Citibank 2012 Annual Report Download - page 274

Download and view the complete annual report

Please find page 274 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

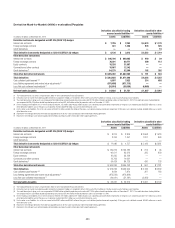

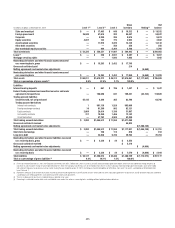

252

ReportsofinventorythatisclassifiedwithinLevel3ofthefairvalue

hierarchy are distributed to senior management in Finance, Risk and the

individual business. This inventory is also discussed in Risk Committees and

in monthly meetings with senior trading management. As deemed necessary,

reports may go to the Audit Committee of the Board of Directors or to the

full Board of Directors. Whenever a valuation adjustment is needed to bring

the price of an asset or liability to its exit price, Product Control reports it to

management along with other price verification results.

In addition, the pricing models used in measuring fair value are governed

by an independent control framework. Although the models are developed

and tested by the individual business units, they are independently validated

bytheModelValidationGroupwithinRiskManagementandreviewedby

Finance with respect to their impact on the price verification procedures. The

purpose of this independent control framework is to assess model risk arising

from models’ theoretical soundness, calibration techniques where needed,

and the appropriateness of the model for a specific product in a defined

market.Valuationadjustments,ifany,gothroughasimilarindependent

review process as the valuation models. To ensure their continued

applicability, models are independently reviewed annually. In addition,

Risk Management approves and maintains a list of products permitted to be

valued under each approved model for a given business.

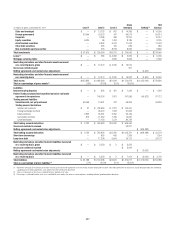

Securities purchased under agreements to resell and

securities sold under agreements to repurchase

No quoted prices exist for such instruments, so fair value is determined using

a discounted cash-flow technique. Cash flows are estimated based on the

terms of the contract, taking into account any embedded derivative or other

features. Expected cash flows are discounted using interest rates appropriate

to the maturity of the instrument as well as the nature of the underlying

collateral. Generally, when such instruments are held at fair value, they are

classifiedwithinLevel2ofthefairvaluehierarchy,astheinputsusedinthe

valuation are readily observable. However, certain long-dated positions are

classifiedwithinLevel3ofthefairvaluehierarchy.

Trading account assets and liabilities—trading securities

and trading loans

When available, the Company uses quoted market prices to determine the

fairvalueoftradingsecurities;suchitemsareclassifiedasLevel1ofthe

fair value hierarchy. Examples include some government securities and

exchange-traded equity securities.

For bonds and secondary market loans traded over the counter, the

Company generally determines fair value utilizing valuation techniques,

including discounted cash flows, price-based and internal models, such

as Black-Scholes and Monte Carlo simulation. Fair value estimates from

these internal valuation techniques are verified, where possible, to prices

obtainedfromindependentvendors.Vendorscompilepricesfromvarious

sources and may apply matrix pricing for similar bonds or loans where no

price is observable. A price-based methodology utilizes, where available,

quoted prices or other market information obtained from recent trading

activity of assets with similar characteristics to the bond or loan being valued.

The yields used in discounted cash flow models are derived from the same

price information. Trading securities and loans priced using such methods

aregenerallyclassifiedasLevel2.However,whenlessliquidityexistsfora

security or loan, a quoted price is stale, a significant adjustment to the price

of a similar security or loan is necessary to reflect differences in the terms of

the actual security or loan being valued, or prices from independent sources

are insufficient to corroborate valuation, a loan or security is generally

classifiedasLevel3.Thepriceinputusedinaprice-basedmethodologymay

be zero for a security, such as a subprime CDO, that is not receiving any

principal or interest and is currently written down to zero.

Where the Company’s principal market for a portfolio of loans is the

securitization market, the Company uses the securitization price to determine

the fair value of the portfolio. The securitization price is determined from

the assumed proceeds of a hypothetical securitization in the current market,

adjusted for transformation costs (i.e., direct costs other than transaction

costs) and securitization uncertainties such as market conditions and

liquidity. As a result of the severe reduction in the level of activity in

certain securitization markets since the second half of 2007, observable

securitization prices for certain directly comparable portfolios of loans

have not been readily available. Therefore, such portfolios of loans are

generallyclassifiedasLevel3ofthefairvaluehierarchy.However,forother

loan securitization markets, such as commercial real estate loans, pricing

verification of the hypothetical securitizations has been possible, since these

markets have remained active. Accordingly, this loan portfolio is classified as

Level2ofthefairvaluehierarchy.

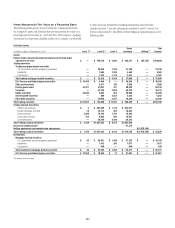

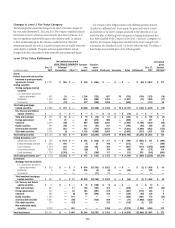

Trading account assets and liabilities—derivatives

Exchange-traded derivatives are generally measured at fair value using

quotedmarket(i.e.,exchange)pricesandareclassifiedasLevel1ofthefair

value hierarchy.

The majority of derivatives entered into by the Company are executed over

the counter and are valued using internal valuation techniques, as no quoted

market prices exist for such instruments. The valuation techniques and inputs

depend on the type of derivative and the nature of the underlying instrument.

The principal techniques used to value these instruments are discounted

cash flows and internal models, including Black-Scholes and Monte Carlo

simulation. The fair values of derivative contracts reflect cash the Company has

paid or received (for example, option premiums paid and received).

The key inputs depend upon the type of derivative and the nature of

the underlying instrument and include interest rate yield curves, foreign-

exchange rates, volatilities and correlation. The Company uses overnight

indexed swap (OIS) curves as fair value measurement inputs for the

valuation of certain collateralized interest-rate related derivatives. The

instrumentisclassifiedaseitherLevel2orLevel3dependinguponthe

observability of the significant inputs to the model.