credit or market risk event.

• Cross-border risk, as defined by the FFIEC, focuses on the potential

exposure if foreign governments take actions, such as enacting exchange

controls, which prevent the conversion of local currency to non-local

currency or restrict the remittance of funds outside the country. Unlike

country risk, FFIEC cross-border risk measures exposure to the immediate

obligors or counterparties domiciled in the given country or, if applicable,

by the location of collateral or guarantors of the legally binding

guarantees, generally without the benefit of margin received or hedge

positions, and recognizes offsetting exposures only for certain products.

The differences between the presentation of country risk and cross-border

risk can be substantial, including the identification of the country of risk,

as described above. In addition, some of the more significant differences by

product are described below:

• Forcountryrisk,netderivativereceivablesaregenerallyreportedbased

on fair value, netting receivables and payables under the same legally

binding netting agreement, and recognizing the benefit of margin

received under legally enforceable margin agreements and any hedge

positions in place. For cross-border risk, these items are also reported

based on fair value and allow for netting of receivables and payables if

a legally binding netting agreement is in place, but only with the same

specific counterparty, and do not recognize the benefit of margin received

or hedges in place.

• For country risk, secured financing transactions, such as repurchase

agreements and reverse repurchase agreements, as well as securities

loaned and borrowed, are reported based on the net credit exposure

arising from the transaction, which is typically small or zero given the

over-collateralized structure of these transactions. For cross-border risk,

reverse repurchase agreements and securities borrowed are reported based

on notional amounts and do not include the value of any collateral

received (repurchase agreements and securities loaned are not included in

cross-border risk reporting).

• For country risk, loans are reported net of hedges and collateral pledged

under legally enforceable margin agreements. For cross-border risk, loans

are reported without taking hedges into account.

• For country risk, securities in AFS and trading portfolios are reported on a

net basis, netting long positions against short positions. For cross-border

risk, securities in AFS and trading portfolios are not netted.

• For country risk, credit default swaps (CDS) are reported based on the

net notional amount of CDS purchased and sold, assuming zero recovery

from the underlying entity, and adjusted for any mark-to-market

receivable or payable position. For cross-border risk, CDS are included

based on the gross notional amount sold, and do not include any

offsetting purchased CDS on the same underlying entity.

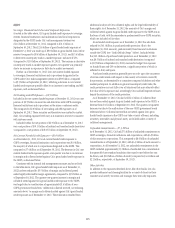

Argentina and Venezuela Developments

Citi operates in several countries with strict foreign exchange controls that

limit its ability to convert local currency into U.S. dollars and/or transfer funds

outside the country. In such cases, Citi could be exposed to a risk of loss in the

event that the local currency devalues as compared to the U.S. dollar.

Argentina

Since 2011, the Argentine government has been tightening its foreign

exchange controls. As a result, Citi’s access to U.S. dollars and other foreign

currencies, which apply to capital repatriation efforts, certain operating

expenses, and discretionary investments offshore, has become limited.

In addition, beginning in January 2012, the Central Bank of Argentina

increased its minimum capital requirements, which affects Citi’s ability to

remit profits out of the country.

As of December 31, 2012, Citi’s net investment in its Argentine operations

was approximately $740 million, compared to $740 million as of

December 31, 2011 and down from $800 million as of September 30, 2012.

The decrease quarter-over-quarter was primarily the result of a dividend of

approximately $65 million received by Citi in the fourth quarter of 2012. For

the full year of 2012, Citi received dividends of $125 million.

Citi uses the Argentine peso as the functional currency in Argentina

and translates its financial statements into U.S. dollars using the official

exchange rate as published by the Central Bank of Argentina, which

continued to devalue its currency during the fourth quarter of 2012, from

4.70 Argentine pesos to one U.S. dollar at September 30, 2012 to 4.90

Argentine pesos to one U.S. dollar at December 31, 2012. It is generally

expected that the devaluation of the Argentine peso could continue.

The impact of devaluations of the Argentine peso on Citi’s net investment

in Argentina is reported as a translation loss in stockholders’ equity offset, to

the extent hedged, by:

• gains or losses recorded in stockholders’ equity on net investment hedges

that have been designated as, and qualify for, hedge accounting under

ASC 815 Derivatives and Hedging; and

• gainsorlossesrecordedinearningsforitsU.S.dollardenominated

monetary assets or currency futures held in Argentina that do not

qualify as net investment hedges under ASC 815.