Citibank 2012 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

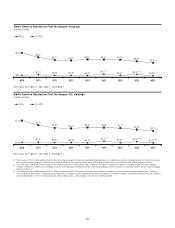

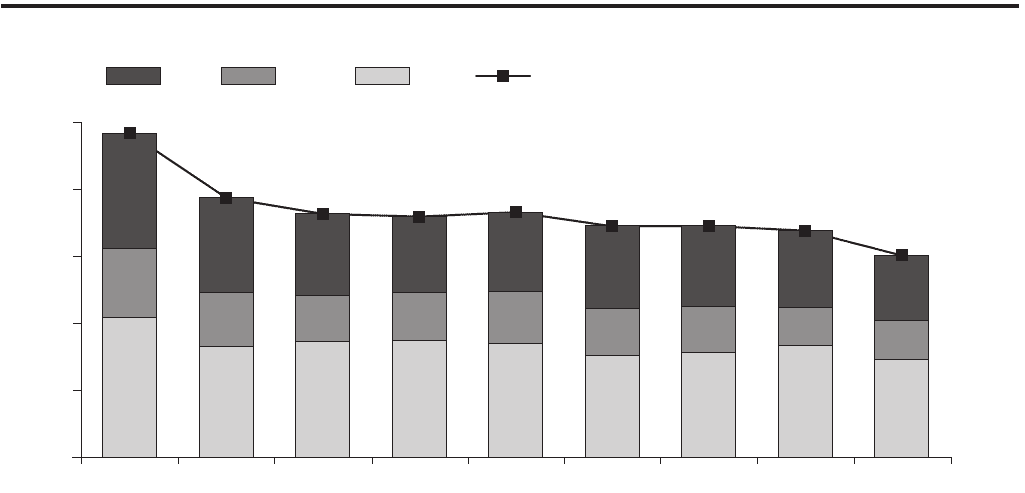

85

North America Residential First Mortgage Delinquencies—Citi Holdings

In billions of dollars

Days Past Due:

0

2

4

6

8

10

30+ DPD180+ 90-179 30-89

4Q123Q122Q121Q124Q113Q112Q111Q114Q10

4.19 3.30 3.45 3.49 3.39 3.03 3.14 3.33 2.91

2.06

1.61 1.38 1.43 1.57 1.41 1.37 1.16 1.17

3.43

2.84 2.44 2.26 2.36 2.47 2.41

1.95

2.28

9.68

7.75 7.27 7.19 7.32 6.90 6.91 6.77

6.03

Note: For each of the tables above, past due exclude (i) U.S. mortgage loans that are guaranteed by U.S. government-sponsored agencies because the potential loss predominantly resides with the U.S. agencies, and (ii)

loans recorded at fair value. Totals may not sum due to rounding.

Management actions, primarily asset sales and to a lesser extent

modification programs, continued to be the primary drivers of the overall

improved asset performance within Citi’s residential first mortgage portfolio

in Citi Holdings during the periods presented above (excluding the impacts to

net credit losses described in the notes to the tables above).

Citi sold approximately $2.1 billion of delinquent residential first

mortgages during 2012, including $0.6 billion during the fourth quarter of

2012. Since the beginning of 2010, Citi has sold approximately $9.6 billion of

delinquent residential mortgages.

In addition, Citi modified approximately $0.9 billion and $0.3 billion

of residential first mortgage loans during 2012 and in the fourth quarter of

2012, respectively, including loan modifications pursuant to the national

mortgage settlement. (For additional information on Citi’s residential first

mortgage loan modifications, see Note 16 to the Consolidated Financial

Statements.) Loan modifications under the national mortgage settlement

have improved Citi’s 30+ days past due delinquencies by approximately

$249 million as of the end of 2012. While re-defaults of previously modified

mortgages under the HAMP and Citi Supplemental Modification (CSM)

programs continued to track favorably versus expectations as of December 31,

2012, Citi’s residential first mortgage portfolio continued to show some signs

of the impact of re-defaults of previously modified mortgages.

Citi believes that its ability to offset increasing delinquencies or net credit

losses in its residential first mortgage portfolio, due to any deterioration of

the underlying credit performance of these loans, re-defaults, the lengthening

of the foreclosure process (see “Foreclosures” below) or otherwise, pursuant

to asset sales or modifications could be limited going forward as a result of

the lower remaining inventory of loans to sell or modify or due to lack of

market demand for asset sales. Citi has taken these trends and uncertainties,

including the potential for re-defaults, into consideration in determining its

loan loss reserves. See “North America Consumer Mortgages—Loan Loss

Reserve Coverage” below.