Citibank 2012 Annual Report Download - page 257

Download and view the complete annual report

Please find page 257 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

235

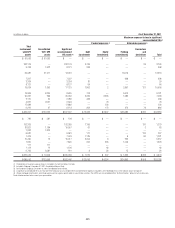

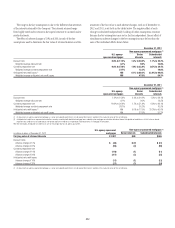

The Company also re-securitizes U.S. government-agency guaranteed

mortgage-backed (agency) securities. During the 12 months ended December

31, 2012, Citi transferred agency securities with a fair value of approximately

$30.3 billion to re-securitization entities. As of December 31, 2012, the fair

value of Citi-retained interests in agency re-securitization transactions

structured by Citi totaled approximately $1.7 billion ($1.1 billion of which

related to re-securitization transactions executed in 2012) and is recorded in

Trading account assets. The original fair value of agency re-securitization

transactions in which Citi holds a retained interest as of December 31, 2012

was approximately $71.2 billion.

As of December 31, 2012, the Company did not consolidate any private-

label or agency re-securitization entities.

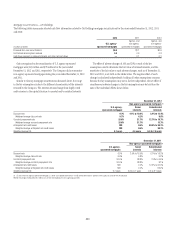

Citi-Administered Asset-Backed Commercial Paper Conduits

The Company is active in the asset-backed commercial paper conduit

business as administrator of several multi-seller commercial paper conduits

and also as a service provider to single-seller and other commercial paper

conduits sponsored by third parties.

Citi’s multi-seller commercial paper conduits are designed to provide

the Company’s clients access to low-cost funding in the commercial paper

markets. The conduits purchase assets from or provide financing facilities to

clients and are funded by issuing commercial paper to third-party investors.

The conduits generally do not purchase assets originated by the Company.

The funding of the conduits is facilitated by the liquidity support and credit

enhancements provided by the Company.

As administrator to Citi’s conduits, the Company is generally responsible

for selecting and structuring assets purchased or financed by the conduits,

making decisions regarding the funding of the conduits, including

determining the tenor and other features of the commercial paper issued,

monitoring the quality and performance of the conduits’ assets, and

facilitating the operations and cash flows of the conduits. In return, the

Company earns structuring fees from customers for individual transactions

and earns an administration fee from the conduit, which is equal to the

income from the client program and liquidity fees of the conduit after

payment of conduit expenses. This administration fee is fairly stable, since

most risks and rewards of the underlying assets are passed back to the clients

and, once the asset pricing is negotiated, most ongoing income, costs and

fees are relatively stable as a percentage of the conduit’s size.

The conduits administered by the Company do not generally invest

in liquid securities that are formally rated by third parties. The assets are

privately negotiated and structured transactions that are designed to be

held by the conduit, rather than actively traded and sold. The yield earned

by the conduit on each asset is generally tied to the rate on the commercial

paper issued by the conduit, thus passing interest rate risk to the client. Each

asset purchased by the conduit is structured with transaction-specific credit

enhancement features provided by the third-party client seller, including

over collateralization, cash and excess spread collateral accounts, direct

recourse or third-party guarantees. These credit enhancements are sized with

the objective of approximating a credit rating of A or above, based on the

Company’s internal risk ratings.

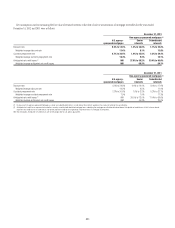

Substantially all of the funding of the conduits is in the form of short-

term commercial paper, with a weighted average life generally ranging

from 25 to 45 days. At the respective period ends December 31, 2012 and

December 31, 2011, the weighted average lives of the commercial paper

issued by consolidated and unconsolidated conduits were approximately 38

and 37 days, respectively.

The primary credit enhancement provided to the conduit investors is in

the form of transaction-specific credit enhancement described above. In

addition, each consolidated conduit has obtained a letter of credit from the

Company, which needs to be sized to at least 8–10% of the conduit’s assets

with a floor of $200 million. The letters of credit provided by the Company

to the consolidated conduits total approximately $2.1 billion. The net result

across all multi-seller conduits administered by the Company is that, in the

event defaulted assets exceed the transaction-specific credit enhancements

described above, any losses in each conduit are allocated first to the Company

and then the commercial paper investors.

The Company also provides the conduits with two forms of liquidity

agreements that are used to provide funding to the conduits in the event

of a market disruption, among other events. Each asset of the conduits is

supported by a transaction-specific liquidity facility in the form of an asset

purchase agreement (APA). Under the APA, the Company has generally

agreed to purchase non-defaulted eligible receivables from the conduit at par.

The APA is not generally designed to provide credit support to the conduit,

as it generally does not permit the purchase of defaulted or impaired assets.

Any funding under the APA will likely subject the underlying borrower to

the conduits to increased interest costs. In addition, the Company provides

the conduits with program-wide liquidity in the form of short-term lending

commitments. Under these commitments, the Company has agreed to lend

to the conduits in the event of a short-term disruption in the commercial

paper market, subject to specified conditions. The Company receives fees for

providing both types of liquidity agreements and considers these fees to be on

fair market terms.