Citibank 2012 Annual Report Download - page 229

Download and view the complete annual report

Please find page 229 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

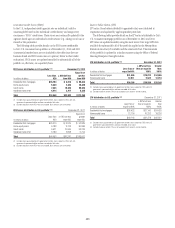

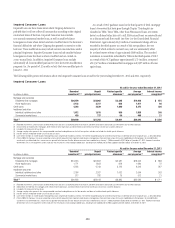

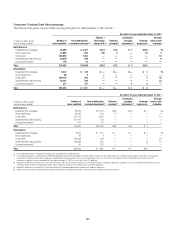

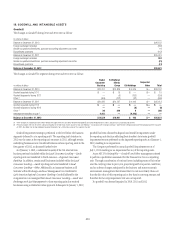

207

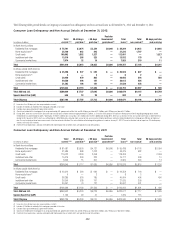

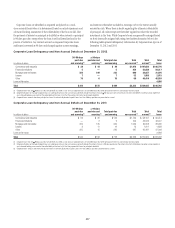

Corporate loans are identified as impaired and placed on a cash

(non-accrual) basis when it is determined, based on actual experience and

a forward-looking assessment of the collectability of the loan in full, that

the payment of interest or principal is doubtful or when interest or principal

is 90 days past due, except when the loan is well collateralized and in the

process of collection. Any interest accrued on impaired Corporate loans

and leases is reversed at 90 days and charged against current earnings,

and interest is thereafter included in earnings only to the extent actually

received in cash. When there is doubt regarding the ultimate collectability

of principal, all cash receipts are thereafter applied to reduce the recorded

investment in the loan. While Corporate loans are generally managed based

on their internally assigned risk rating (see further discussion below), the

following tables present delinquency information by Corporate loan type as of

December 31, 2012 and 2011:

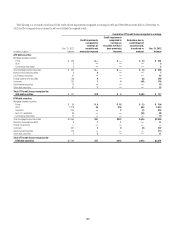

Corporate Loan Delinquency and Non-Accrual Details at December 31, 2012

In millions of dollars

30–89 days

past due

and accruing (1)

> 90 days

past due and

accruing (1)

Total past due

and accruing

Total

non-accrual (2)

Total

current (3)

Total

loans

Commercial and industrial $ 38 $ 10 $ 48 $1,078 $107,650 $108,776

Financial institutions 5 — 5 454 53,858 54,317

Mortgage and real estate 224 109 333 680 30,057 31,070

Leases 7 — 7 52 1,956 2,015

Other 70 6 76 69 46,414 46,559

Loans at fair value 4,056

Total $ 344 $125 $ 469 $2,333 $239,935 $246,793

(1) Corporate loans that are > 90 days past due are generally classified as non-accrual. Corporate loans are considered past due when principal or interest is contractually due but unpaid.

(2) Citi generally does not manage Corporate loans on a delinquency basis. Non-accrual loans generally include those loans that are > 90 days past due or those loans for which Citi believes, based on actual experience

and a forward-looking assessment of the collectability of the loan in full, that the payment of interest or principal is doubtful.

(3) Corporate loans are past due when principal or interest is contractually due but unpaid. Loans less than 30 days past due are presented as current.

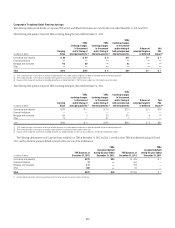

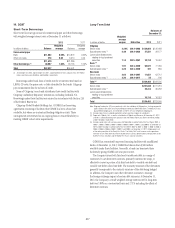

Corporate Loan Delinquency and Non-Accrual Details at December 31, 2011

In millions of dollars

30–89 days

past due

and accruing (1)

> 90 days

past due and

accruing (1)

Total past due

and accruing

Total

non-accrual (2)

Total

current (3)

Total

loans

Commercial and industrial $ 93 $ 30 $ 123 $1,134 $ 98,157 $ 99,414

Financial institutions — 2 2 763 42,642 43,407

Mortgage and real estate 224 125 349 1,039 26,908 28,296

Leases 3 11 14 13 1,811 1,838

Other 225 15 240 287 46,481 47,008

Loans at fair value 3,939

Total $ 545 $183 $ 728 $3,236 $215,999 $223,902

(1) Corporate loans that are > 90 days past due are generally classified as non-accrual. Corporate loans are considered past due when principal or interest is contractually due but unpaid.

(2) Citi generally does not manage Corporate loans on a delinquency basis. Non-accrual loans generally include those loans that are ≥ 90 days past due or those loans for which Citi believes, based on actual experience

and a forward-looking assessment of the collectability of the loan in full, that the payment of interest or principal is doubtful.

(3) Corporate loans are past due when principal or interest is contractually due but unpaid. Loans less than 30 days past due are presented as current.