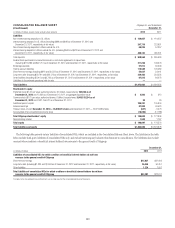

Citibank 2012 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

153

Private-Label Residential Mortgage Securitizations

Citi is also exposed to representation and warranty repurchase claims as a

result of mortgage loans sold through private-label residential mortgage

securitizations. These representations were generally made or assigned to the

issuing trust and related to, among other things, the following:

• the absence of fraud on the part of the borrower, the seller or any

appraiser, broker or other party involved in the origination of the loan

(which was sometimes wholly or partially limited to the knowledge of the

representation provider);

• whether the property securing the loan was occupied by the borrower as

his or her principal residence;

• the loan’s compliance with applicable federal, state and local laws;

• whether the loan was originated in conformity with the originator’s

underwriting guidelines; and

• detailed data concerning the loans that were included on the mortgage

loan schedule.

Repurchase Reserve

Citi has recorded a mortgage repurchase reserve (referred to as the

repurchase reserve) for its potential repurchase or make-whole liability

regarding representation and warranty claims that is included in Other

liabilities in the Consolidated Balance Sheet. Citi’s repurchase reserve

primarily relates to whole loan sales to the GSEs and is thus calculated

primarily based on Citi’s historical repurchase activity with the GSEs.

Repurchase Reserve—Whole Loan Sales

The repurchase reserve is based on various assumptions which, as referenced

above, are primarily based on Citi’s historical repurchase activity with the

GSEs. As of December 31, 2012, the most significant assumptions used

to calculate the reserve levels are: (i) the probability of a claim based on

correlation between loan characteristics and repurchase claims; (ii) claims

appeal success rates; and (iii) estimated loss per repurchase or make-whole

payment. In addition, Citi considers reimbursements estimated to be received

from third-party sellers, which are generally based on Citi’s analysis of its

most recent collection trends and the financial solvency or viability of the

third-party sellers, in estimating its repurchase reserve.

As referenced above, the repurchase reserve estimation process for

potential whole loan representation and warranty claims relies on various

assumptions that involve numerous estimates and judgments, including

with respect to certain future events, and thus entails inherent uncertainty.

Therefore, Citi estimates and discloses the range of reasonably possible loss

for whole loan sale representation and warranty claims in excess of amounts

accrued. This estimate is derived by modifying the key assumptions discussed

above to reflect management’s judgment regarding reasonably possible

adverse changes to those assumptions. Citi’s estimate of reasonably possible

loss is based on currently available information, significant judgment and

numerous assumptions that are subject to change.

In the case of a repurchase of a credit-impaired SOP 03-3 loan, the

difference between the loan’s fair value and unpaid principal balance at the

time of the repurchase is recorded as a utilization of the repurchase reserve.

Make-whole payments to the investor are also treated as utilizations and

charged directly against the reserve. The repurchase reserve is estimated

when Citi sells loans (recorded as an adjustment to the gain on sale, which is

included in Other revenue in the Consolidated Statement of Income) and is

updated quarterly. Any change in estimate is recorded in Other revenue.

Repurchase Reserve—Private-Label Securitizations

Investors in private-label securitizations may seek recovery for alleged

breaches of representations and warranties, as well as losses caused by

non-performing loans more generally, through repurchase claims or

through litigation premised on a variety of legal theories. Citi considers

litigation relating to private-label securitizations as part of its contingencies

analysis. For additional information, see Note 28 to the Consolidated

Financial Statements.

Citi cannot reasonably estimate probable losses from future repurchase

claims for private-label securitizations because the claims to date have been

received at an unpredictable rate, the factual basis for those claims is unclear,

and very few such claims have been resolved. Rather, at the present time, Citi

records reserves related to private-label securitizations repurchase claims

based on estimated losses arising from those claims received that appear to be

based on a review of the underlying loan files. These reserves are recorded in

Principal transactions in the Consolidated Statement of Income.

Goodwill

Goodwill represents the excess of acquisition cost over the fair value

of net tangible and intangible assets acquired. Goodwill is subject to

annual impairment testing and between annual tests if an event occurs

or circumstances change that would more-likely-than-not reduce the fair

value of a reporting unit below its carrying amount. The Company has an

option to assess qualitative factors to determine if it is necessary to perform

the goodwill impairment test. If, after assessing the totality of events or

circumstances, the Company determines that it is not more-likely-than-not

that the fair value of a reporting unit is less than its carrying amount, no

further testing is necessary. If, however, the Company determines that it is

more-likely-than-not that the fair value of a reporting unit is less than its

carrying amount, then the Company is required to perform the first step

of the two-step goodwill impairment test. Furthermore, on any business

dispositions, goodwill is allocated to the business disposed of based on the

ratio of the fair value of the business disposed of to the fair value of the

reporting unit.

Additional information on Citi’s goodwill impairment testing can be

found in Note 18 to the Consolidated Financial Statements.