Citibank 2012 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

129

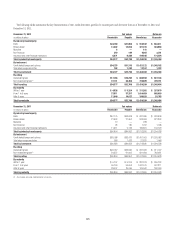

As discussed in Note 4 to the Consolidated Financial Statements, as of

December 31, 2012, Citigroup consists of the following business segments:

Global Consumer Banking, Institutional Clients Group, Corporate/

Other and Citi Holdings. Goodwill impairment testing is performed at

the level below the business segment (referred to as a reporting unit).

Goodwill is allocated to Citi’s reporting units at the date the goodwill is

initially recorded. Once goodwill has been allocated to the reporting units,

it generally no longer retains its identification with a particular acquisition,

but instead becomes identified with the reporting unit as a whole. As a

result, all of the fair value of each reporting unit is available to support the

allocated goodwill. Citi’s nine reporting units at December 31, 2012 were

North America Regional Consumer Banking, EMEA Regional Consumer

Banking, Asia Regional Consumer Banking, Latin America Regional

Consumer Banking, Securities and Banking, Transaction Services,

Brokerage and Asset Management, Local Consumer Lending—Cards

and Local Consumer Lending—Other.

Citi’s reporting unit structure in 2012 was the same as the reporting unit

structure in 2011, although certain underlying businesses were transferred

between certain reporting units in the first quarter of 2012. As of January 1,

2012, a substantial majority of the Citi retail services business previously

included within the Local Consumer Lending—Cards reporting unit was

transferred to North America—Regional Consumer Banking. In addition,

certain small businesses included within the Local Consumer Lending—

Cards reporting unit were transferred to Local Consumer Lending—Other.

Additionally, an insurance business in El Salvador within Brokerage and

Asset Management was transferred to Latin America Regional Consumer

Banking. Goodwill affected by these transfers was reassigned from Local

Consumer Lending—Cards and Brokerage and Asset Management,

respectively, to those reporting units that received the businesses using a

relative fair value approach. Subsequent to January 1, 2012, goodwill has

been allocated to disposals and tested for impairment under the reporting

unit structure reflecting these transfers. An interim goodwill impairment

test was performed on the impacted reporting units as of January 1, 2012,

resulting in no impairment.

Under ASC 350, Intangibles—Goodwill and Other, the Company has an

option to assess qualitative factors to determine if it is necessary to perform

the goodwill impairment test. If, after assessing the totality of events or

circumstances, the Company determines that it is not more-likely-than-not

that the fair value of a reporting unit is less than its carrying amount, no

further testing is necessary. If, however, the Company determines that it is

more-likely-than-not that the fair value of a reporting unit is less than its

carrying amount, then the Company is required to perform the two-step

goodwill impairment test.

The first step requires a comparison of the fair value of the individual

reporting unit to its carrying value, including goodwill. If the fair value of

the reporting unit is in excess of the carrying value, the related goodwill

is considered not to be impaired and no further analysis is necessary. If

the carrying value of the reporting unit exceeds the fair value, there is an

indication of potential impairment and a second step of testing is performed

to measure the amount of impairment, if any, for that reporting unit.

If required, the second step involves calculating the implied fair value

of goodwill for each of the affected reporting units. The implied fair value

of goodwill is determined in the same manner as the amount of goodwill

recognized in a business combination. The implied fair value is the excess

of the fair value of the reporting unit determined in step one over the fair

value of the net assets and identifiable intangibles. If the amount of goodwill

allocated to the reporting unit exceeds the implied fair value of the goodwill

in the pro forma purchase price allocation, an impairment charge is

recorded for the excess. A recognized impairment charge cannot exceed the

amount of goodwill allocated to a reporting unit and cannot subsequently be

reversed even if the fair value of the reporting unit recovers.

The carrying value used in both steps of the impairment test for each

reporting unit is derived by allocating Citigroup’s total stockholders’ equity

to each of Citi’s components (defined below) based on the risk capital

assessed for each component. Refer to the “Risk Capital” section above for

further discussion. The assigned carrying value of the nine reporting units,

the Special Asset Pool and Corporate/Other (together the “components”)

is equal to Citigroup’s total stockholders’ equity. In allocating Citigroup’s

total stockholders’ equity to each component, the reported goodwill and

intangibles associated with each reporting unit are specifically included in

the carrying amount of the respective reporting units and the remaining

stockholders’ equity is then allocated to each component based on the

relative risk capital associated with each component.

Goodwill impairment testing involves management judgment, requiring

an assessment of whether the carrying value of the reporting unit can be

supported by the fair value of the individual reporting unit using widely

accepted valuation techniques, such as the market approach (earnings

multiples and/or transaction multiples) and/or the income approach

(discounted cash flow (DCF) method). In applying these methodologies, Citi

utilizes a number of factors, including actual operating results, future

business plans, economic projections, and market data. Citi prepares a

formal three-year strategic plan for its businesses on an annual basis. These

projections incorporate certain external economic projections developed at

the point in time the plan is developed. For the purpose of performing any

impairment test, the most recent three-year forecast available is updated by

Citi to reflect current economic conditions as of the testing date. Citi used

the updated long-range financial forecasts as a basis for its annual goodwill

impairment test on July 1, 2012.