Citibank 2012 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

21

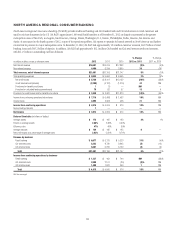

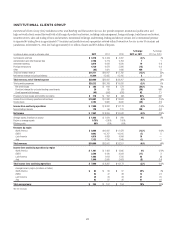

The discussion of the results of operations for Latin America RCB below excludes the impact of FX translation for all periods presented. Presentation

of the results of operations, excluding the impact of FX translation, are non-GAAP financial measures. Citi believes the presentation of Latin America

RCB’s results excluding the impact of FX translation is a more meaningful depiction of the underlying fundamentals of the business. For a

reconciliation of certain of these metrics to the reported results, see the table above.

2012 vs. 2011

Net income was flat to the prior year as higher revenues were offset by higher

credit costs and repositioning charges.

Revenues increased 9%, primarily due to strong revenue growth in

Mexico and higher volumes, mostly related to personal loans and credit

cards. However, continued regulatory pressure involving foreign exchange

controls and related measures in Argentina and Venezuela is expected to

negatively impact revenues in the near term. Net interest revenue increased

10% due to increased volumes, partially offset by continued spread

compression. Citi expects spread compression to continue to negatively

impact revenues in this business during 2013. Non-interest revenue increased

7%, primarily due to increased business volumes in the private pension fund

and insurance businesses.

Expenses increased 6%, primarily due to $131 million of repositioning

charges in the fourth quarter of 2012, higher volume-driven expenses and

increased legal and related costs.

Provisions increased 39%, primarily due to increased loan loss reserve

builds driven by underlying business volume growth, primarily in Mexico

and Colombia. In addition, net credit losses increased in the retail portfolios,

primarily in Mexico, reflecting volume growth. Citi believes that net credit

losses in Latin America will likely continue to trend higher as various loan

portfolios continue to mature.

2011 vs. 2010

Net income declined 14% as higher revenues were more than offset by higher

expenses and higher credit costs.

Revenues increased 7% primarily due to higher volumes. Net interest

revenue increased 6% driven by the continued growth in lending and

deposit volumes, partially offset by spread compression driven in part by

the continued move toward customers with a lower risk profile and stricter

underwriting criteria, especially in the Citi-branded cards portfolio. Non-

interest revenue increased 8%, primarily driven by an increase in banking fee

income from credit card purchase sales.

Expenses increased 10% due to higher volumes and investment spending,

including increased marketing and customer acquisition costs as well as new

branches, partially offset by continued savings initiatives. The increase in the

level of investment spending in the business was largely completed at the end

of 2011.

Provisions increased 43%, reflecting lower loan loss reserve releases. Net

credit losses declined 13%, driven primarily by improvements in the Mexico

cards portfolio due to the move toward customers with a lower-risk profile

and stricter underwriting criteria.