Citibank 2012 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

120

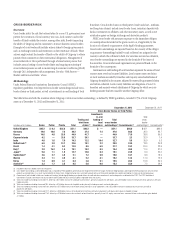

CROSS-BORDER RISK

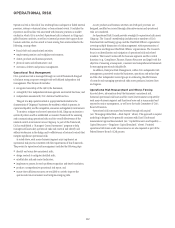

Overview

Cross-border risk is the risk that actions taken by a non-U.S. government may

prevent the conversion of local currency into non-local currency and/or the

transfer of funds outside the country, among other risks, thereby impacting

the ability of Citigroup and its customers to transact business across borders.

Examples of cross-border risk include actions taken by foreign governments

such as exchange controls and restrictions on the remittance of funds. These

actions might restrict the transfer of funds or the ability of Citigroup to obtain

payment from customers on their contractual obligations. Management of

cross-border risk at Citi is performed through a formal review process that

includes annual setting of cross-border limits and ongoing monitoring of

cross-border exposures as well as monitoring of economic conditions globally

through Citi’s independent risk management. See also “Risk Factors—

Market and Economic Risks” above.

Methodology

Under Federal Financial Institutions Examination Council (FFIEC)

regulatory guidelines, total reported cross-border outstandings include cross-

border claims on third parties, as well as investments in and funding of local

franchises. Cross-border claims on third parties (trade and short-, medium-

and long-term claims) include cross-border loans, securities, deposits with

banks, investments in affiliates, and other monetary assets, as well as net

revaluation gains on foreign exchange and derivative products.

FFIEC cross-border risk measures exposure to the immediate obligors

or counterparties domiciled in the given country or, if applicable, by the

location of collateral or guarantors of the legally binding guarantees.

Cross-border outstandings are reported based on the country of the obligor

or guarantor. Outstandings backed by cash collateral are assigned to the

country in which the collateral is held. For securities received as collateral,

cross-border outstandings are reported in the domicile of the issuer of

the securities. Cross-border resale agreements are presented based on the

domicile of the counterparty.

Investments in and funding of local franchises represent the excess of local

country assets over local country liabilities. Local country assets are claims

on local residents recorded by branches and majority-owned subsidiaries of

Citigroup domiciled in the country, adjusted for externally guaranteed claims

and certain collateral. Local country liabilities are obligations of non-U.S.

branches and majority-owned subsidiaries of Citigroup for which no cross-

border guarantee has been issued by another Citigroup office.

The table below sets forth the countries where Citigroup’s total cross-border outstandings, as defined by FFIEC guidelines, exceeded 0.75% of total Citigroup

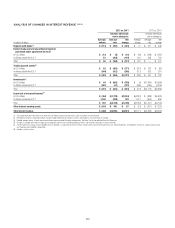

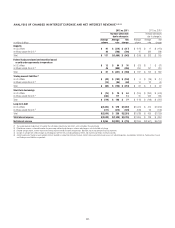

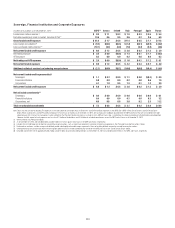

assets as of December 31, 2012 and December 31, 2011:

December 31, 2012 December 31, 2011

Cross-Border Claims on Third Parties

In billions of U.S. dollars Banks Public Private Total

Trading and

short-term

claims

(1)

Investments

in, and

funding of

local

franchises

Total

cross-border

outstandings (2)

Commitments

(3)

Total

cross-

border

outstandings (2) Commitments (3)

United Kingdom $25.2 $ 0.3 $25.6 $51.1 $45.2 $ — $51.1 $85.0 $42.1 $90.3

Germany 14.6 18.0 7.6 40.2 37.4 7.4 47.6 66.8 36.2 64.7

France 14.6 4.8 25.5 44.9 41.7 — 44.9 71.0 38.6 69.3

Cayman Islands 0.2 — 33.5 33.7 30.1 — 33.7 2.3 32.0 1.4

India 4.8 1.6 7.9 14.3 12.2 18.4 32.7 5.5 30.9 5.3

Netherlands (4) 6.9 3.0 13.7 23.6 18.1 2.2 25.8 24.9 18.3 24.8

Brazil 1.4 4.1 9.3 14.8 9.5 6.9 21.7 19.2 20.4 22.9

Italy (5) 2.0 15.2 1.9 19.1 18.2 0.3 19.4 49.8 11.4 37.0

Japan (6) 9.8 1.1 1.8 12.7 12.6 6.4 19.1 23.8 6.0 20.0

Switzerland (7) 2.6 2.7 3.8 9.1 7.2 9.9 19.0 18.7 8.6 18.9

Mexico 2.4 1.1 4.6 8.1 5.2 8.1 16.2 12.4 17.9 12.2

Korea 1.4 0.9 4.1 6.4 3.8 9.1 15.5 26.4 16.3 24.5

Australia (8) 3.3 1.7 3.5 8.5 5.6 6.8 15.3 25.9 7.2 26.4

(1) Included in total cross-border claims on third parties.

(2) Cross-border outstandings, as described above and as required by FFIEC guidelines, generally do not recognize the benefit of margin received or hedge positions and recognize offsetting exposures only for certain

products and relationships. As a result, market volatility in interest rates, foreign exchange rates and credit spreads will cause the level of reported cross-border outstandings to increase, all else being equal.

(3) Commitments (not included in total cross-border outstandings) include legally binding cross-border letters of credit and other commitments and contingencies as defined by the FFIEC. The FFIEC definition of

commitments includes commitments to local residents to be funded with local currency liabilities originated within the country.

(4) Total cross-border outstandings increased 41%, driven by a $2.1 billion increase in funding of local franchises, primarily in placements with banks, and a $2.6 billion increase in the private sector, primarily in AFS and

trading securities.

(5) Total cross-border outstandings increased 70%, driven by a $7.4 billion increase in the public sector, primarily in trading accounts and revaluation gains.

(6) Total cross-border outstandings increased 218%, driven by a $7.7 billion increase in the bank sector, primarily in resale agreements, and a $5.2 billion increase in funding of local franchises, primarily in

placements with banks.

(7) Total cross-border outstandings increased 121%, driven by a $9.0 billion increase in funding of local franchises, primarily in placements with banks due to business liquidity strategy.

(8) Total cross-border outstandings increased 115%, driven by a $7.0 billion increase in investments of local franchises, primarily in non-U.S. equity, consumer loans, commercial loans and revaluation gains booked

as trading.