Citibank 2012 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

26

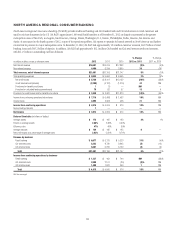

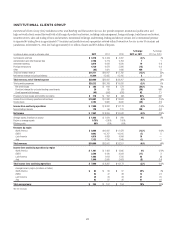

2012 vs. 2011

Net income decreased 10%. Excluding $2.5 billion of negative CVA/DVA (see

table below), net income increased 56%, primarily driven by a 13% increase

in revenues.

Revenues decreased 8%, driven by the negative CVA/DVA and mark-to-

market losses on hedges related to accrual loans. Excluding CVA/DVA:

• Revenues increased 13%, reflecting higher revenues in most major

S&B businesses. Overall, Citi gained wallet share during 2012 in most

major products and regions, while maintaining what it believes to be a

disciplined risk appetite for the market environment.

• Fixed income markets revenues increased 28%, reflecting strong

performance in rates and currencies and higher revenues in credit-related

and securitized products. These results reflected an improved market

environment and more balanced trading flows, particularly in the

second half of 2012. Rates and currencies performance reflected strong

client and trading results in G-10 FX, G-10 rates and Citi’s local markets

franchise. Credit products, securitized markets and municipals products

experienced improved trading results, particularly in the second half of

2012, compared to the prior-year period. Citi’s position serving corporate

clients for markets products also contributed to the strength and diversity

of client flows.

• Equity markets revenues increased 1%, due to improved derivatives

performance as well as the absence of proprietary trading losses in

2011, partially offset by lower cash equity volumes that impacted the

industry as a whole. Citi’s improved performance in derivatives reflected

improved trading and continued progress in capturing additional client

wallet share.

• Investment banking revenues increased 10%, reflecting increases in

debt underwriting and advisory revenues, partially offset by lower equity

underwriting revenues. Debt underwriting revenues rose 18%, driven by

increases in investment grade and high yield bond issuances. Advisory

revenues increased 4%, despite the overall reduction in market activity

during the year. Equity underwriting revenues declined 7%, driven by

lower levels of market and client activity.

• Lending revenues decreased 45%, driven by the mark-to-market losses

on hedges related to accrual loans (see table below). The loss on lending

hedges compared to a gain in the prior year, resulted from CDS spreads

narrowing during 2012. Excluding lending hedges related to accrual

loans, lending revenues increased 31%, primarily driven by growth in the

Corporate loan portfolio and improved spreads in most regions.

• Private Bank revenues increased 8%, driven by growth in client assets as a

result of client acquisition and development efforts in Citi’s targeted client

segments. Deposit volumes, investment assets under management and

loans all increased, while pricing and product mix optimization initiatives

offset underlying spread compression across products.

Expenses decreased 4%. Excluding repositioning charges of $349 million

in 2012 (including $237 million in the fourth quarter of 2012) compared

to $267 million in 2011, expenses also decreased 4%, driven by efficiency

savings from ongoing re-engineering programs and lower compensation

costs. The repositioning efforts in S&B announced in the fourth quarter of

2012 are designed to streamline S&B’s client coverage model and improve

overall productivity.

Provisions increased 5% to $122 million, primarily reflecting lower loan

loss reserve releases, partially offset by lower net credit losses, both due to

portfolio stabilization.